Charter 2006 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2006 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

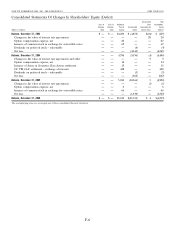

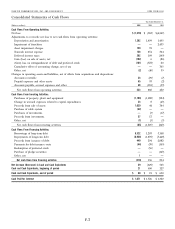

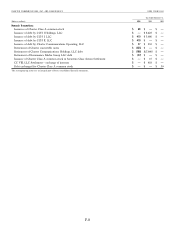

|

|

CHARTER COMMUNICATIONS, INC. AND SUBSIDIARIES 2006 FORM 10-K

Notes to Consolidated Financial Statements (continued)

6. PROPERTY, PLANT AND EQUIPMENT and market new services, such as interactivity and telephone, to

the potential customers (service marketing rights). Fair value is

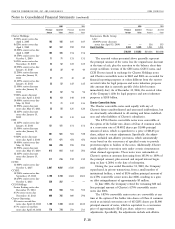

Property, plant and equipment consists of the following as of determined based on estimated discounted future cash flows

December 31, 2006 and 2005: using assumptions consistent with internal forecasts. The

franchise after-tax cash flow is calculated as the after-tax cash

2006 2005 flow generated by the potential customers obtained (less the

Cable distribution systems $ 7,035 $ 7,014 anticipated customer churn), and the new services added to

Customer equipment and installations 4,219 3,955 those customers in future periods. The sum of the present value

Vehicles and equipment 474 473 of the franchises’ after-tax cash flow in years 1 through 10 and

Buildings and leasehold improvements 526 584

Furniture, fixtures and equipment 607 563 the continuing value of the after-tax cash flow beyond year 10

12,861 12,589 yields the fair value of the franchise.

Less: accumulated depreciation (7,644) (6,749) The Company follows the guidance of Emerging Issues

$ 5,217 $ 5,840 Task Force (‘‘EITF’’) Issue 02-17, Recognition of Customer

Relationship Intangible Assets Acquired in a Business Combination, in

The Company periodically evaluates the estimated useful valuing customer relationships. Customer relationships, for valu-

lives used to depreciate its assets and the estimated amount of ation purposes, represent the value of the business relationship

assets that will be abandoned or have minimal use in the future. with existing customers (less the anticipated customer churn),

A significant change in assumptions about the extent or timing and are calculated by projecting future after-tax cash flows from

of future asset retirements, or in the Company’s use of new these customers, including the right to deploy and market

technology and upgrade programs, could materially affect future additional services such as interactivity and telephone to these

depreciation expense. customers. The present value of these after-tax cash flows yields

Depreciation expense for the years ended December 31, the fair value of the customer relationships. Substantially all

2006, 2005 and 2004 was $1.3 billion, $1.4 billion and acquisitions occurred prior to January 1, 2002. The Company

$1.4 billion, respectively. did not record any value associated with the customer relation-

ship intangibles related to those acquisitions. For acquisitions

7. FRANCHISES AND GOODWILL

subsequent to January 1, 2002 the Company did assign a value

Franchise rights represent the value attributed to agreements to the customer relationship intangible, which is amortized over

with local authorities that allow access to homes in cable service its estimated useful life.

areas acquired through the purchase of cable systems. Manage- In September 2004, the SEC staff issued EITF Topic D-108

ment estimates the fair value of franchise rights at the date of which requires the direct method of separately valuing all

acquisition and determines if the franchise has a finite life or an intangible assets and does not permit goodwill to be included in

indefinite-life as defined by SFAS No. 142, Goodwill and Other franchise assets. The Company adopted Topic D-108 in its

Intangible Assets. Franchises that qualify for indefinite-life treat- impairment assessment as of September 30, 2004. Such impair-

ment under SFAS No. 142 are tested for impairment annually ment assessment resulted in a total franchise impairment of

each October 1 based on valuations, or more frequently as approximately $3.3 billion. The Company recorded a cumulative

warranted by events or changes in circumstances. Such test effect of accounting change of $765 million (approximately

resulted in a total franchise impairment of approximately $875 million before tax effects of $91 million and minority

$3.3 billion during the third quarter of 2004. The 2005 and 2006 interest effects of $19 million) for the year ended December 31,

annual impairment tests resulted in no impairment. Franchises 2004 representing the portion of the Company’s total franchise

are aggregated into essentially inseparable asset groups to impairment attributable to no longer including goodwill with

conduct the valuations. The asset groups generally represent franchise assets. The effect of the adoption was to increase net

geographic clustering of the Company’s cable systems into loss and loss per share by $765 million and $2.55, respectively,

groups by which such systems are managed. Management for the year ended December 31, 2004. The remaining $2.4 bil-

believes such grouping represents the highest and best use of lion of the total franchise impairment was attributable to the use

those assets. of lower projected growth rates and the resulting revised

The Company’s valuations, which are based on the present estimates of future cash flows in the Company’s valuation, and

value of projected after tax cash flows, result in a value of was recorded as impairment of franchises in the Company’s

property, plant and equipment, franchises, customer relation- accompanying consolidated statements of operations for the

ships, and its total entity value. The value of goodwill is the year ended December 31, 2004. Sustained analog video cus-

difference between the total entity value and amounts assigned tomer losses by the Company in the third quarter of 2004

to the other assets. primarily as a result of increased competition from direct

Franchises, for valuation purposes, are defined as the future broadcast satellite providers and decreased growth rates in the

economic benefits of the right to solicit and service potential Company’s high-speed Internet customers in the third quarter of

customers (customer marketing rights), and the right to deploy 2004, in part, as a result of increased competition from digital

F-16