Target 2005 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

18

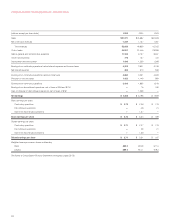

We expect our consolidated gross margin rate in 2006 to be

approximately equal to our 2005 rate as potential opportunities to

increase gross margin are expected to approximately offset potential

pressures. The factors affecting our outlook include: our introduction

of new merchandising strategies, our growth in direct imports and

our ability to leverage our increasing scale, offset by the competitive

pricing environment and the more rapid pace of growth of lower

margin categories, like consumables and commodities.

Selling, General and Administrative Expense Rate

Our SG&A expense rate represents payroll, benefits, advertising,

distribution, buying and occupancy, start-up and other expenses as

a percentage of sales. SG&A expenses exclude depreciation and

amortization and expenses associated with our credit card operation,

which are reflected separately in our Consolidated Statements of

Operations. In 2005, 2004 and 2003 approximately $110 million,

$72 million and $58 million, respectively, of vendor income was recorded

as an offset to SG&A expenses because it represented reimbursement

for specific, incremental and identifiable advertising costs.

In 2005, our consolidated SG&A expense rate increased to

21.8 percent compared to 21.4 percent in 2004. The expense rate

increase was due to several factors, including the year-over-year

impact of reduced transition services income related to our 2004

divestitures of Marshall Field’s and Mervyn’s, higher utilities expense

and the effects of stronger year-over-year performance on incentive

and share-based compensation expense. Some of the expense rate

increase can also be attributed to growth in marketing expenses for

which the corresponding vendor income is recorded as a reduction of

inventory costs because it did not meet the criteria required for

recording it as an element of SG&A expenses. The combination of

all unfavorable expense items more than offset the year-over-year

favorability from last year’s lease accounting adjustment.

In 2004, our consolidated SG&A expense rate rose to

21.4 percent compared to 21.2 percent in 2003. Approximately half

of this year-over-year increase was attributable to a lease expense

adjustment that synchronized our straight-line expense term with the

depreciable lives of the associated assets. See further discussion in

Note 29, page 39. The primary driver of the remaining increase was

higher workers’ compensation costs.

In 2006, we expect our SG&A expense rate to be approximately

equal to our 2005 rate.

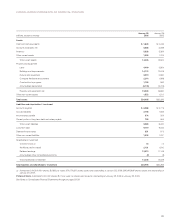

Credit Card Contribution

We offer credit to qualified guests through our REDcard products,

including the Target Visa and Target Card. Our credit card revenues

are finance charges, late fees and other revenues. In addition, we

receive third-party merchant fees from merchants who accept the

Target Visa credit card. In 2005 and 2004, our net credit card revenues

increased due to continued growth in the Target Visa portfolio. In 2005,

growth in net credit card revenues was also attributable to higher

interest rates, as a majority of our receivables are assessed finance

charges at a prime-based floating rate. Credit card expenses include

a bad debt provision, as well as operations and marketing expenses

supporting our credit card portfolio. In 2005 versus 2004, our bad

debt provision grew at a slower pace than our average receivables

balance due to the aging of the portfolio and the favorable macro-

economic credit card environment. However, our total reserve balance

as a percentage of average receivables increased in 2005 as we

reserve for the expected effects of the mandated increases in

minimum payments for certain guests. Our net write-offs as a

percentage of average receivables and our delinquency rates

continued to improve, despite a significant increase in bankruptcy

filings in advance of the October 2005 effective date of the related

federal bankruptcy legislation. Operations and marketing expenses

increased primarily due to the growth of the Target Visa portfolio.

The contribution from our credit card operation to EBIT includes

finance charge revenue, late fees, other revenue, intracompany and

third party merchant fees, less bad debt provision and operations

and marketing expenses.

We expect our 2006 credit card receivables to grow in line with

2006 sales, and we expect our overall credit card performance to

remain strong. The improvement in our delinquency rates is not

expected to continue throughout 2006 as we cycle the effects of the

October 2005 bankruptcy legislation and experience the effects of

the mandated increases in minimum payments for certain guests.

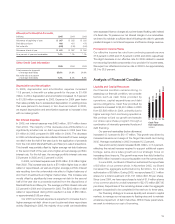

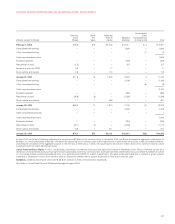

Credit Card Contribution to EBIT

(millions) 2005 2004 2003

Revenues:

Finance charges, late fees

and other revenues $1,225 $1,059 $1,015

Merchant fees

Intracompany 72 65 49

Third-party 124 98 82

Total revenues 1,421 1,222 1,146

Expenses:

Bad debt provision 466 451 476

Operations and marketing 310 286 246

Total expenses 776 737 722

Pre-tax credit card contribution to EBIT $ 645 $ 485 $ 424

As a percent of average receivables 11.6% 9.8% 9.1%

Receivables

(millions) 2005 2004 2003

Year-end receivables $6,117 $5,456 $4,973

Average receivables $5,544 $4,927 $4,661

Accounts with three or more

payments past due as a percent

of year-end receivables 2.8% 3.5% 4.2%