Target 2005 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

21

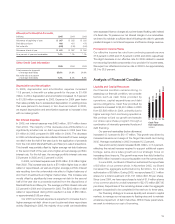

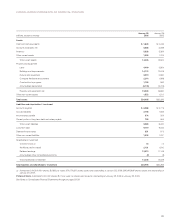

Commitments and Contingencies

At January 28, 2006, our debt, lease, real estate and purchase

contractual obligations were as follows:

Contractual Obligations

Payments Due by Period

Less than 1–3 3– 5 After 5

(millions) Total 1 Year Years Years Years

Long-term debt (a) $9,792 $751 $2,772 $2,987 $3,282

Interest payments –

long-term debt (b) 4,274 557 929 692 2,096

Capital lease

obligations 223 12 25 26 160

Operating leases (c) 3,097 137 255 221 2,484

Real estate obligations 838 818 20 — —

Purchase obligations 1,431 431 434 222 344

Standby letters of credit (d) 104 102 2 — —

Contractual cash

obligations $19,759 $2,808 $4,437 $4,148 $8,366

(a) Required principal payments only. Excludes SFAS No.133, “Accounting for

Derivative Instruments and Hedging Activities,” fair market value adjustments

recorded in long-term debt.

(b) Includes payments on $1,650 million of floating rate long-term debt secured by

credit card receivables, $750 million of which matures in 2007 and $900 million

of which matures in 2010. These payments are calculated assuming rates of

approximately 5 percent for each year outstanding. Excludes payments received

or made related to interest rate swaps discussed on page 33.

(c) Total contractual lease payments include certain options to extend the lease term,

in the amount of $1,421 million, that are expected to be exercised because the

investment in leasehold improvements is significant and also includes $122 million

of legally binding minimum lease payments for stores opening in 2006. Refer to

Note 22, pages 33-34, for further discussion of leases, including a definition of

what is included in and excluded from rent expense.

(d) Primarily related to the portion of our insurance claims for which we have retained

the risk.

Real estate obligations include commitments for the purchase,

construction or remodeling of real estate and facilities. Purchase

obligations include all legally binding contracts such as firm minimum

commitments for inventory purchases, merchandise royalties,

purchases of equipment, marketing-related contracts, software

acquisition/license commitments and service contracts.

In the normal course of business we issue purchase orders to

purchase inventory, which represent authorizations to purchase and

are cancelable by their terms. We do not consider purchase orders

to be firm inventory commitments and therefore they are excluded

from the table above. We also issue letters of credit in the ordinary

course of business which are excluded from this table as these

obligations are conditional on the purchase order not being cancelled.

If under certain circumstances, and at our sole discretion, we choose

to cancel a purchase order, we may be obligated to reimburse the

vendor for unrecoverable outlays incurred prior to cancellation.

We have not included obligations under our pension and post-

retirement health care benefit plans in the contractual obligations table

above. Our historical practice regarding these plans has been to

contribute amounts necessary to satisfy minimum pension funding

requirements plus periodic discretionary amounts determined to be

appropriate. Further information on these plans, including our expected

contributions for 2006, is addressed in Note 28 on pages 36-38.

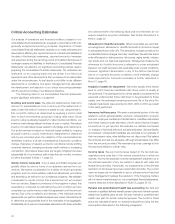

Market Risk

Our exposure to market risk results primarily from interest rate changes

on our debt obligations and on our credit card receivables, the majority

of which are now assessed finance charges at a prime-based floating

rate. At the end of 2005, our level of floating-rate debt obligations

approximated our level of floating-rate credit card assets. As a result,

based on our balance sheet position at January 28, 2006, interest

rate changes would have approximately offsetting impacts on our net

interest expense and finance charge revenues. To preserve our net

interest margin, we intend to maintain sufficient levels of floating-rate

debt to generate parallel changes in net interest expense as finance

charge revenues fluctuate. See further discussion in Note 21, page 33.

In addition, we are exposed to fluctuations of market returns on

our qualified defined benefit pension and non-qualified defined

contribution plans. The annualized effect of a one percentage point

decrease in the return on pension plan assets would decrease plan

assets by $19 million at January 28, 2006. The resulting impact on

net pension expense would be calculated consistent with the

provisions of SFAS No. 87, “Employers’ Accounting for Pensions.”

See further discussion in Note 28, pages 36-38. The annualized effect

of a one percentage point change in market returns on our non-

qualified defined contribution plans (inclusive of the effect of the

investment vehicles used to manage our economic exposure) would

not be significant. See further discussion in Note 27, page 36.

We do not have significant direct exposure to foreign currency

rates as all of our stores are located in the United States and the vast

majority of imported merchandise is purchased in U.S. dollars.

Overall, there have been no material changes in our primary risk

exposures or management of market risks since the prior year.

Analysis of Discontinued Operations

Marshall Field’s and Mervyn’s were divested in 2004; no financial results

of discontinued operations are included for the year ended January 28,

2006. In 2004, revenues and earnings from discontinued operations

reflected only a partial year of results and excluded the holiday season.

For the years ended January 29, 2005 and January 31, 2004, total

revenues included in discontinued operations were $3,095 million

and $6,138 million, respectively, and earnings from discontinued

operations were $75 million and $190 million, net of taxes of $46 million

and $116 million, respectively. In addition, we recorded a gain on the

sale of discontinued operations of $1,238 million, net of taxes of

$761 million, during the year ended January 29, 2005.