Walmart 2008 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2008 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

WAL-MART 2008 ANNUAL REPORT 13

numerous dierent formats of retail stores and restaurants, including

discount stores, supercenters and Sam’s Clubs that operate outside

the United States.

For certain nancial information relating to our segments, see Note 11

to our Consolidated Financial Statements.

The Retail Industry

We operate in the highly competitive retail industry in both the

United States and the countries we serve internationally. We face

strong sales competition from other discount, department, drug,

variety and specialty stores, warehouse clubs, and supermarkets,

many of which are national, regional or international chains, as well

as internet-based retailers and catalog businesses. We compete with

a number of companies for prime retail site locations, as well as in

attracting and retaining quality employees (who we call “associates”).

We, along with other retail companies, are inuenced by a number of

factors including, but not limited to: cost of goods, consumer debt

levels and buying patterns, economic conditions, consumer credit

availability, interest rates, customer preferences, unemployment,

labor costs, ination, currency exchange uctuations, fuel and energy

prices, weather patterns, catastrophic events, competitive pressures

and insurance costs. Further information on risks to our Company

can be located in “Item 1A. Risk Factors” in our Annual Report on

Form 10-K for the year ended January 31, 2008.

Company Performance Metrics

Management uses a number of metrics to assess the Company’s

performance including:

• Total sales and comparable store sales;

• Operating income;

• Earnings per share;

• Return on investment; and

• Free cash ow.

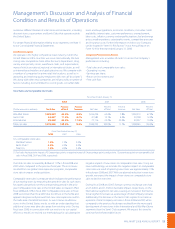

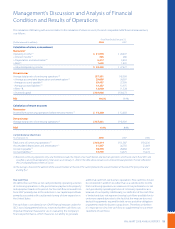

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

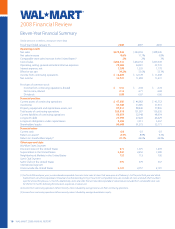

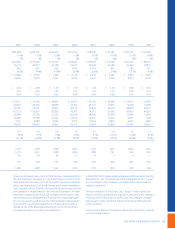

Total Sales and Comparable Store Sales

Fiscal Year Ended January 31,

2008 2007 2006

Percent Percent Percent Percent Percent

(Dollar amounts in millions) Net Sales of Total Increase Net Sales of Total Increase Net Sales of Total

Wal-Mart Stores $239,529 64.0% 5.8% $226,294 65.6% 7.8% $209,910 67.9%

Sam’s Club 44,357 11.8% 6.7% 41,582 12.1% 4.5% 39,798 12.9%

International 90,640 24.2% 17.5% 77,116 22.3% 30.2% 59,237 19.2%

Total net sales $374,526 100.0% 8.6% $344,992 100.0% 11.7% $308,945 100.0%

Fiscal Year Ended January 31,

2008 2007 2006

U.S. comparable store sales

Wal-Mart Stores 1.0% 1.9% 3.0%

Sam’s Club (1) 4.9% 2.5% 5.0%

Total U.S. 1.6% 2.0% 3.4%

(1) Fuel sales had a positive impact of 0.7 percentage points, a negative impact of 0.4 percentage points, and positive 1.3 percentage points on comparable club

sales in scal 2008, 2007 and 2006, respectively.

Our total net sales increased by 8.6% and 11.7% in scal 2008 and

2007 when compared to the previous scal year. Those increases

resulted from our global store expansion programs, comparable

store sales increases and acquisitions.

Comparable store sales is a measure which indicates the performance

of our existing stores by measuring the growth in sales for such stores

for a particular period over the corresponding period in the prior

year. Comparable store sales in the United States increased 1.6% in

scal 2008 and 2.0% in scal 2007. Comparable store sales in scal

2008 were lower than scal 2007 due to softness in the home and

apparel categories and pressure from new store expansions within

the trade area of established stores. As we continue to add new

stores in the United States, we do so with an understanding that

additional stores may take sales away from existing units. During

scal year 2008, in connection with our revisions to our capital

eciency model, we revised our methodology for calculating the

negative impact of new stores on comparable store sales. Using our

new methodology, we estimate the negative impact on comparable

store sales as a result of opening new stores was approximately 1.5%

in scal years 2008 and 2007. With our planned reduction in new store

growth, we expect the impact of new stores on comparable store

sales to decline over time.

During scal 2008 and 2007, foreign currency exchange rates had

a $4.5 billion and $1.5 billion favorable impact, respectively, on the

International segment’s net sales, causing an increase in the Interna-

tional segment’s net sales as a percentage of total Company net sales.

Additionally, the decrease in the Sam’s Club segment’s net sales as

a percent of total Company net sales in scal 2008 and 2007, when

compared to the previous scal years resulted from the more rapid

development of new stores in the International and Wal-Mart Stores

segments than the Sam’s Club segment. We expect this trend to

continue for the foreseeable future.