Lowe's 2015 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2015 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

|

|

44

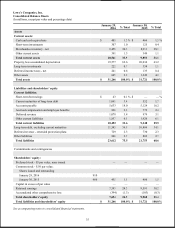

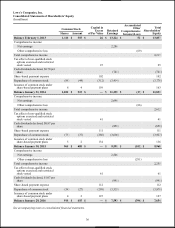

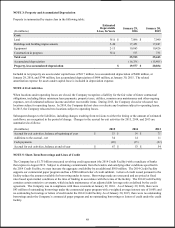

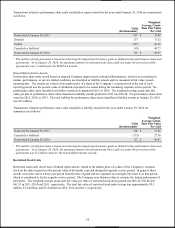

Recent Accounting Pronouncements - In November 2015, the Financial Accounting Standards Board (FASB) issued

Accounting Standards Update (ASU) 2015-17, Balance Sheet Classification of Deferred Taxes. The ASU requires entities to

classify deferred tax liabilities and assets as noncurrent in a classified statement of financial position. This ASU is effective for

fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. Early adoption is permitted for

all entities as of the beginning of an interim or annual reporting period. The Company elected to early adopt this accounting

update as of January 29, 2016, and applied it retrospectively to prior periods. The adoption of the ASU resulted in a

reclassification of $230 million of current deferred tax assets and $97 million of noncurrent deferred tax liabilities to

noncurrent deferred tax assets in the Company’s consolidated balance sheet as of January 30, 2015. The adoption of this

guidance did not have any impact on the Company’s consolidated statements of earnings, comprehensive income, shareholders’

equity, or cash flows.

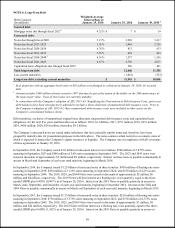

In April 2015, the FASB issued ASU 2015-03, Simplifying the Presentation of Debt Issuance Costs. The ASU requires that

debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the

carrying amount of that debt liability. This ASU is effective for fiscal years beginning after December 15, 2015, and interim

periods within those fiscal years, with early adoption permitted. The Company elected to early adopt this accounting update as

of January 29, 2016, and applied it retrospectively to prior periods. The adoption of the ASU resulted in a reclassification of

debt issuance costs of $9 million from other assets to long-term debt, excluding current maturities in the Company’s

consolidated balance sheet as of January 30, 2015. The adoption of this guidance did not have any impact on the Company’s

consolidated statements of earnings, comprehensive income, shareholders’ equity, or cash flows.

Effective January 31, 2015, the Company adopted ASU 2014-08, Reporting Discontinued Operations and Disclosures of

Components of an Entity. The ASU amends the definition of a discontinued operation and also provides new disclosure

requirements for disposals meeting the definition, and for those that do not meet the definition, of a discontinued operation.

Under the new guidance, a discontinued operation may include a component or a group of components of an entity, or a

business or nonprofit activity that has been disposed of or is classified as held for sale, and represents a strategic shift that has

or will have a major effect on an entity’s operations and financial results. The ASU also expands the scope to include the

disposals of equity method investments and acquired businesses held for sale. The adoption of the guidance by the Company

did not have a material impact on its consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842). The guidance in this ASU supersedes the leasing

guidance in Topic 840, Leases. Under the new guidance, lessees are required to recognize lease assets and lease liabilities on

the balance sheet for those leases previously classified as operating leases. For leases with a term of 12 months or less, a lessee

is permitted to make an accounting policy election by class of underlying asset not to recognize lease assets and lease liabilities.

If a lessee makes this election, it should recognize lease expense for such leases generally on a straight-line basis over the lease

term. This ASU is effective for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years,

with early adoption permitted. The Company is currently evaluating the impact of adopting this ASU on its consolidated

financial statements.

In January 2016, the FASB issued ASU 2016-01, Recognition and Measurement of Financial Assets and Liabilities. The ASU

requires, among other things, that entities measure equity investments (except those accounted for under the equity method of

accounting or those that result in consolidation of the investee) at fair value, with changes in fair value recognized in net

income. Under this ASU, entities will no longer be able to recognize unrealized holding gains and losses on equity securities

classified today as available-for-sale in other comprehensive income, and they will no longer be able to use the cost method of

accounting for equity securities that do not have readily determinable fair values. The guidance for classifying and measuring

investments in debt securities and loans is not impacted. ASU 2016-01 eliminates certain disclosure requirements related to

financial instruments measured at amortized cost and adds disclosures related to the measurement categories of financial assets

and financial liabilities. The guidance is effective for annual periods beginning after December 15, 2017. Early adoption is

permitted for only certain portions of the ASU. The adoption of this guidance by the Company is not expected to have a

material impact on its consolidated financial statements.

In July 2015, the FASB issued ASU 2015-11, Simplifying the Measurement of Inventory. The ASU requires entities using the

first-in, first-out (FIFO) inventory costing method to subsequently value inventory at the lower of cost and net realizable value.

The ASU defines net realizable value as the estimated selling prices in the ordinary course of business, less reasonably

predictable costs of completion, disposal, and transportation. This ASU requires prospective application and is effective for

fiscal years beginning after December 15, 2016, and interim periods within those fiscal years, with early adoption permitted.

The adoption of this guidance by the Company is not expected to have a material impact on its consolidated financial

statements.