Target 2005 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46

|

|

37

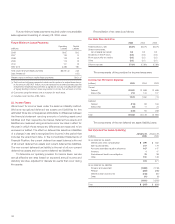

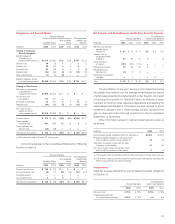

Obligations and Funded Status

Pension Benefits Postretirement

Non-qualified Health Care

Qualified Plans Plans Benefits

(millions) 2005 2004 2005 2004 2005 2004

Change in Projected

Benefit Obligation

Benefit obligation

at beginning of

measurement period (a) $1,515 $1,333 $ 34 $ 29 $ 107 $ 123

Service cost 66 78 1123

Interest cost 85 82 2267

Actuarial loss 55 68 443(6)

Benefits paid (94) (65) (5) (3) (13) (13)

Plan amendments (1) 19 (3) 1—(7)

Benefit obligation at end

of measurement period $1,626 $1,515 $ 33 $ 34 $ 105 $ 107

Change in Plan Assets

Fair value of plan assets

at beginning of

measurement period $1,698 $1,405 $— $— $— $—

Actual return on

plan assets 174 157 ————

Employer contribution 67 201 5313 13

Benefits paid (94) (65) (5) (3) (13) (13)

Fair value of plan

assets at end of

measurement period $1,845 $1,698 $— $— $— $—

Funded status $ 219 $ 183 $(33) $(34) $(105) $(107)

Unrecognized

actuarial loss 561 584 16 15 86

Unrecognized prior

service cost (32) (39) —2——

Net amount recognized $ 748 $ 728 $(17) $(17) $ (97) $(101)

(a) Measurement date is October 31 of each year.

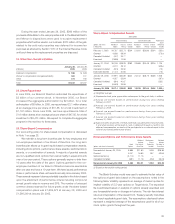

Amounts recognized in the Consolidated Statements of Financial

Position consist of:

Pension Benefits Postretirement

Non-qualified Health Care

Qualified Plans Plans Benefits

(millions) 2005 2004 2005 2004 2005 2004

Prepaid benefit cost $ 752 $ 733 $— $— $— $—

Accrued benefit cost (9) (11) (22) (24) (97) (101)

Intangible assets ———2——

Accumulated OCI 5655——

Net amount recognized $ 748 $ 728 $(17) $(17) $ (97) $(101)

Net Pension and Postretirement Health Care Benefits Expense

Postretirement

Pension Benefits Health Care Benefits

(millions) 2005 2004 2003 2005 2004 2003

Service cost benefits

earned during

the period $ 67 $ 79 $ 74 $ 2 $3 $2

Interest cost on

projected benefit

obligation 87 84 75 678

Expected return

on assets (137) (122) (114) ———

Recognized losses 43 36 18 111

Recognized prior

service cost (5) (7) (7) ———

Settlement/ curtailment

charges —1——(7) —

Total $ 55 $ 71 $ 46 $ 9 $ 4 $11

The amortization of any prior service cost is determined using

the straight-line method over the average remaining service period

of employees expected to receive benefits under the plan. As a result

of freezing the benefits for Marshall Field’s and Mervyn’s team

members at the time of their respective dispositions and retaining the

related assets and obligations of the plans, we were required to record

curtailment charges in 2004. These charges are also included in the

gain on disposal of discontinued operations in the Consolidated

Statements of Operations.

Other information related to defined benefit pension plans is

as follows:

(millions) 2005 2004

Accumulated benefit obligation (ABO) for all plans (a) $1,534 $1,501

Projected benefit obligation for pension plans

with an ABO in excess of plan assets (b) 46 49

Total ABO for pension plans with an ABO

in excess of plan assets 41 45

Fair value of plan assets for pension plans

with an ABO in excess of plan assets 35

(a) The present value of benefits earned to date assuming no future salary growth.

(b) The present value of benefits earned to date by plan participants, including the

effect of assumed future salary increases.

Assumptions

Weighted average assumptions used to determine benefit obligations

at October 31:

Postretirement

Pension Benefits Health Care Benefits

2005 2004 2005 2004

Discount rate 5.75% 5.75% 5.75% 5.75%

Average assumed rate

of compensation increase 3.50% 2.75% n/a n/a