McDonalds 2015 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2015 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

McDonald's Corporation 2015 Annual Report 23

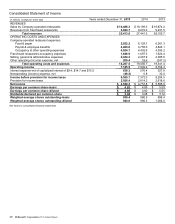

PROVISION FOR INCOME TAXES

In 2015, 2014 and 2013, the reported effective income tax rates

were 30.9%, 35.5% and 31.9%, respectively.

In 2014, the higher effective income tax rate was primarily due

to a change in tax reserves for 2003-2010 resulting from an

unfavorable lower tax court ruling in a foreign tax jurisdiction, as

well as the impact of changes in tax reserves related to audit

progression in multiple foreign tax jurisdictions. These items had a

negative impact of 4.1% on the effective tax rate.

In 2013, the effective income tax rate included a tax benefit of

nearly $50 million, reflecting the retroactive impact of certain tax

benefits as a result of the American Taxpayer Relief Act of 2012.

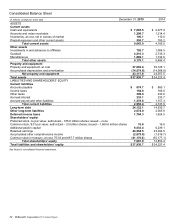

Consolidated net deferred tax liabilities included tax assets,

net of valuation allowance, of $1.8 billion in 2015 and $1.6 billion

in 2014. Substantially all of the net tax assets are expected to be

realized in the U.S. and other profitable markets.

RECENTLY ISSUED ACCOUNTING STANDARDS

Revenue Recognition

In May 2014, the Financial Accounting Standards Board ("FASB")

issued guidance codified in Accounting Standards Codification

("ASC") 606, "Revenue Recognition - Revenue from Contracts

with Customers," which amends the guidance in ASC 605,

"Revenue Recognition." In July 2015, the FASB made a decision

to defer by one year the effective date of its new standard to

January 1, 2018, although early adoption is permitted as of

January 1, 2017.

The new standard allows for either a full retrospective or

modified retrospective transition approach. The Company does not

believe that the standard will impact its recognition of revenue

from company-operated restaurants or its recognition of royalties

from restaurants operated by franchisees or licensed to affiliates

and developmental licensees, which are based on a percent of

sales. The Company is continuing to evaluate the impact the

adoption of this standard will have on the recognition of other less

significant revenue transactions, such as initial fees from

franchisees for new restaurant openings or new franchise terms.

Cash Flows

The Company generates significant cash from its operations and

has substantial credit availability and capacity to fund operating

and discretionary spending such as capital expenditures, debt

repayments, dividends and share repurchases.

Cash provided by operations totaled $6.5 billion and

exceeded capital expenditures by $4.7 billion in 2015, while cash

provided by operations totaled $6.7 billion and exceeded capital

expenditures by $4.1 billion in 2014. In 2015, cash provided by

operations decreased $191 million or 3% compared with 2014,

primarily due to lower operating results, including the impact from

weaker foreign currencies, and other operating activity. This was

partly offset by changes in working capital. In 2014, cash provided

by operations decreased $390 million or 5% compared with 2013

primarily due to lower operating results, partly offset by lower

income tax payments.

Cash used for investing activities totaled $1.4 billion in 2015,

a decrease of $885 million compared with 2014. The decrease

primarily reflected lower capital expenditures. Cash used for

investing activities totaled $2.3 billion in 2014, a decrease of $369

million compared with 2013. The decrease primarily reflected

lower capital expenditures, a decrease in other investing activities

related to short-term time deposits and higher proceeds from sales

of restaurant businesses.

Cash provided by financing activities totaled $735 million in

2015, an increase of $5.4 billion compared with 2014, primarily

due to an increase in net borrowings, partly offset by higher

treasury stock purchases. Cash used for financing activities

totaled $4.6 billion in 2014, an increase of $575 million compared

with 2013, primarily due to higher treasury stock purchases, partly

offset by an increase in net borrowings.

The Company’s cash and equivalents balance was $7.7

billion and $2.1 billion at year end 2015 and 2014, respectively.

The increase in 2015 was due to higher net borrowings to be used

primarily for share repurchases in 2016. In addition to cash and

equivalents on hand and cash provided by operations, the

Company can meet short-term funding needs through its

continued access to commercial paper borrowings and line of

credit agreements.

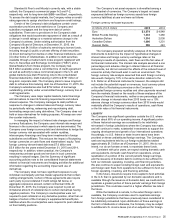

RESTAURANT DEVELOPMENT AND CAPITAL EXPENDITURES

In 2015, the Company opened 989 restaurants and closed 722

restaurants. In 2014, the Company opened 1,316 restaurants and

closed 487 restaurants. The increase in restaurant closings in

2015 reflected a strategic review that resulted in additional

closures of under-performing restaurants. The Company closes

restaurants for a variety of reasons, such as existing sales and

profit performance or loss of real estate tenure.

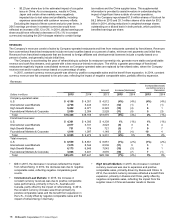

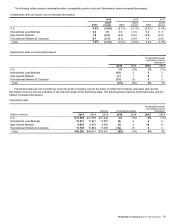

Systemwide restaurants at year end

2015 2014 2013

U.S. 14,259 14,350 14,278

International Lead Markets 6,802 6,717 6,604

High Growth Markets 5,266 5,031 4,639

Foundational Markets &

Corporate 10,198 10,160 9,908

Total 36,525 36,258 35,429

Approximately 82% of the restaurants at year-end 2015 were

franchised, including 90% in the U.S., 82% in International Lead

markets, 46% in High Growth markets and 90% in Foundational

markets.

Capital expenditures decreased $769 million or 30% in 2015,

primarily due to fewer new restaurant openings and lower

reinvestment at existing restaurants. Capital expenditures

decreased $242 million or 9% in 2014, primarily due to lower

reinvestment in existing restaurants. In both years, the lower

reinvestment primarily reflected fewer reimages.

Capital expenditures invested in the U.S., International Lead

markets and High Growth markets represented about 90% of the

total in 2015, 2014 and 2013.

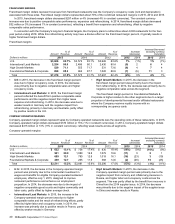

Capital expenditures

In millions 2015 2014 2013

New restaurants $892$ 1,435 $ 1,473

Existing restaurants 842 1,044 1,244

Other(1) 80 104 108

Total capital expenditures $1,814 $ 2,583 $ 2,825

Total assets $37,939 $34,227 $36,626

(1) Primarily corporate equipment and other office-related expenditures.

New restaurant investments in all years were concentrated in

markets with strong returns or opportunities for long-term growth.

Average development costs vary widely by market depending on

the types of restaurants built and the real estate and construction

costs within each market. These costs, which include land,

buildings and equipment, are managed through the use of

optimally-sized restaurants, construction and design efficiencies,

and leveraging best practices. Although the Company is not

responsible for all costs for every restaurant opened, total

development costs (consisting of land, buildings and equipment)