Nike 2009 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2009 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

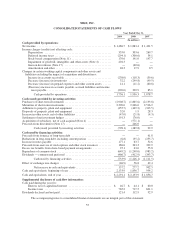

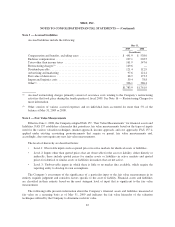

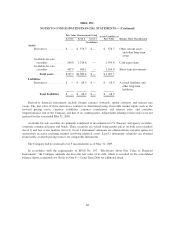

NIKE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

reporting unit’s business; and working capital effects. The market valuation approach indicates the fair value of

the business based on a comparison of the reporting unit to comparable publicly traded companies in similar lines

of business. Significant estimates in the market valuation approach model include identifying similar companies

with comparable business factors such as size, growth, profitability, risk and return on investment and assessing

comparable revenue and operating income multiples in estimating the fair value of the reporting unit.

The Company believes the weighted use of discounted cash flows and the market valuation approach is the

best method for determining the fair value of its reporting units because these are the most common valuation

methodologies used within its industry; and the blended use of both models compensates for the inherent risks

associated with either model if used on a stand-alone basis.

Indefinite-lived intangible assets primarily consist of acquired trade names and trademarks. In measuring the

fair value for these intangible assets, the Company utilizes the relief-from-royalty method. This method assumes

that trade names and trademarks have value to the extent that their owner is relieved of the obligation to pay

royalties for the benefits received from them. This method requires the Company to estimate the future revenue

for the related brands, the appropriate royalty rate and the weighted average cost of capital.

Foreign Currency Translation and Foreign Currency Transactions

Adjustments resulting from translating foreign functional currency financial statements into U.S. dollars are

included in the foreign currency translation adjustment, a component of accumulated other comprehensive

income in shareholders’ equity.

The Company’s global subsidiaries have various assets and liabilities, primarily receivables and payables,

that are denominated in currencies other than their functional currency. These balance sheet items are subject to

remeasurement under SFAS No. 52, “Foreign Currency Translation,” (“FAS 52”), the impact of which is

recorded in other (income) expense, net, within our consolidated statements of income.

Accounting for Derivatives and Hedging Activities

The Company uses derivative financial instruments to limit exposure to changes in foreign currency

exchange rates and interest rates. The Company accounts for derivatives pursuant to SFAS No. 133, “Accounting

for Derivative Instruments and Hedging Activities,” as amended and interpreted (“FAS 133”). FAS 133

establishes accounting and reporting standards for derivative instruments and requires all derivatives be recorded

at fair value on the balance sheet. Changes in the fair value of derivative financial instruments are either

recognized in other comprehensive income (a component of shareholders’ equity), debt or net income depending

on the underlying exposure being hedged and the extent to which the derivative is effective.

See Note 18 — Risk Management and Derivatives for more information on the Company’s risk

management program and derivatives.

Stock-Based Compensation

On June 1, 2006, the Company adopted SFAS No. 123R “Share-Based Payment” (“FAS 123R”), which

requires the Company to record expense for stock-based compensation to employees using a fair value method.

Under FAS 123R, the Company estimates the fair value of options granted under the NIKE, Inc. 1990 Stock

Incentive Plan (the “1990 Plan”) and employees’ purchase rights under the Employee Stock Purchase Plans

(“ESPPs”) using the Black-Scholes option pricing model. The Company recognizes this fair value, net of

estimated forfeitures, as selling and administrative expense in the consolidated statements of income over the

vesting period using the straight-line method.

60