Target 2005 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

|

|

30

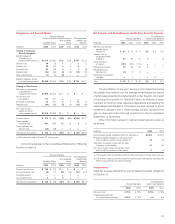

9. Cash Equivalents

Cash equivalents include highly liquid investments with an original

maturity of three months or less from the time of purchase. We carry

these investments at cost, which approximates market value. These

investments were $1,172 million and $1,732 million in 2005 and 2004,

respectively. Also included in cash equivalents are proceeds due from

credit and debit card transactions with settlement terms of less than

five days. Credit and debit card receivables included within cash

equivalents were $285 million and $242 million, respectively, for 2005

and 2004.

10. Accounts Receivable

Accounts receivable are recorded net of an allowance for expected

losses. The allowance, recognized in an amount equal to the

anticipated future write-offs based on delinquencies, risk scores, aging

trends, industry risk trends and our historical experience, was

$451 million at January 28, 2006 and $387 million at January 29,

2005. Substantially all accounts continue to accrue finance charges

until they are written off. Accounts are written off when they become

180 days past due.

In 2004, we chartered Target Bank for the purpose of issuing

credit cards to qualified businesses, as our Target National Bank

charter does not allow for the issuance of commercial credit cards.

As a method of providing funding for our accounts receivable,

we sell on an ongoing basis all of our consumer credit card receivables

to Target Receivables Corporation (TRC), a wholly-owned bankruptcy

remote subsidiary. TRC then transfers the receivables to the Target

Credit Card Master Trust (the Trust), which from time to time will sell

debt securities to third parties, either directly or through a related

trust. These debt securities represent undivided interests in the Trust

assets. TRC has also retained an undivided interest in the Trust’s

assets that are not represented by the debt securities sold to third

parties and a 2 percent undivided interest in the Trust assets that is

held by Target National Bank, a wholly-owned subsidiary of Target

which also services receivables. TRC uses the proceeds from the

sale of debt securities and its share of collections on the receivables

to pay the purchase price of the receivables to Target.

The accounting guidance for such transactions, SFAS No.140,

“Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities (a replacement of SFAS No.125),”

requires the inclusion of the receivables within the Trust and any debt

securities issued by the Trust, or a related trust, in our Consolidated

Statements of Financial Position. Notwithstanding this accounting

treatment, the receivables transferred to the Trust are not available

to general creditors of Target. Upon termination of the securitization

program and repayment of all debt securities issued from time to time

by the Trust, or a related trust, any remaining assets could be

distributed to Target in a liquidation of TRC.

11. Inventory

Substantially all of our inventory and the related cost of sales are

accounted for under the retail inventory accounting method using the

last-in, first-out (LIFO) method. Inventory is stated at the lower of LIFO

cost or market. The LIFO provision is calculated based on inventory

levels, markup rates and internally-measured retail price indices. We

have not recorded any material LIFO provision in 2005 or 2004.

We routinely enter into arrangements with certain vendors whereby

we do not purchase or pay for merchandise until that merchandise is

ultimately sold to a guest. Revenues under this program are included

in the sales line in the Consolidated Statements of Operations, but

the merchandise received under the program is not included in our

Consolidated Statements of Financial Position because of the

simultaneous timing of our purchase and sale of this inventory. Sales

made under these arrangements totaled $872 million, $357 million

and $142 million for 2005, 2004 and 2003, respectively.

In 2005, we adopted SFAS No.151, “Inventory Costs, an

amendment of ARB No. 43, Chapter 4,” which clarifies that abnormal

amounts of idle facilities expense, freight, handling costs and spoilage

are to be recognized as current period charges and provides guidance

on the allocation of overhead. This adoption did not have a material

impact on our net earnings, cash flows or financial position.

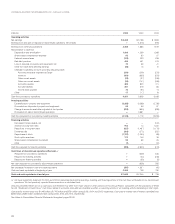

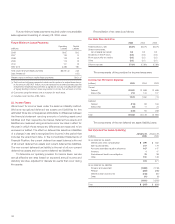

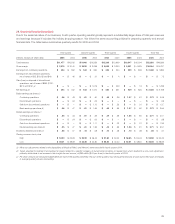

12. Other Current Assets

January 28, January 29,

(millions) 2006 2005

Vendor income and other receivables $ 560 $ 428

Deferred taxes 344 344

Other 349 452

Total $1,253 $1,224

In addition to vendor income, other receivables relate primarily to pharmacy

receivables and merchandise sourcing services provided to third parties.

13. Property and Equipment

Property and equipment are recorded at cost, less accumulated

depreciation. Depreciation is computed using the straight-line method

over estimated useful lives. Depreciation expense for the years 2005,

2004 and 2003 was $1,384 million, $1,232 million and $1,068 million,

respectively. Accelerated depreciation methods are generally used

for income tax purposes. Repair and maintenance costs were

$474 million, $453 million and $393 million in 2005, 2004 and 2003,

respectively, and are expensed as incurred.

Estimated useful lives by major asset category are as follows:

Asset Life (in years)

Buildings and improvements 8 –39

Fixtures and equipment 4 –15

Computer hardware and software 4