Walmart 2008 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2008 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

|

|

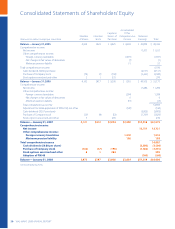

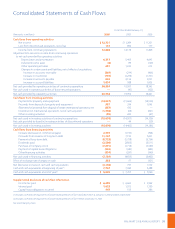

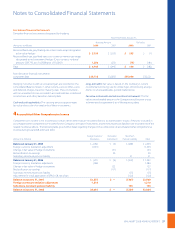

Notes to Consolidated Financial Statements

WAL-MART 2008 ANNUAL REPORT 39

years through 2015. In addition, the Company had other deferred

tax assets of $0.5 billion at January 31, 2008 and 2007, for which any

benet would be accounted for as an adjustment to goodwill. See

Note 13, “Recent Accounting Pronouncements,” for the impact of

Statement of Financial Accounting Standards No. 141(R), “Business

Combinations” with regard to accounting for tax benets acquired

in a business combination.

During scal 2007, the Company recorded a pretax loss of $918 million

on the disposition of its German operations. In addition, the Com-

pany recognized a tax benet of $126 million related to this transac-

tion. The Company recorded an additional loss on this disposition

of $153 million during scal year 2008. See Note 6, “Acquisitions and

Disposals,” for additional information about this transaction. The

Company plans to deduct the tax loss realized on the disposition

of its German operations as an ordinary worthless stock deduction.

Final resolution of the amount and character of the deduction may

result in the recognition of additional tax benets of up to $1.7 billion

which may be included in discontinued operations in future periods.

The Internal Revenue Service often challenges the characterization

of such deductions. If the loss is characterized as a capital loss, any

such capital loss could only be realized by being oset against future

capital gains and would expire in 2012. Any deferred tax asset, net of

its related valuation allowance, resulting from the characterization of

the loss as capital may be included with the Company’s non-current

assets of discontinued operations.

The Company adopted the provisions of FIN 48 eective February 1,

2007. FIN 48 claries the accounting for income taxes by prescribing

a minimum recognition threshold a tax position is required to meet

before being recognized in the nancial statements. FIN 48 also

provides guidance on derecognition, measurement, classication,

interest and penalties, accounting in interim periods, disclosure and

transition. As a result of the implementation of FIN 48, the Company

recognized a $236 million increase in the liability for unrecognized

tax benets relating to continuing operations and a $28 million

increase in the related liability for interest and penalties for a total

of $264 million. Of this amount, $160 million was accounted for as

a reduction to the February 1, 2007, balance of retained earnings,

$70 million as an increase to non-current deferred tax assets, and

$34 million as an increase to current deferred tax assets.

The Company classies interest on uncertain tax benets as interest

expense and income tax penalties as operating, selling, general and

administrative expenses. At February 1, 2007, before any tax benets,

the Company had $177 million of accrued interest and penalties on

unrecognized tax benets.

In the normal course of business, the Company provides for uncertain

tax positions and the related interest and adjusts its unrecognized

tax benets and accrued interest accordingly. For the full year scal

2008, unrecognized tax benets related to continuing operations and

accrued interest increased by $89 million and $65 million, respectively.

During the next twelve months, it is reasonably possible that tax

audit resolutions could reduce unrecognized tax benets by $50 mil-

lion to $200 million, either because the tax positions are sustained

on audit or because the Company agrees to their disallowance. Such

unrecognized taxed benets relate primarily to timing recognition

issues and the resolution of the gain determination on a discontinued

operation in scal year 2004.

A reconciliation of the beginning and ending balance of unrecognized

tax benefits related to continuing operations is as follows (dollars

in millions):

Balance at February 1, 2007 $779

Increases related to prior year tax positions 125

Decreases related to prior year tax positions (82)

Increases related to current year tax positions 106

Settlements during the period (50)

Lapse of statute of limitations (10)

Balance at January 31, 2008 $868

The amount, if recognized, which is included in the balance at

January 31, 2008, that would aect the Company’s eective tax rate

is $597 million. The dierence represents the amount of unrecognized

tax benets for which the ultimate tax consequence is certain, but

for which there is uncertainty about the timing of the tax conse-

quence recognition. Because of the impact of deferred tax account-

ing the timing would not impact the annual eective tax rate but

could accelerate the payment of cash to the taxing authority to an

earlier period.

Additionally, as of February 1, 2007, the Company had unrecognized

tax benets of $1.7 billion which if recognized would be recorded as

discontinued operations. Of this, $1.67 billion is related to a worthless

stock deduction to be claimed for the Company’s disposition of its

German operations in the second quarter of scal 2007, as mentioned

above. This increased by $57 million in the second quarter of scal

2008 as a result of the nal resolution of outstanding purchase price

adjustment claims and certain indemnities in conjunction with the

disposition of the Company’s German operations. The Company

cannot predict with reasonable certainty if this matter will be

resolved within the next twelve months.

The Company is subject to income tax examinations for its U.S. federal

income taxes generally for the scal years 2007 and 2008, with scal

years 2004 through 2006 remaining open for a limited number of

issues, for non-U.S. income taxes for the tax years 2002 through 2008,

and for state and local income taxes for the scal years generally 2004

through 2007 and from 1997 for a limited number of issues.

Additionally, the Company is subject to tax examinations for payroll,

value added, sales-based and other taxes. A number of these exami-

nations are ongoing and, in certain cases, have resulted in assessments

from the taxing authorities. Where appropriate, the Company has

made accruals for these matters which are reected in the Company’s

Consolidated Financial Statements. While these matters are individu-

ally immaterial, a group of related matters, if decided adversely to the

Company, may result in liability material to the Company’s nancial

condition or results of operations.