Charter 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

CHARTER COMMUNICATIONS, INC. 2006 FORM 10-K

(Verifying the integrity of the customer’s network connec- method over management’s estimate of the estimated useful

tion by initiating test signals downstream from the headend lives of the related assets as listed below:

to the customer’s digital set-top box.

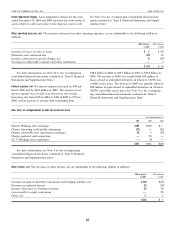

Cable distribution systems 7-20 years

Judgment is required to determine the extent to which Customer equipment and installations 3-5 years

overhead costs incurred result from specific capital activities, and Vehicles and equipment 1-5 years

Buildings and leasehold improvements 5-15 years

therefore should be capitalized. The primary costs that are Furniture, fixtures and equipment 5 years

included in the determination of the overhead rate are

(i) employee benefits and payroll taxes associated with capital- Impairment of property, plant and equipment, franchises and goodwill.

ized direct labor, (ii) direct variable costs associated with As discussed above, the net carrying value of our property, plant

capitalizable activities, consisting primarily of installation and and equipment is significant. We also have recorded a significant

construction vehicle costs, (iii) the cost of support personnel, amount of cost related to franchises, pursuant to which we are

such as dispatchers, who directly assist with capitalizable granted the right to operate our cable distribution network

installation activities, and (iv) indirect costs directly attributable throughout our service areas. The net carrying value of

to capitalizable activities. franchises as of December 31, 2006 and 2005 was approximately

While we believe our existing capitalization policies are $9.2 billion (representing 61% of total assets) and $9.8 billion

appropriate, a significant change in the nature or extent of our (representing 60% of total assets), respectively. Furthermore, our

system activities could affect management’s judgment about the noncurrent assets include approximately $61 million of goodwill.

extent to which we should capitalize direct labor or overhead in We adopted SFAS No. 142, Goodwill and Other Intangible

the future. We monitor the appropriateness of our capitalization Assets, on January 1, 2002. SFAS No. 142 requires that franchise

policies, and perform updates to our internal studies on an intangible assets that meet specified indefinite-life criteria no

ongoing basis to determine whether facts or circumstances longer be amortized against earnings, but instead must be tested

warrant a change to our capitalization policies. We capitalized for impairment annually based on valuations, or more frequently

internal direct labor and overhead of $204 million, $190 million as warranted by events or changes in circumstances. In

and $164 million, respectively, for the years ended December 31, determining whether our franchises have an indefinite-life, we

2006, 2005, and 2004. Capitalized internal direct labor and considered the likelihood of franchise renewals, the expected

overhead costs have increased in 2005 and 2006 as compared to costs of franchise renewals, and the technological state of the

2004 as a result of the use of more internal labor for associated cable systems, with a view to whether or not we are

capitalizable installations, rather than third party contractors. in compliance with any technology upgrading requirements

specified in a franchise agreement. We have concluded that as

Useful lives of property, plant and equipment. We evaluate the of December 31, 2006, 2005, and 2004 more than 99% of our

appropriateness of estimated useful lives assigned to our prop- franchises qualify for indefinite-life treatment under

erty, plant and equipment, based on annual analyses of such SFAS No. 142, and that less than one percent of our franchises

useful lives, and revise such lives to the extent warranted by do not qualify for indefinite-life treatment, due to technological

changing facts and circumstances. Any changes in estimated or operational factors that limit their lives. Costs of finite-lived

useful lives as a result of these analyses, which were not franchises, along with costs associated with franchise renewals,

significant in the periods presented, will be reflected prospec- are amortized on a straight-line basis over 10 years, which

tively beginning in the period in which the study is completed. represents management’s best estimate of the average remaining

The effect of a one-year decrease in the weighted average useful lives of such franchises. Franchise amortization expense

remaining useful life of our property, plant and equipment was $2 million, $4 million, and $3 million for the years ended

would be an increase in depreciation expense for the year ended December 31, 2006, 2005, and 2004, respectively. We expect

December 31, 2006 of approximately $168 million. The effect of that amortization expense on franchise assets will be approxi-

a one-year increase in the weighted average useful life of our mately $1 million annually for each of the next five years.

property, plant and equipment would be a decrease in deprecia- Actual amortization expense in future periods could differ from

tion expense for the year ended December 31, 2006 of these estimates as a result of new intangible asset acquisitions or

approximately $131 million. divestitures, changes in useful lives, and other relevant factors.

Depreciation expense related to property, plant and equip- Our goodwill is also deemed to have an indefinite life under

ment totaled $1.3 billion, $1.4 billion, and $1.4 billion, represent- SFAS No. 142.

ing approximately 26%, 30%, and 21% of costs and expenses, for SFAS No. 144, Accounting for Impairment or Disposal of Long-

the years ended December 31, 2006, 2005, and 2004, respec- Lived Assets, requires that we evaluate the recoverability of our

tively. Depreciation is recorded using the straight-line composite property, plant and equipment and franchise assets which did

not qualify for indefinite-life treatment under SFAS No. 142,

upon the occurrence of events or changes in circumstances

which indicate that the carrying amount of an asset may not be

recoverable. Such events or changes in circumstances could

include such factors as the impairment of our indefinite-life

33