American Express 2012 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2012 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

AMERICAN EXPRESS COMPANY

2012 FINANCIAL REVIEW

ASSET SECURITIZATION PROGRAMS

The Company periodically securitizes cardmember receivables

and loans arising from its card business, as the securitization

market provides the Company with cost-effective funding.

Securitization of cardmember receivables and loans is

accomplished through the transfer of those assets to a trust,

which in turn issues to third-party investors certificates or notes

(securities) collateralized by the transferred assets. The proceeds

from issuance are distributed to the Company, through its

wholly owned subsidiaries, as consideration for the transferred

assets.

The receivables and loans being securitized are reported as

assets on the Company’s Consolidated Balance Sheets and the

related securities issued to third-party investors are reported as

long-term debt.

Under the respective terms of the securitization trust

agreements, the occurrence of certain triggering events

associated with the performance of the assets of each trust could

result in payment of trust expenses, establishment of reserve

funds, or in a worst-case scenario, early amortization of investor

certificates. During the year ended December 31, 2012, no such

triggering events occurred.

The ability of issuers of asset-backed securities relating to

cardmember receivables and loans of an originating bank to

obtain necessary credit ratings for their issuances has historically

been based, in part, on qualification under the FDIC’s safe

harbor rule for assets transferred in securitizations. In 2009 and

2010, the FDIC issued a series of changes to its safe harbor rule,

including a final rule for securitization safe harbor, issued in

2010, requiring issuers to comply with a new set of requirements

in order to qualify for the safe harbor protection. Issuances out of

the Lending Trust are grandfathered under the new FDIC final

rule. There are two trusts for the Company’s cardmember charge

card receivable securitization, the American Express Issuance

Trust (the Charge Trust) and the American Express Issuance

Trust II (the Charge Trust II). The Charge Trust does not satisfy

the criteria required to be covered by the FDIC’s new safe harbor

rule, nor did it meet the requirements to be covered by the safe

harbor rule existing prior to 2009. It was structured, and

continues to be structured, so that the financial assets transferred

to the Charge Trust would not be deemed to be property of the

originating banks in the event the FDIC is appointed as a receiver

or conservator of the originating banks. The Charge Trust II,

which was formed in October 2012, was designed to satisfy the

criteria to be covered by the FDIC’s new safe harbor rule.

LIQUIDITY MANAGEMENT

The Company’s liquidity objective is to maintain access to a

diverse set of cash, readily marketable securities and contingent

sources of liquidity, so that the Company can continuously meet

expected future financing obligations and business requirements

for at least a 12-month period, even in the event it is unable to

raise new funds under its regular funding programs. The

Company has in place a Liquidity Risk Policy that sets out the

Company’s approach to managing liquidity risk on an

enterprise-wide basis.

The Company incurs and accepts liquidity risk arising in the

normal course of offering its products and services. The liquidity

risks that the Company is exposed to can arise from a variety of

sources, and thus its liquidity management strategy includes a

variety of parameters, assessments and guidelines, including, but

not limited to:

폷Maintaining a diversified set of funding sources (refer to

Funding Strategy section for more details);

폷Maintaining unencumbered liquid assets and off-balance sheet

liquidity sources; and

폷Projecting cash inflows and outflows from a variety of sources

and under a variety of scenarios, including contingent liquidity

exposures such as unused cardmember lines of credit and

collateral requirements for derivative transactions.

The Company’s current liquidity target is to have adequate

liquidity in the form of excess cash and readily marketable

securities that are easily convertible into cash to satisfy all

maturing long-term funding obligations for a 12-month period.

In addition to its cash and readily marketable securities, the

Company maintains a variety of contingent liquidity resources,

such as access to undrawn amounts under its secured financing

facilities and the Federal Reserve discount window as well as

committed bank credit facilities.

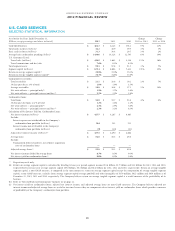

As of December 31, 2012, the Company’s excess cash available to

fund long-term maturities was as follows:

(Billions) Total

Cash $ 15.8(a)

Securities held as collateral 0.3(b)

Cash available to fund maturities $ 16.1

(a) Includes $22.3 billion classified as cash and cash equivalents, less $6.5 billion

of cash available to fund day-to-day operations. The $15.8 billion represents

cash residing in the United States.

(b) Off-balance sheet securities held as collateral from a counterparty that had

not been sold or repledged.

The upcoming approximate maturities of the Company’s long-

term unsecured debt, debt issued in connection with asset-

backed securitizations and long-term certificates of deposit are as

follows:

(Billions) Debt Maturities

2013 Quarters Ending:

Unsecured

Debt

Asset-Backed

Securitizations

Certificates

of Deposit Total

March 31 $ — $ — $ 0.8 $ 0.8

June 30 4.5 0.9 0.9 6.3

September 30 3.1 2.0 0.6 5.7

December 31 — 1.2 2.6 3.8

Total $ 7.6 $ 4.1 $ 4.9 $ 16.6

The Company’s financing needs for the next 12 months are

expected to arise from these debt and deposit maturities as well

as changes in business needs, including changes in outstanding

cardmember loans and receivables and acquisition activities.

34