Proctor and Gamble 2012 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2012 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

42 The Procter & Gamble Company

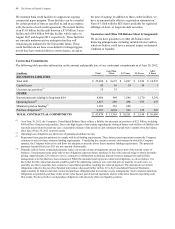

discounted basis, the discount rate impacts our plan

obligations and expenses. Discount rates used for our U.S.

defined benefit pension and OPEB plans are based on a yield

curve constructed from a portfolio of high quality bonds for

which the timing and amount of cash outflows approximate

the estimated payouts of the plan. For our international

plans, the discount rates are set by benchmarking against

investment grade corporate bonds rated AA or better. The

average discount rate on the defined benefit pension plans

and OPEB plans of 4.2% and 4.3% respectively, represents a

weighted average of local rates in countries where such

plans exist. A 100-basis point change in the pension discount

rate would impact annual after-tax defined benefit pension

expense by approximately $160 million. A change in the

OPEB discount rate of 100 basis points would impact annual

after-tax OPEB expense by approximately $70 million. For

additional details on our defined benefit pension and OPEB

plans, see Note 8 to the Consolidated Financial Statements.

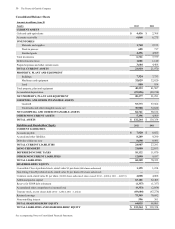

Acquisitions, Goodwill and Intangible Assets

We account for acquired businesses using the acquisition

method of accounting. Under the purchase method, our

Consolidated Financial Statements reflect the operations of

an acquired business starting from the completion of the

acquisition. In addition, the assets acquired and liabilities

assumed are recorded at the date of acquisition at their

respective estimated fair values, with any excess of the

purchase price over the estimated fair values of the net assets

acquired recorded as goodwill.

Significant judgment is required in estimating the fair value

of intangible assets and in assigning their respective useful

lives. Accordingly, we typically obtain the assistance of

third-party valuation specialists for significant tangible and

intangible assets. The fair value estimates are based on

available historical information and on future expectations

and assumptions deemed reasonable by management, but are

inherently uncertain.

We typically use an income method to estimate the fair value

of intangible assets, which is based on forecasts of the

expected future cash flows attributable to the respective

assets. Significant estimates and assumptions inherent in the

valuations reflect a consideration of other marketplace

participants, and include the amount and timing of future

cash flows (including expected growth rates and

profitability), the underlying product or technology life

cycles, economic barriers to entry, a brand's relative market

position and the discount rate applied to the cash flows.

Unanticipated market or macroeconomic events and

circumstances may occur, which could affect the accuracy or

validity of the estimates and assumptions.

Determining the useful life of an intangible asset also

requires judgment. Certain brand intangibles are expected to

have indefinite lives based on their history and our plans to

continue to support and build the acquired brands. Other

acquired intangible assets (e.g., certain trademarks or brands,

customer relationships, patents and technologies) are

expected to have determinable useful lives. Our assessment

as to brands that have an indefinite life and those that have a

determinable life is based on a number of factors including

competitive environment, market share, brand history,

underlying product life cycles, operating plans and the

macroeconomic environment of the countries in which the

brands are sold. Our estimates of the useful lives of

determinable-lived intangibles are primarily based on these

same factors. All of our acquired technology and customer-

related intangibles are expected to have determinable useful

lives.

The costs of determinable-lived intangibles are amortized to

expense over their estimated life. The value of indefinite-

lived intangible assets and residual goodwill is not

amortized, but is tested at least annually for impairment. Our

impairment testing for goodwill is performed separately

from our impairment testing of indefinite-lived intangibles.

We test goodwill for impairment by reviewing the book

value compared to the fair value at the reportable unit level.

We test individual indefinite-lived intangibles by reviewing

the individual book values compared to the fair value. We

determine the fair value of our reporting units and indefinite-

lived intangible assets based on the income approach. Under

the income approach, we calculate the fair value of our

reporting units and indefinite-lived intangible assets based

on the present value of estimated future cash flows.

Considerable management judgment is necessary to evaluate

the impact of operating and macroeconomic changes and to

estimate future cash flows to measure fair value.

Assumptions used in our impairment evaluations, such as

forecasted growth rates and cost of capital, are consistent

with internal projections and operating plans. We believe

such assumptions and estimates are also comparable to those

that would be used by other marketplace participants. When

certain events or changes in operating conditions occur,

indefinite-lived intangible assets may be reclassified to a

determinable life asset and an additional impairment

assessment may be performed.

During the second quarter of fiscal 2012, we changed our

annual goodwill impairment testing date from July 1 to

October 1 of each year. This change was made to better align

the timing of our annual impairment testing with the timing

of the Company's annual strategic planning process. We

tested goodwill for impairment as of July 1, 2011 (the testing

date under our previous policy) and no impairments were

indicated. The results of our impairment testing during the

quarter ended December 31, 2011, indicated that the

estimated fair values of our Appliances and Salon

Professional reporting units were less than their respective

carrying amount therefore we recorded a non-cash before

and after tax impairment charge of $1.3 billion.

Additionally, our impairment testing for indefinite lived

intangible assets during the quarter ended December 31,

2011 indicated a decline in the fair value of our Koleston

Perfect and Wella trade name intangible assets below their

respective carrying values. This resulted in a non-cash

before tax impairment charge of $246 million ($173 million