Nike 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

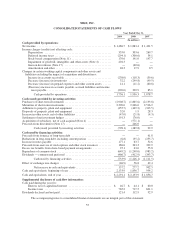

NIKE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Recently Adopted Accounting Standards

On December 1, 2008, the Company adopted Statement of SFAS No. 161, “Disclosures about Derivative

Instruments and Hedging Activities — an amendment of FASB Statement No.133” (“FAS 161”), which provides

revised guidance for enhanced disclosures about how and why an entity uses derivative instruments, how

derivative instruments and the related hedged items are accounted for under FAS 133, and how derivative

instruments and the related hedged items affect an entity’s financial position, financial performance and cash

flows. The adoption of FAS 161 did not have an impact on the Company’s consolidated financial position or

results of operations. For additional information, see Note 18 — Risk Management and Derivatives.

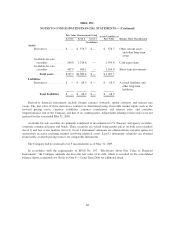

On June 1, 2008, the Company adopted SFAS No. 157, “Fair Value Measurements” (“FAS 157”) for

financial assets and liabilities, which clarifies the meaning of fair value, establishes a framework for measuring

fair value and expands disclosures about fair value measurements. Fair value is defined under FAS 157 as the

exchange price that would be received for an asset or paid to transfer a liability in the principal or most

advantageous market for the assets or liabilities in an orderly transaction between market participants on the

measurement date. Subsequent changes in fair value of these financial assets and liabilities are recognized in

earnings or other comprehensive income when they occur. The effective date of the provisions of FAS 157 for

non-financial assets and liabilities, except for items recognized at fair value on a recurring basis, was deferred by

Financial Accounting Standards Board (“FASB”) Staff Position FAS 157-2 (“FSP FAS 157-2”) and are effective

for the fiscal year beginning June 1, 2009. The adoption of FAS 157 for financial assets and liabilities did not

have an impact on the Company’s consolidated financial position or results of operations. The adoption of FAS

157 for non-financial assets and liabilities is not expected to have an impact on the Company’s consolidated

financial position or results of operations. For additional information on the fair value of financial assets and

liabilities, see Note 6 — Fair Value Measurements.

Also effective June 1, 2008, the Company adopted SFAS No. 159, “The Fair Value Option for Financial

Assets and Financial Liabilities” (“FAS 159”), which allows an entity the irrevocable option to elect fair value

for the initial and subsequent measurement for certain financial assets and liabilities on a contract-by-contract

basis. As of May 31, 2009, the Company has not elected the fair value option for any additional financial assets

and liabilities beyond those already prescribed by accounting principles generally accepted in the United States.

In October 2008, the FASB issued Staff Position No. FAS 157-3, “Determining the Fair Value of a

Financial Asset in a Market That Is Not Active” (“FSP FAS 157-3”). FSP FAS 157-3 clarifies the application of

FAS 157 in a market that is not active and defines additional key criteria in determining the fair value of a

financial asset when the market for that financial asset is not active. FSP FAS 157-3 applies to financial assets

within the scope of accounting pronouncements that require or permit fair value measurements in accordance

with FAS 157. FSP FAS 157-3 was effective upon issuance and the application of FSP FAS 157-3 did not have a

material impact on the Company’s consolidated financial statements.

Recently Issued Accounting Standards

In May 2009, the FASB issued SFAS No. 165, “Subsequent Events” (“FAS 165”), which establishes

general standards of accounting and disclosure for events that occur after the balance sheet date but before

financial statements are issued. The provisions of FAS 165 are effective for the quarter ending August 31, 2009.

The Company does not expect the adoption will have a material impact on its consolidated financial position or

results of operations.

In April 2009, the FASB issued Staff Position No. FAS 107-1 and APB 28-1, “Interim Disclosures about

Fair Value of Financial Instruments” (“FSP FAS 107-1 and APB 28-1”), which amends SFAS No. 107,

“Disclosures about Fair Value of Financial Instruments”, and APB Opinion No. 28, “Interim Financial

62