Nike 2015 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2015 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

PART II

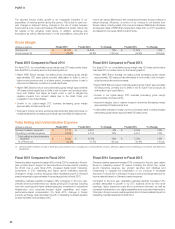

Constant currency apparel revenue growth was due to increases in nearly all

key categories, primarily Sportswear, Running and Women’s Training,

partially offset by a decline in Football (Soccer) revenues due to higher World

Cup sales in fiscal 2014. Unit sales of apparel decreased 1% while average

selling price per unit contributed approximately 6 percentage points of apparel

revenue growth. The increase in average selling price per unit was primarily

attributable to an increase in revenues from our higher-priced DTC business,

and to a lesser extent, price increases in response to inflationary conditions.

On a reported basis, EBIT decreased 14% primarily due to reported revenue

declines, lower gross margin and higher selling and administrative expense,

as well as the impact of weakening foreign currency exchange rates. Gross

margin decreased 140 basis points due to unfavorable standard foreign

currency exchange rates, higher inventory obsolescence and higher off-price

mix, partially offset by higher average selling prices. Selling and administrative

expense increased due to higher operating overhead costs, primarily to

support DTC growth, as well as higher demand creation expense, in part as a

result of support for the World Cup in early fiscal 2015 and higher sports

marketing expense.

Fiscal 2014 Compared to Fiscal 2013

Excluding changes in currency exchange rates, fiscal 2014 revenues for

Emerging Markets increased 13% as a result of growth across nearly every

territory. Our largest territory, Brazil, grew 19%, while our SOCO territory grew

25%. Mexico revenues decreased 3% largely as a result of shipping delays

caused by issues with a distribution center transition in the first half of fiscal

2014. On a category basis, revenues were higher in nearly every category, led

by Football (Soccer), Running and Sportswear.

Constant currency footwear revenue growth for fiscal 2014 was driven by

growth in nearly every key category, led by Running, Sportswear, Football

(Soccer) and Action Sports. Unit sales for fiscal 2014 increased 4% and

average selling price per pair contributed approximately 6 percentage points

of footwear revenue growth. The increase in average selling price per pair was

primarily driven by price increases, in part reflecting inflationary conditions in

certain Latin American territories, and to a lesser extent, shifts in mix to higher-

priced products.

Constant currency apparel revenue increased driven by growth in every key

category, most notably Football (Soccer) and Running. Unit sales increased

11% and average selling price per unit contributed approximately 10

percentage points of apparel revenue growth, primarily due to price

increases, in part reflecting inflationary conditions in certain Latin American

territories.

Fiscal 2014 reported EBIT decreased primarily due to a decline in gross

margin, higher selling and administrative expense and weaker currencies in a

number of developing markets. Gross margin decreased 30 basis points due

primarily to unfavorable foreign currency exchange rates, higher product

costs, higher warehousing costs related to distribution center transition

challenges in Mexico and higher discounts, which more than offset higher

average selling prices. Selling and administrative expense increased due to

higher operating overhead costs to support the expansion of our DTC

business and infrastructure investments to support growth, as well as

increases in demand creation spending to support the World Cup and key

product launches.

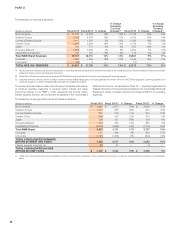

Global Brand Divisions

(Dollars in millions) Fiscal 2015 Fiscal 2014 % Change

% Change

Excluding

Currency

Changes Fiscal 2013 % Change

% Change

Excluding

Currency

Changes

Revenues $ 115 $ 125 -8% -2% $ 115 9% 6%

(Loss) Before Interest and Taxes $ (2,263) $ (1,993) 14% $ (1,716) 16%

Global Brand Divisions primarily represent demand creation, operating

overhead and product creation and design expenses that are centrally

managed for the NIKE Brand. Revenues for Global Brand Divisions are

primarily attributable to NIKE Brand licensing businesses that are not part of a

geographic operating segment.

Fiscal 2015 Compared to Fiscal 2014

Global Brand Divisions’ loss before interest and taxes increased $270 million

in fiscal 2015, primarily due to higher operating overhead reflecting continued

investments in operational infrastructure, including digital capabilities,

consumer engagement and supply chain initiatives, as well as higher

performance-based compensation. Demand creation expense increased

slightly due to support for the World Cup in the first quarter of fiscal 2015 and

key brand and consumer events.

Fiscal 2014 Compared to Fiscal 2013

For fiscal 2014, Global Brand Divisions’ loss before interest and taxes

increased $277 million, primarily driven by an increase in centrally managed

product costs, increased investments in our digital infrastructure, as well as

higher demand creation spending in the fourth quarter of fiscal 2014 to

support the World Cup and product creation and design initiatives.

Converse

(Dollars in millions) Fiscal 2015 Fiscal 2014 % Change

% Change

Excluding

Currency

Changes Fiscal 2013 % Change

% Change

Excluding

Currency

Changes

Revenues $ 1,982 $ 1,684 18% 21%$ 1,449 16% 15%

Earnings Before Interest and Taxes $ 517 $ 496 4% $ 425 17%

In territories we define as “direct distribution markets” Converse designs,

markets and sells products directly to distributors, wholesale customers and

to consumers through DTC operations. The largest direct distribution markets

are the United States, the United Kingdom and China. Converse does not

own the Converse trademarks in Japan. Territories other than direct

distribution markets and Japan are serviced by third-party licensees who pay

royalties to Converse for the use of its registered trademarks and other

intellectual property rights.

94