Target 2005 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

17

Executive Summary

Target Corporation (the Corporation or Target) operates large-format

general merchandise discount stores in the United States. Our credit

card operation represents an integral component of our core retail

business. Through our branded proprietary credit (or REDcard)

products, we strengthen the bond with our guests, drive incremental

sales and contribute meaningfully to earnings. We also operate

Target.com, an online business which is small relative to our overall

size, but is growing at a much more rapid annual pace than our stores

and provides important benefits to our stores and to our credit card

operation.

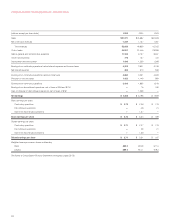

Fiscal 2005 was a year of excellent sales and earnings growth

for Target. Earnings from continuing operations grew 27.7 percent to

$2,408 million and, on this same basis, diluted earnings per share

rose 31.0 percent to $2.71. Comparable-store sales increased

5.6 percent and our credit contribution to EBIT increased 32.8 percent

to $645 million. The combination of strong sales performance, gross

margin rate expansion and enhanced contribution from our credit

card operation produced EBIT of $4,323 million, an increase of more

than 20 percent from 2004.

We are committed to consistently delighting our guests, providing

a workplace that is preferred by our team members and investing to

improve the quality of life in communities where we operate. In this

way, we believe we will continue to achieve profitable market share

growth and deliver superior shareholder value for many years to come.

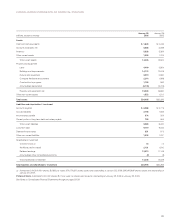

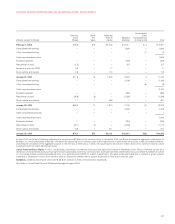

Management’s Discussion and Analysis is based on our

Consolidated Financial Statements, pages 24-27.

Analysis of Continuing Operations

Revenues and

Comparable-Store Sales

Sales include merchandise sales, net of

expected returns, from our stores and

our online business, as well as gift card

breakage revenue. Refer to Note 2,

pages 28-29 for a definition of breakage

revenue. Total revenues include sales

and net credit card revenues (income

from finance charges, late fees and other

revenues from our proprietary credit card

products). Total revenues do not include

sales tax as we consider ourselves a

pass-through conduit for collecting and

remitting sales taxes. Comparable-store sales are sales from stores

open longer than one year, including stores that have relocated and

general merchandise stores that have been remodeled. Comparable-

store sales do not include sales from general merchandise stores that

have been converted to a SuperTarget store format in the past twelve

months, sales from stores that were intentionally closed to be

remodeled or sales from our online business. The method of

calculating comparable-store sales varies across the retail industry.

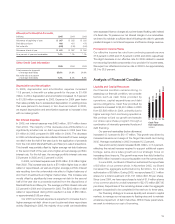

Revenue Growth

2005 2004 2003

Comparable-store sales 5.6% 5.3% 4.4%

Other sales factors (a) 6.6% 6.3% 7.7%

Total sales 12.2% 11.6% 12.1%

Net credit card revenues 16.5% 5.5% 23.2%

Total revenues 12.3% 11.5% 12.3%

(a) Principally contributions from new stores.

Comparable-store sales growth in 2005 and 2004 was

attributable to growth in both average transaction amount and the

number of transactions in comparable stores. In 2006, we expect

to generate a low-double-digit percentage increase in revenues,

reflecting contribution from new store expansion, continued growth

in comparable-store sales due to increases in average transaction

amount and the number of transactions in comparable stores and

growth in net credit card revenues. In 2005, there was essentially no

impact of inflation/deflation on sales growth, compared to a

deflationary impact of approximately 1 percent in 2004 and 4 percent

in 2003. We do not expect inflation/ deflation to have a significant

effect on sales growth in 2006.

Gross Margin Rate

Gross margin rate represents gross margin (sales less cost of sales)

as a percent of sales. Cost of sales includes purchases, markdowns,

inventory shrink, and other costs associated with our merchandise, as

well as all freight to our stores and global sourcing costs. These costs

are partially offset by various forms of consideration earned from our

vendors, referred to as “vendor income.” Refer to Critical Accounting

Estimates, page 22.

In 2005, our consolidated gross margin rate increased

0.7 percentage points to a rate of 31.9 percent. This change in gross

margin rate primarily reflected an improvement in markup, including an

increase in direct import penetration, as well as favorable inventory

shrinkage performance. Refer to Critical Accounting Estimates,

page 22, for further discussion of cost of sales. Markup is the

difference between an item’s cost and its retail price (expressed as a

percentage of its retail price). Factors that affect markup include

vendor offerings and negotiations, vendor income, sourcing strategies,

market forces like the cost of raw materials and freight and competitive

influences. The definition and method of calculating markup and gross

margin varies across the retail industry.

In 2004, our consolidated gross margin rate increased by

0.6 percentage points to a rate of 31.2 percent primarily due to an

increase in markup, including an increase in direct import penetration.

MANAGEMENT’S DISCUSSION AND ANALYSIS

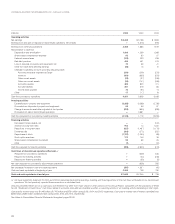

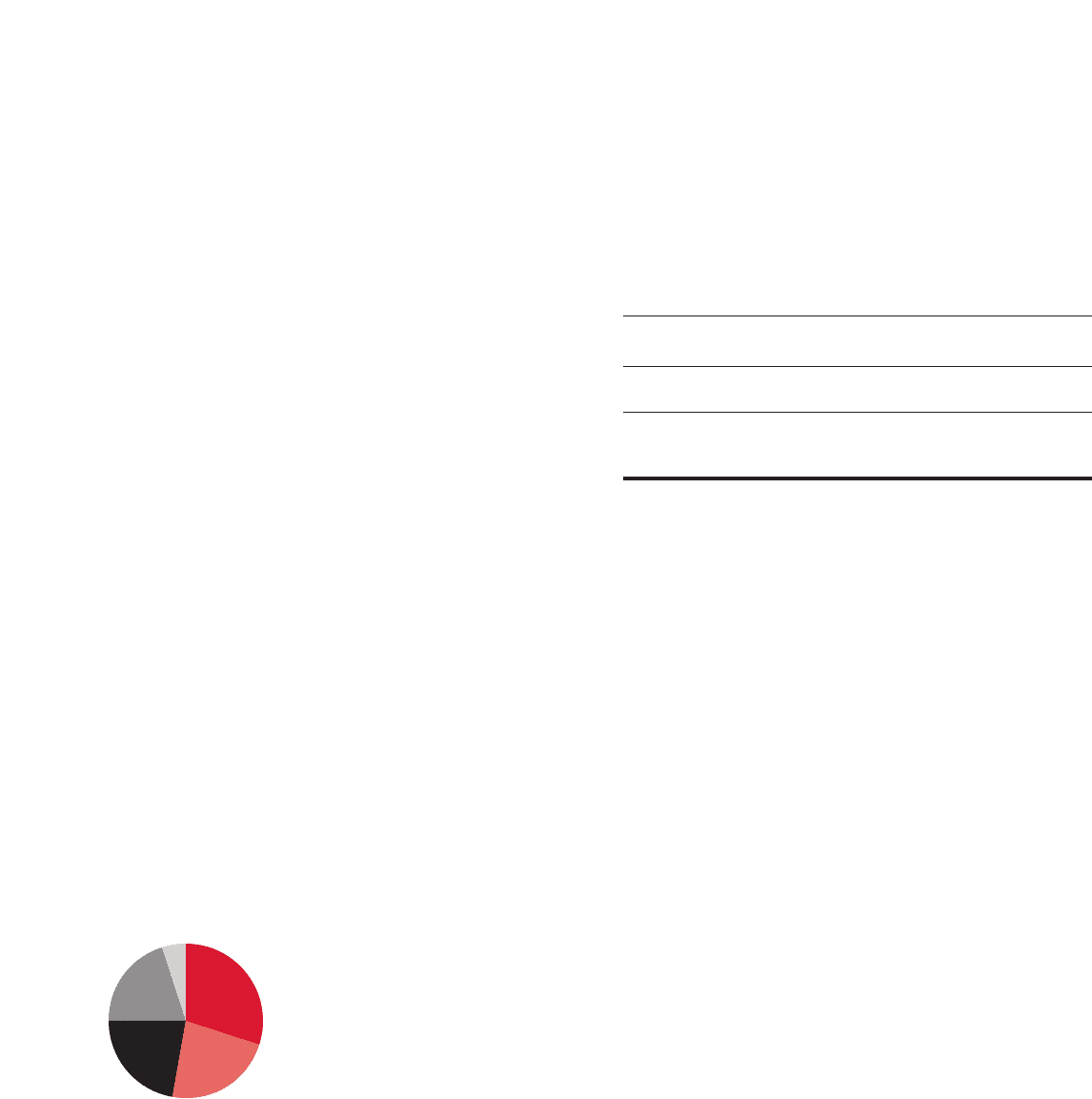

2005 Sales Mix

($51.3 billion)

• Consumables & Commodities

• Electronics, Entertainment,

• Sporting Goods & Toys

• Apparel & Accessories

• Home Furnishings & Décor

• Other

23%

20%

5%

30%

22%