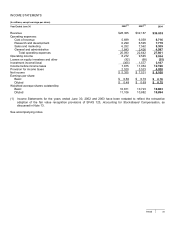

Microsoft 2004 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2004 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS (CONTINUED)

PAGE 30

SFAS 109, Accounting for Income Taxes, establishes financial accounting and reporting standards for the effect of

income taxes. The objectives of accounting for income taxes are to recognize the amount of taxes payable or refundable

for the current year and deferred tax liabilities and assets for the future tax consequences of events that have been

recognized in an entity’s financial statements or tax returns. Judgment is required in assessing the future tax

consequences of events that have been recognized in our financial statements or tax returns. Variations in the actual

outcome of these future tax consequences could materially impact our financial position or our results of operations.

ISSUES AND UNCERTAINTIES

This Annual Report contains statements that are forward-looking. These statements are based on current expectations

and assumptions that are subject to risks and uncertainties. Actual results could differ materially because of issues and

uncertainties such as those listed below and elsewhere in this report, which, among others, should be considered in

evaluating our future financial performance.

Challenges to our Business Model. Since our inception, our business model has been based upon customers

agreeing to pay a fee to license software developed and distributed by us. Under this commercial software model,

software developers bear the costs of converting original ideas into software products through investments in research

and development, offsetting these costs with the revenue received from the distribution of their products. We believe the

commercial software model has had substantial benefits for users of software, allowing them to rely on our expertise and

the expertise of other software developers that have powerful incentives to develop innovative software that is useful,

reliable, and compatible with other software and hardware. In recent years, there has been a growing challenge to the

commercial software model. Under the non-commercial software model, open source software produced by loosely

associated groups of unpaid programmers and made available for license to end users without charge is distributed by

firms at nominal cost that earn revenue on complementary services and products, without having to bear the full costs of

research and development for the open source software. The most notable example of open source software is the Linux

operating system. While we believe our products provide customers with significant advantages in security and

productivity, and generally have a lower total cost of ownership than open source software, the popularization of the non-

commercial software model continues to pose a significant challenge to our business model, including recent efforts by

proponents of open source software to convince governments worldwide to mandate the use of open source software in

their purchase and deployment of software products. To the extent open source software gains increasing market

acceptance, sales of our products may decline, we may have to reduce the prices we charge for our products, and

revenue and operating margins may consequently decline.

Intellectual Property Rights. We defend our intellectual property rights, but unlicensed copying and use of software

and intellectual property rights represents a loss of revenue to us. While this adversely affects U.S. revenue, the impact

on revenue from outside the United States is more significant, particularly in countries where laws are less protective of

intellectual property rights. Throughout the world, we actively educate consumers about the benefits of licensing genuine

products and educate lawmakers about the advantages of a business climate where intellectual property rights are

protected. However, continued educational and enforcement efforts may not affect revenue positively, and revenue could

be adversely affected by further deterioration in compliance with existing legal protections or reductions in the legal

protection for intellectual property rights of software developers.

From time to time we receive notices from others claiming we infringe their intellectual property rights. The number of

these claims may grow. Responding to these claims may require us to enter into royalty and licensing agreements on

unfavorable terms, require us to stop selling or to redesign affected products, or to pay damages or to satisfy

indemnification commitments with our customers. If we are required to enter into such agreements or take such actions,

our operating margins may decline as a result.

We have made and expect to continue making significant expenditures to acquire the use of technology and intellectual

property rights, including via cross-licenses of broad patent portfolios.

Unauthorized Disclosure of Source Code. Source code, the detailed program commands for our operating systems

and software programs, is the most significant asset we own. While we license certain portions of our source code for

various software programs and operating systems to a number of licensees, we take significant measures to protect the

secrecy of large portions of our source code. If an unauthorized disclosure of a significant portion of our source code

occurs, we could potentially lose future trade secret protection for that source code. The loss of future trade secret

protection could make it easier for third parties to compete with our products by copying functionality, which could