Walmart 2008 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2008 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

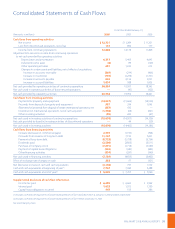

22 WAL-MART 2008 ANNUAL REPORT

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

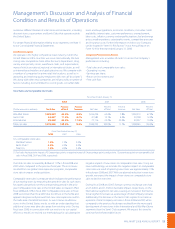

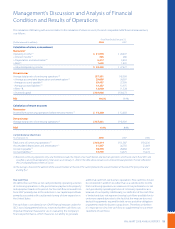

Capital Resources

During scal 2008, we issued $11.2 billion of long-term debt. The net

proceeds from the issuance of such long-term debt were used to

repay outstanding commercial paper indebtedness and for other

general corporate purposes.

Management believes that cash ows from operations and proceeds

from the sale of commercial paper will be sucient to nance seasonal

buildups in merchandise inventories and meet other cash requirements.

If our operating cash ows are not sucient to pay dividends and to

fund our capital expenditures, we anticipate funding any shortfall in

these expenditures with a combination of commercial paper and

long-term debt. We plan to renance existing long-term debt as it

matures and may desire to obtain additional long-term nancing for

other corporate purposes. We anticipate no diculty in obtaining

long-term nancing in view of our credit rating and favorable experi-

ences in the debt market in the recent past. The following table details

the ratings of the credit rating agencies that rated our outstanding

indebtedness at January 31, 2008. The rating agency ratings are not

recommendations to buy, sell or hold our commercial paper or debt

securities. Each rating may be subject to revision or withdrawal at

any time by the assigning rating organization and should be evalu-

ated independently of any other rating.

Rating Agency Commercial Paper Long-Term Debt

Standard & Poor’s A-1+ AA

Moody’s Investors Service P-1 Aa2

Fitch Ratings F1+ AA

DBRS Limited R-1(middle) AA

To monitor our credit rating and our capacity for long-term nancing,

we consider various qualitative and quantitative factors. We monitor

the ratio of our debt to our total capitalization as support for our

long-term nancing decisions. At January 31, 2008 and January 31,

2007, the ratio of our debt to total capitalization was approximately

40.9% and 38.8%, respectively. For the purpose of this calculation,

debt is dened as the sum of commercial paper, long-term debt

due within one year, obligations under capital leases due in one year,

long-term debt and long-term obligations under capital leases. Total

capitalization is dened as debt plus shareholders’ equity. Our ratio

of debt to our total capitalization has increased in scal 2008 due

to increased borrowing to fund our increased share repurchases as

well as other business needs.

We also use the ratio of adjusted cash flow from operations to

adjusted average debt as another metric to review leverage.

Adjusted cash ow from operations as the numerator is dened as

cash ow from operations of continuing operations for the current

year plus two–thirds of the current year operating rent expense less

current year capitalized interest expense. Adjusted average debt as

the denominator is dened as average debt plus eight times average

operating rent expense. Average debt is the simple average of begin-

ning and ending commercial paper, long-term debt due within one

year, obligations under capital leases due in one year, long-term debt

and long-term obligations under capital leases. Average operating

rent expense is the simple average of current year and prior year

operating rent expense. We believe this metric is useful to investors

as it provides them with a tool to measure our leverage. This metric

was 39% for our scal year 2008 and lower than 43% for our scal

year 2007. The decrease in the metric is primarily due to higher bor-

rowing levels as previously discussed.

The ratio of adjusted cash ow to adjusted average debt is considered

a non-GAAP nancial measure under the SEC’s rules. The most recog-

nized directly comparable GAAP measure is the ratio of cash ow from

operations of continuing operations for the current year to average

total debt (which excludes any eect of operating leases or capital-

ized interest), which was 49% for scal year 2008 and 51% for scal

year 2007.

A detailed calculation of the adjusted cash ow from operations to

adjusted average debt is set forth below along with a reconciliation

to the corresponding measurement calculated in accordance with

generally accepted accounting principles.