Charter 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

CHARTER COMMUNICATIONS, INC. 2006 FORM 10-K

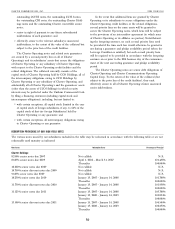

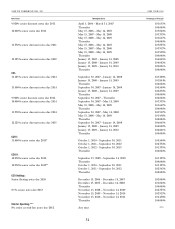

Note Series Redemption Dates Percentage of Principal

83

/8% senior second-lien notes due 2014 April 30, 2009 — April 29, 2010 104.188%

April 30, 2010 — April 29, 2011 102.792%

April 30, 2011 — April 29, 2012 101.396%

Thereafter 100.000%

* CCH I may, prior to October 1, 2008 in the event of a qualified equity offering providing sufficient proceeds, redeem up to 35% of the aggregate principal amount of

the CCH I notes at a redemption price of 111% of the principal amount plus accrued and unpaid interest.

** CCH II may, prior to October 1, 2009 in the event of a qualified equity offering providing sufficient proceeds, redeem up to 35% of the aggregate principal amount of

the CCH II notes at a redemption price of 110.25% of the principal amount plus accrued and unpaid interest.

*** Charter Operating may, prior to April 30, 2007 in the event of a qualified equity offering providing sufficient proceeds, redeem up to 35% of the aggregate principal

amount of the Charter Operating notes at a redemption price of 108.375% with respect to the 83

/8% senior second-lien notes due 2014 Notes and a redemption price of

108% with respect to the 8% senior second-lien notes due 2012.

**** Charter Operating may, at any time and from time to time, at their option, redeem the outstanding 8% second lien notes due 2012, in whole or in part, at a redemption

price equal to 100% of the principal amount thereof plus accrued and unpaid interest, if any, to the redemption date, plus the Make-Whole Premium. The Make-Whole

Premium is an amount equal to the excess of (a) the present value of the remaining interest and principal payments due on a 8% senior second-lien notes due 2012 to

its final maturity date, computed using a discount rate equal to the Treasury Rate on such date plus 0.50%, over (b) the outstanding principal amount of such Note.

In the event that a specified change of control event occurs, Restrictions on Additional Debt

each of the respective issuers of the notes must offer to The limitations on incurrence of debt and issuance of preferred

repurchase any then outstanding notes at 101% of their principal stock contained in various indentures permit each of the

amount or accrued value, as applicable, plus accrued and unpaid respective notes issuers and its restricted subsidiaries to incur

interest, if any. additional debt or issue preferred stock, so long as, after giving

pro forma effect to the incurrence, the leverage ratio would be

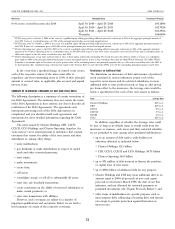

SUMMARY OF RESTRICTIVE COVENANTS OF OUR HIGH YIELD NOTES below a specified level for each of the note issuers as follows:

The following description is a summary of certain restrictions of Issuer Leverage Ratio

our Debt Agreements. The summary does not restate the terms

Charter Holdings 8.75 to 1

of the Debt Agreements in their entirety, nor does it describe all CIH 8.75 to 1

restrictions of the Debt Agreements. The agreements and CCH I 7.5 to 1

instruments governing each of the Debt Agreements are CCH II 5.5 to 1

complicated and you should consult such agreements and CCOH 4.5 to 1

instruments for more detailed information regarding the Debt CCO 4.25 to 1

Agreements. In addition, regardless of whether the leverage ratio could

The notes issued by Charter Holdings, CIH, CCH I, be met, so long as no default exists or would result from the

CCH II, CCO Holdings and Charter Operating (together, the incurrence or issuance, each issuer and their restricted subsidiar-

‘‘note issuers’’) were issued pursuant to indentures that contain ies are permitted to issue among other permitted indebtedness:

covenants that restrict the ability of the note issuers and their

(up to an amount of debt under credit facilities not

subsidiaries to, among other things: otherwise allocated as indicated below:

(incur indebtedness;

(Charter Holdings: $3.5 billion

(pay dividends or make distributions in respect of capital

(CIH, CCH I, CCH II and CCO Holdings: $9.75 billion

stock and other restricted payments;

(Charter Operating: $6.8 billion

(issue equity;

(up to $75 million of debt incurred to finance the purchase

(make investments; or capital lease of new assets;

(create liens;

(up to $300 million of additional debt for any purpose;

(sell assets;

(Charter Holdings and CIH may incur additional debt in an

(consolidate, merge, or sell all or substantially all assets; amount equal to 200% of proceeds of new cash equity

proceeds received since March 1999, the date of our first

(enter into sale leaseback transactions;

indenture, and not allocated for restricted payments or

(create restrictions on the ability of restricted subsidiaries to permitted investments (the ‘‘Equity Proceeds Basket’’); and

make certain payments; or

(other items of indebtedness for specific purposes such as

(enter into transactions with affiliates. intercompany debt, refinancing of existing debt, and interest

However, such covenants are subject to a number of rate swaps to provide protection against fluctuation in

important qualifications and exceptions. Below we set forth a interest rates.

brief summary of certain of the restrictive covenants.

52