Walmart 2008 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2008 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

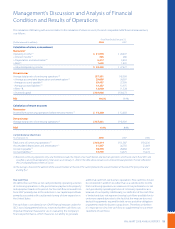

24 WAL-MART 2008 ANNUAL REPORT

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

Market Risk

In addition to the risks inherent in our operations, we are exposed to

certain market risks, including changes in interest rates and changes

in foreign currency exchange rates.

The analysis presented for each of our market risk sensitive instruments

is based on a 10% change in interest or foreign currency exchange

rates. These changes are hypothetical scenarios used to calibrate

potential risk and do not represent our view of future market changes.

As the hypothetical gures discussed below indicate, changes in fair

value based on the assumed change in rates generally cannot be

extrapolated because the relationship of the change in assumption

to the change in fair value may not be linear. The eect of a variation

in a particular assumption is calculated without changing any other

assumption. In reality, changes in one factor may result in changes

in another, which may magnify or counteract the sensitivities.

At January 31, 2008 and 2007, we had $35.7 billion and $32.7 billion,

respectively, of long-term debt outstanding. Our weighted average

eective interest rate on long-term debt, after considering the eect

of interest rate swaps, was 4.8% and 4.9% at January 31, 2008 and 2007,

respectively. A hypothetical 10% increase in interest rates in eect

at January 31, 2008 and 2007, would have increased annual interest

expense on borrowings outstanding at those dates by $25 million

and $47 million, respectively.

At January 31, 2008 and 2007, we had $5.0 billion and $2.6 billion of

outstanding commercial paper obligations. The weighted average

interest rate, including fees, on these obligations at January 31, 2008

and 2007, was 4.0% and 5.3%, respectively. A hypothetical 10% increase

in commercial paper rates in effect at January 31, 2008 and 2007,

would have increased annual interest expense on the outstanding

balances on those dates by $20 million and $14 million, respectively.

We enter into interest rate swaps to minimize the risks and costs

associated with nancing activities, as well as to maintain an appro-

priate mix of xed- and oating-rate debt. Our preference is to main-

tain between 40% and 50% of our debt portfolio, including interest

rate swaps, in oating-rate debt. The swap agreements are contracts

to exchange xed- or variable-rates for variable- or xed-interest rate

payments periodically over the life of the instruments. The aggre-

gate fair value of these swaps represented a gain of $265 million at

January 31, 2008 and a loss of $1 million at January 31, 2007. A hypo-

thetical increase (or decrease) of 10% in interest rates from the level

in eect at January 31, 2008, would have resulted in a (loss) or gain

in value of the swaps of ($45 million) or $46 million, respectively.

A hypothetical increase (or decrease) of 10% in interest rates from the

level in eect at January 31, 2007, would have resulted in a (loss) or

gain in value of the swaps of ($95 million) or $103 million, respectively.

We hold currency swaps to hedge the foreign currency exchange

component of our net investments in the United Kingdom. The

aggregate fair value of these swaps at January 31, 2008 and 2007,

represented a loss of $75 million and $181 million, respectively.

A hypothetical 10% increase (or decrease) in the foreign currency

exchange rates underlying these swaps from the market rate would

have resulted in a (loss) or gain in the value of the swaps of ($182 mil-

lion) and $182 million, respectively, at January 31, 2008. A hypothetical

10% increase (or decrease) in the foreign currency exchange rates

underlying these swaps from the market rate would have resulted

in a (loss) or gain in the value of the swaps of ($178 million) and

$196 million, respectively, at January 31, 2007. A hypothetical 10%

change in interest rates underlying these swaps from the market

rates in eect at January 31, 2008 and 2007, would have an insigni-

cant impact on the value of the swaps.

The following represents an allocation of our capital expenditures:

Allocation of Capital Expenditures

Projections Actual

Capital Expenditures Fiscal Year 2009 Fiscal Year 2008 Fiscal Year 2007

New stores, including expansions & relocations 35.4% 48.1% 51.0%

Remodels 7.6% 5.7% 5.4%

Information systems, distribution and other 22.8% 15.8% 21.5%

Total United States 65.8% 69.6% 77.9%

International 34.2% 30.4% 22.1%

Total capital expenditures 100.0% 100.0% 100.0%