Walmart 2008 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2008 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56

|

|

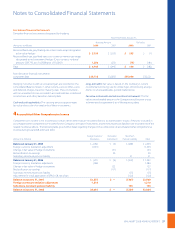

Notes to Consolidated Financial Statements

WAL-MART 2008 ANNUAL REPORT 47

13 Recent Accounting Pronouncements

In September 2006, the FASB issued Statement of Financial Accounting

Standards No. 157, “Fair Value Measurements” (“SFAS 157”). This standard

denes fair value, establishes a framework for measuring fair value

in generally accepted accounting principles and expands required

disclosures about fair value measurements. In November 2007, the

FASB provided a one year deferral for the implementation of SFAS 157

for nonnancial assets and liabilities. The Company will adopt SFAS

157 on February 1, 2008, as required. The adoption of SFAS 157 is not

expected to have a material impact on the Company’s nancial con-

dition and results of operations. However, the Company believes it will

likely be required to provide additional disclosures as part of future

nancial statements, beginning with the rst quarter of scal 2009.

In September 2006, the FASB also issued Statement of Financial

Accounting Standards No. 158, “Employers’ Accounting for Dened

Benet Pension and Other Postretirement Plans – an amendment of

FASB Statements No. 87, 88, 106 and 132(R)” (“SFAS 158”). This standard

requires recognition of the funded status of a benet plan in the state-

ment of nancial position. The Standard also requires recognition in

other comprehensive income of certain gains and losses that arise

during the period but are deferred under pension accounting rules, as

well as modies the timing of reporting and adds certain disclosures.

The Company adopted the funded status recognition and disclosure

elements as of January 31, 2007, and will adopt measurement ele-

ments as of January 31, 2009, as required by SFAS 158. The adoption

of SFAS 158 did not have a material impact on the Company’s nan-

cial condition, results of operations or liquidity.

In February 2007, the FASB issued Statement of Financial Accounting

Standards No. 159, “The Fair Value Option for Financial Assets and

Financial Liabilities — Including an amendment of FASB Statement

No. 115” (“SFAS 159”). SFAS 159 permits companies to measure many

nancial instruments and certain other items at fair value at specied

election dates. SFAS 159 will be eective beginning February 1, 2008.

The adoption of SFAS 159 is not expected to have a material impact

on the Company’s nancial condition and results of operations.

In December 2007, the FASB issued Statement of Financial Accounting

Standards No. 141(R), “Business Combinations” (“SFAS 141(R)”).

SFAS 141(R) replaces SFAS 141, “Business Combinations,” but retains

the requirement that the purchase method of accounting for

acquisitions be used for all business combinations. SFAS 141(R) better

denes the acquirer and the acquisition date in a business combination,

establishes principles for recognizing and measuring the assets acquired

(including goodwill), the liabilities assumed and any noncontrolling

interests in the acquired business and requires expanded disclosures

than previously required by SFAS 141. SFAS 141(R) also requires that,

from the date of adoption of SFAS 141(R), any change in valuation

allowance or uncertain tax position related to an acquired business,

irrespective of the acquisition date, shall be recorded as an adjustment

to income tax expense and not as an adjustment to goodwill as had

previously been required under SFAS 141. SFAS 141(R) will be eective for

all business combinations with an acquisition date on or after February 1,

2009, and early adoption is not permitted. The Company is currently

evaluating the impact SFAS No. 141(R) will have on the Company’s

Consolidated Financial Statements.

In December 2007, the FASB issued Statement of Financial Accounting

Standards No. 160, “Noncontrolling Interests in Consolidated Financial

Statements – an amendment of ARB No. 51” (“SFAS 160”). SFAS 160

requires that noncontrolling (or minority) interests in subsidiaries be

reported in the equity section of the company’s balance sheet, rather

than in the balance sheet between liabilities and equity. SFAS 160

also changes the manner in which the net income of the subsidiary

is reported and disclosed in the controlling company’s income

statement and establishes guidelines for accounting for changes

in ownership percentages and for deconsolidation. SFAS 160 will

be eective beginning February 1, 2009. The adoption of SFAS 160 is

not expected to have a material impact on the Company’s nancial

condition and results of operations.

14 Subsequent Events

On March 6, 2008, the Company’s Board of Directors approved an

increase in annual dividends to $0.95 per share. The annual dividend

will be paid in four quarterly installments on April 7, 2008, June 2,

2008, September 2, 2008, and January 2, 2009, to holders of record

on March 14, May 16, August 15 and December 15, 2008, respectively.

In March 2008, the Company announced it was exploring strategic

options for its property development subsidiary, Gazeley Limited,

which could conclude in a sale of that business. Gazeley Limited

develops industrial distribution warehouses in the United Kingdom,

mainland Europe and China and has extended its operations to

India and Mexico.