Nike 2009 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2009 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

NIKE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Reporting”, to require disclosures about fair value of financial instruments in interim and annual reporting

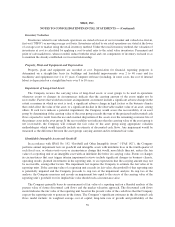

periods. The provisions of FSP FAS 107-1 and APB 28-1 are effective for the quarter ending August 31, 2009.

The Company does not expect the adoption will have an impact on its consolidated financial position or results of

operations.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“FAS

141(R)”) and SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements” (“FAS 160”).

These standards aim to improve, simplify, and converge international standards of accounting for business

combinations and the reporting of noncontrolling interests in consolidated financial statements. FAS 141(R) is

effective for business combinations for which the acquisition date is on or after June 1, 2009. Generally, the

effects of FAS 141(R) will depend on future acquisitions. FAS 160 is effective for the Company beginning

June 1, 2009. The Company does not expect the adoption of FAS 160 will have a material impact on its

consolidated financial position or results of operations.

In April 2008, the FASB issued Staff Position No. FAS 142-3, “Determination of the Useful Life of

Intangible Assets” (“FSP FAS 142-3”). FSP FAS 142-3 amends the factors that should be considered in

developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset

under FAS 142. The intent of the position is to improve the consistency between the useful life of a recognized

intangible asset under FAS 142 and the period of expected cash flows used to measure the fair value of the asset

under FAS 141(R), and other U.S. generally accepted accounting principles. The provisions of FSP FAS 142-3

are effective for the fiscal year beginning June 1, 2009. The Company does not expect the adoption of FSP FAS

142-3 will have a material impact on its consolidated financial position or results of operations.

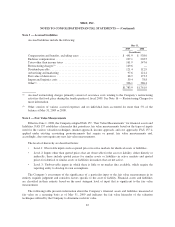

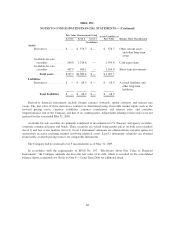

Note 2 — Inventories

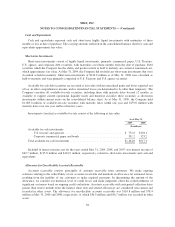

Inventory balances of $2,357.0 million and $2,438.4 million at May 31, 2009 and 2008, respectively, were

substantially all finished goods.

Note 3 — Property, Plant and Equipment

Property, plant and equipment includes the following:

As of May 31,

2009 2008

(In millions)

Land ........................................................... $ 221.6 $ 209.4

Buildings ....................................................... 974.0 934.6

Machinery and equipment .......................................... 2,094.3 2,005.0

Leasehold improvements ........................................... 802.0 757.3

Construction in process ............................................ 163.8 196.7

4,255.7 4,103.0

Less accumulated depreciation ...................................... 2,298.0 2,211.9

$1,957.7 $1,891.1

Capitalized interest was not material for the years ended May 31, 2009, 2008 and 2007.

63