Target 2005 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

|

|

31

In accordance with SFAS No.144, “Accounting for the Impairment

or Disposal of Long-Lived Assets,” all long-lived assets are reviewed

when events or changes in circumstances indicate that the asset’s

carrying value may not be recoverable. No material impairments were

recorded in 2005, 2004 or 2003 as a result of the tests performed.

In March 2005, the FASB issued FASB Interpretation No. 47,

“Accounting for Conditional Asset Retirement Obligations, an

interpretation of FASB Statement No.143” (FIN 47). The primary

purpose of FIN 47 is to clarify that an entity is required to recognize a

liability for the fair value of a conditional asset retirement obligation

when incurred if the liability’s fair value can be reasonably estimated.

FIN 47 is effective no later than the end of fiscal years ending after

December 15, 2005. The adoption of this guidance did not have a

material impact on our net earnings, cash flows or financial position.

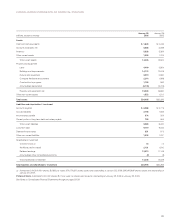

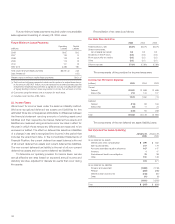

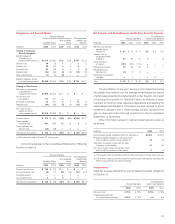

14. Other Non-Current Assets

January 28, January 29,

(millions) 2006 2005

Prepaid pension expense $ 752 $ 733

Cash value of life insurance 524 446

Goodwill and intangible assets 183 206

Other 93 126

Total $1,552 $1,511

15. Goodwill and Intangible Assets

Goodwill and intangible assets are recorded within other non-current

assets at cost less accumulated amortization. Goodwill and intangible

assets by major classes were as follows:

Leasehold

Acquisition

Goodwill Costs Other Total

Jan. 28, Jan.29, Jan. 28, Jan.29, Jan. 28, Jan.29, Jan. 28, Jan.29,

(millions) 2006 2005 2006 2005 2006 2005 2006 2005

Gross asset $ 80 $ 80 $ 182 $ 185 $ 205 $ 201 $ 467 $ 466

Accumulated

amortization (20) (20) (70) (52) (194) (188) (284) (260)

Net goodwill

and intangible

assets $ 60 $ 60 $ 112 $ 133 $ 11 $ 13 $ 183 $ 206

Amortization is computed on intangible assets with definite useful

lives using the straight-line method over estimated useful lives that

range from three to 29 years. Amortization expense for the years

2005, 2004 and 2003 was $25 million, $27 million and $30 million,

respectively. The estimated aggregate amortization expense of our

definite-lived intangible assets for each of the five succeeding fiscal

years is as follows:

(millions) 2006 2007 2008 2009 2010

Amortization expense $23 $20 $19 $19 $17

We have goodwill and certain intangible assets that are not

amortized but instead are subject to an annual impairment test.

Discounted cash flow models are used in determining fair value for

the purposes of the required annual impairment analysis. No material

impairments were recorded in 2005, 2004 and 2003 as a result of

the tests performed.

During 2004, goodwill with an approximate carrying value of

$63 million was disposed of as part of the Marshall Field’s transaction.

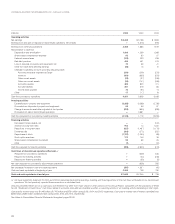

16. Accounts Payable

Our accounting policy is to reduce accounts payable when checks

to vendors clear the bank from which they were drawn. Outstanding

checks included in accounts payable were $645 million and

$992 million at year-end 2005 and 2004, respectively.

17. Accrued Liabilities

January 28, January 29,

(millions) 2006 2005

Wages and benefits $ 506 $ 422

Taxes payable 366 287

Gift card liability 294 214

Other 1,027 710

Total $2,193 $1,633

Taxes payable consist of real estate, employee withholdings and sales tax liabilities.

Gift card liability represents the amount of gift cards that have been issued but have

not been redeemed, net of estimated breakage.

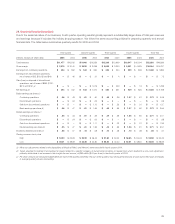

18. Commitments and Contingencies

At January 28, 2006, our obligations included notes and debentures

of $9,771 million (further discussed in Note 19, page 32), the present

value of capital lease obligations of $101 million and total future

payments of operating leases with total contractual lease payments

of $3,097 million, including certain options for lease term extension

that are expected to be exercised in the amount of $1,421 million

and $122 million of legally binding minimum lease payments for stores

that will open in 2006 (see additional detail in Note 22, pages 33-34).

In addition, real estate obligations, including commitments for the

purchase, construction, or remodeling of real estate and facilities,

were approximately $838 million at January 28, 2006. Purchase

obligations, which include all legally binding contracts such as firm

commitments for inventory purchases, merchandise royalties,

purchases of equipment, marketing-related contracts, software

acquisition/license commitments and service contracts and were

$1,431 million at January 28, 2006. In the normal course of business

we issue purchase orders to purchase inventory, which represent

authorizations to purchase and are cancelable by their terms. We do

not consider purchase orders to be firm inventory commitments. We

also issue letters of credit in the ordinary course of business which

are not firm commitments as they are conditional on the purchase

order not being cancelled. If under certain circumstances, and at our

sole discretion, we choose to cancel a purchase order, we may be