Target 2005 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2005 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

|

|

33

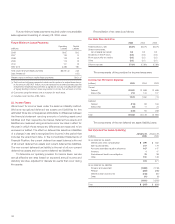

21. Interest Rate Swaps

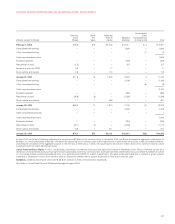

Our accounting policy for derivative financial instruments is discussed

in Note 1 on page 28.

At January 28, 2006 and January 29, 2005, interest rate swaps

were outstanding in notional amounts totaling $3,300 million and

$2,850 million, respectively. The increase in swap exposure was

executed to convert more of our fixed-rate debt to floating-rate debt

to minimize the effect on our earnings of changes in interest rates,

given that the majority of interest rates on our credit card receivables

re-price based on the changes in the prime rate.

During 2005, we entered into four interest rate swaps with

notional amounts of $250 million, $350 million, $325 million and

$225 million. We also terminated an interest rate swap with a notional

amount of $200 million, resulting in a gain of $24 million that will be

amortized into net interest expense over the remaining 13-year life of

the hedged debt. During 2004, we entered into two interest rate

swaps with notional amounts of $200 million and two interest rate

swaps with notional amounts of $250 million. We also terminated an

interest rate swap with a notional amount of $200 million, resulting in

a loss of $16 million that will be amortized into net interest expense

over the remaining 14-year life of the hedged debt. In 2005 and 2004,

the gains and losses amortized into net interest expense for

terminated swaps were not material to our results of operations.

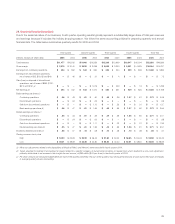

Interest Rate Swaps

(dollars in millions)

Notional Amount

Outstanding at Pay Floating Rate at (a)

Jan. 28, Jan. 29, Receive Jan. 28, Jan. 29,

Maturity 2006 2005 Fixed 2006 2005

Feb. 2005 $— $ 500 7.5% —% 2.4%

May 2006 550 550 4.6 4.8 3.3

Mar. 2008 250 —3.9 4.4 —

Mar. 2008 250 250 3.8 4.4 2.4

Oct. 2008 500 500 4.4 4.8 3.2

Oct. 2008 250 250 3.8 4.4 2.5

Nov. 2008 200 200 3.9 4.4 2.4

Jun. 2009 400 400 4.4 4.8 3.3

Jun. 2009 350 —4.2 4.5 —

Aug. 2010 325 —4.8 4.5 —

Aug. 2010 225 —4.5 4.5 —

May 2018 —200 5.8 — 3.3

$3,300 $2,850

(a) Reflects floating interest rate as of the respective year-end.

The weighted average life of the interest rate swaps was approximately 2.7 years

at January 28, 2006.

The fair value of outstanding interest rate swaps and unamortized

gains/(losses) from terminated interest rate swaps was $(21) million

at January 28, 2006 and $45 million at January 29, 2005. There was

no ineffectiveness recognized in 2005, 2004 or 2003 related to these

instruments.

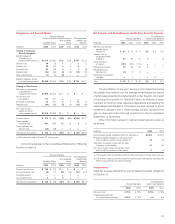

22. Leases

We lease certain retail locations, warehouses, distribution centers,

office space, equipment and land. Assets held under capital leases

are included in property and equipment and lease payments are

charged to depreciation and net interest expense over the life of the

lease. Operating lease rentals are expensed on a straight-line basis

over the life of the lease. Rent expense is recognized beginning with

the earlier of the date when we become legally obligated for the rent

payments or the date when we take possession of the property. At

the inception of a lease, we determine the lease term by assuming

the exercise of those renewal options that are reasonably assured

because of the significant economic penalty that exists for not

exercising those options. The exercise of lease renewal options is at

our sole discretion. The expected lease term is used to determine

whether a lease is capital or operating and is used to calculate straight-

line rent expense. Additionally, the useful life of buildings and leasehold

improvements are limited by the expected lease term. Our amortization

of leasehold improvements is consistent with the guidance issued by

the EITF in 2005 in Issue No. 05-6, “Determining the Amortization

Period for Leasehold Improvements Purchased after Lease Inception

or Acquired in a Business Combination,” which requires that leasehold

improvements purchased after the beginning of the initial lease term

be amortized over the shorter of the assets’ useful lives or a term that

includes the original lease term plus any renewals that are reasonably

assured at the date the leasehold improvements are purchased.

Therefore, our adoption of this guidance did not have an impact in

our net earnings, cash flows or financial position.

Rent expense on buildings, which is included in selling, general

and administrative expenses, includes percentage rents based on a

percentage of retail sales over contractual levels. Total rent expense

was $154 million in 2005, $240 million in 2004 and $150 million in

2003. Refer to Note 29, page 39 for discussion of the 2004 lease

accounting adjustment. Certain leases require us to pay real estate

taxes, insurance, maintenance and other operating expenses

associated with the leased premises. These amounts are not included

in rent expense but are classified in selling, general and administrative

expenses consistent with similar costs for owned locations. Most long-

term leases include options to renew, with terms varying from one to

50 years. Certain leases also include options to purchase the property.