Nike 2015 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2015 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

PART II

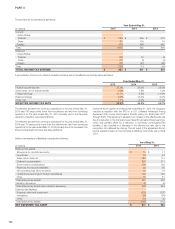

the two-step impairment test is unnecessary. The two-step impairment test

first requires the Company to estimate the fair value of its reporting units. If the

carrying value of a reporting unit exceeds its fair value, the goodwill of that

reporting unit is potentially impaired and the Company proceeds to step two

of the impairment analysis. In step two of the analysis, the Company

measures and records an impairment loss equal to the excess of the carrying

value of the reporting unit’s goodwill over its implied fair value, if any.

The Company generally bases its measurement of the fair value of a reporting

unit on a blended analysis of the present value of future discounted cash flows

and the market valuation approach. The discounted cash flows model

indicates the fair value of the reporting unit based on the present value of the

cash flows that the Company expects the reporting unit to generate in the

future. The Company’s significant estimates in the discounted cash flows

model include: its weighted average cost of capital; long-term rate of growth

and profitability of the reporting unit’s business; and working capital effects.

The market valuation approach indicates the fair value of the business based

on a comparison of the reporting unit to comparable publicly traded

companies in similar lines of business. Significant estimates in the market

valuation approach model include identifying similar companies with

comparable business factors such as size, growth, profitability, risk and return

on investment and assessing comparable revenue and operating income

multiples in estimating the fair value of the reporting unit.

Indefinite-lived intangible assets primarily consist of acquired trade names and

trademarks. The Company may first perform a qualitative assessment to

determine whether it is more likely than not that an indefinite-lived intangible

asset is impaired. If, after assessing the totality of events and circumstances,

the Company determines that it is more likely than not that the indefinite-lived

intangible asset is not impaired, no quantitative fair value measurement is

necessary. If a quantitative fair value measurement calculation is required for

these intangible assets, the Company utilizes the relief-from-royalty method.

This method assumes that trade names and trademarks have value to the

extent that their owner is relieved of the obligation to pay royalties for the

benefits received from them. This method requires the Company to estimate

the future revenue for the related brands, the appropriate royalty rate and the

weighted average cost of capital.

Operating Leases

The Company leases retail store space, certain distribution and warehouse

facilities, office space and other non-real estate assets under operating

leases. Operating lease agreements may contain rent escalation clauses, rent

holidays or certain landlord incentives, including tenant improvement

allowances. Rent expense for non-cancelable operating leases with

scheduled rent increases or landlord incentives are recognized on a straight-

line basis over the lease term, beginning with the effective lease

commencement date, which is generally the date in which the Company

takes possession of or controls the physical use of the property. Certain

leases also provide for contingent rents, which are determined as a percent of

sales in excess of specified levels. A contingent rent liability is recognized

together with the corresponding rent expense when specified levels have

been achieved or when the Company determines that achieving the specified

levels during the period is probable.

Fair Value Measurements

The Company measures certain financial assets and liabilities at fair value on a

recurring basis, including derivatives and available-for-sale securities. Fair

value is the price the Company would receive to sell an asset or pay to transfer

a liability in an orderly transaction with a market participant at the

measurement date. The Company uses a three-level hierarchy established by

the Financial Accounting Standards Board (“FASB”) that prioritizes fair value

measurements based on the types of inputs used for the various valuation

techniques (market approach, income approach and cost approach).

The levels of hierarchy are described below:

•Level 1: Quoted prices in active markets for identical assets or liabilities.

•Level 2: Inputs other than quoted prices that are observable for the asset or

liability, either directly or indirectly; these include quoted prices for similar

assets or liabilities in active markets and quoted prices for identical or similar

assets or liabilities in markets that are not active.

•Level 3: Unobservable inputs for which there is little or no market data

available, which require the reporting entity to develop its own assumptions.

The Company’s assessment of the significance of a particular input to the fair

value measurement in its entirety requires judgment and considers factors

specific to the asset or liability. Financial assets and liabilities are classified in

their entirety based on the most conservative level of input that is significant to

the fair value measurement.

Pricing vendors are utilized for certain Level 1 and Level 2 investments. These

vendors either provide a quoted market price in an active market or use

observable inputs without applying significant adjustments in their pricing.

Observable inputs include broker quotes, interest rates and yield curves

observable at commonly quoted intervals, volatilities and credit risks. The fair

value of derivative contracts is determined using observable market inputs

such as the daily market foreign currency rates, forward pricing curves,

currency volatilities, currency correlations and interest rates and considers

nonperformance risk of the Company and that of its counterparties.

The Company’s fair value processes include controls that are designed to

ensure appropriate fair values are recorded. These controls include a

comparison of fair values to another independent pricing vendor.

Refer to Note 6 — Fair Value Measurements for additional information.

Foreign Currency Translation and Foreign

Currency Transactions

Adjustments resulting from translating foreign functional currency financial

statements into U.S. Dollars are included in the foreign currency translation

adjustment, a component of Accumulated other comprehensive income in

Total shareholders’ equity.

The Company’s global subsidiaries have various assets and liabilities,

primarily receivables and payables, which are denominated in currencies

other than their functional currency. These balance sheet items are subject to

re-measurement, the impact of which is recorded in Other (income) expense,

net, within the Consolidated Statements of Income.

Accounting for Derivatives and Hedging

Activities

The Company uses derivative financial instruments to reduce its exposure to

changes in foreign currency exchange rates and interest rates. All derivatives

are recorded at fair value on the Consolidated Balance Sheets and changes in

the fair value of derivative financial instruments are either recognized in

Accumulated other comprehensive income (a component of Total

shareholders’ equity), Long-term debt or Net income depending on the

nature of the underlying exposure, whether the derivative is formally

designated as a hedge and, if designated, the extent to which the hedge is

effective. The Company classifies the cash flows at settlement from

derivatives in the same category as the cash flows from the related hedged

items. For undesignated hedges and designated cash flow hedges, this is

primarily within the Cash provided by operations component of the

Consolidated Statements of Cash Flows. For designated net investment

hedges, this is within the Cash used by investing activities component of the

Consolidated Statement of Cash Flows. For the Company’s fair value

116