Charter 2006 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2006 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

CHARTER COMMUNICATIONS, INC. 2006 FORM 10-K

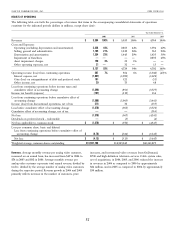

the third quarter of 2004 primarily as a result of increased Because the respective capital account balances of each of

competition from DBS providers and decreased growth rates in Vulcan Cable and CII were reduced to zero by December 31,

our and our industry peers’ high-speed Internet customers in the 2002, certain net tax losses of Charter Holdco that were to be

third quarter of 2004, in part as a result of increased competition allocated for 2002, 2003, 2004 and 2005, to Vulcan Cable and

from DSL providers, led us to lower our projected growth rates CII, instead have been allocated to Charter (the ‘‘Regulatory

and accordingly revise our estimates of future cash flows from Allocations’’). As a result of the allocation of net tax losses to

those used in prior years. See ‘‘Item 1. Business — Competition.’’ Charter in 2005, Charter’s capital account balance was reduced

The valuations completed at October 1, 2006 and 2005 to zero during 2005. The LLC Agreement provides that once

showed franchise values in excess of book value, and thus the capital account balances of all members have been reduced

resulted in no impairment. to zero, net tax losses are to be allocated to Charter, Vulcan

Cable and CII based generally on their respective percentage

Income Taxes. All operations are held through Charter Holdco ownership of outstanding common units. Such allocations are

and its direct and indirect subsidiaries. Charter Holdco and the also considered to be Regulatory Allocations. The LLC Agree-

majority of its subsidiaries are not subject to income tax. ment further provides that, to the extent possible, the effect of

However, certain of these subsidiaries are corporations and are the Regulatory Allocations is to be offset over time pursuant to

subject to income tax. All of the taxable income, gains, losses, certain curative allocation provisions (the ‘‘Curative Allocation

deductions and credits of Charter Holdco are passed through to Provisions’’) so that, after certain offsetting adjustments are

its members: Charter, CII and Vulcan Cable. Charter is made, each member’s capital account balance is equal to the

responsible for its share of taxable income or loss of Charter capital account balance such member would have had if the

Holdco allocated to it in accordance with the Charter Holdco Regulatory Allocations had not been part of the LLC Agree-

limited liability company agreement (‘‘LLC Agreement’’) and ment. The cumulative amount of the actual tax losses allocated

partnership tax rules and regulations. to Charter as a result of the Regulatory Allocations through the

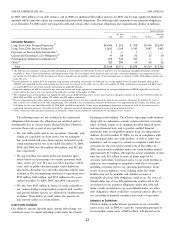

The LLC Agreement provides for certain special allocations year ended December 31, 2006 is approximately $4.1 billion.

of net tax profits and net tax losses (such net tax profits and net As a result of the Special Loss Allocations and the

tax losses being determined under the applicable federal income Regulatory Allocations referred to above (and their interaction

tax rules for determining capital accounts). Under the LLC with the allocations related to assets contributed to Charter

Agreement, through the end of 2003, net tax losses of Charter Holdco with differences between book and tax basis), the

Holdco that would otherwise have been allocated to Charter cumulative amount of losses of Charter Holdco allocated to

based generally on its percentage ownership of outstanding Vulcan Cable and CII is in excess of the amount that would

common units were allocated instead to membership units held have been allocated to such entities if the losses of Charter

by Vulcan Cable and CII (the ‘‘Special Loss Allocations’’) to the Holdco had been allocated among its members in proportion to

extent of their respective capital account balances. After 2003, their respective percentage ownership of Charter Holdco com-

under the LLC Agreement, net tax losses of Charter Holdco are mon membership units. The cumulative amount of such excess

allocated to Charter, Vulcan Cable and CII based generally on losses was approximately $1 billion through December 31, 2006.

their respective percentage ownership of outstanding common In certain situations, the Special Loss Allocations, Special

units to the extent of their respective capital account balances. Profit Allocations, Regulatory Allocations, and Curative Alloca-

Allocations of net tax losses in excess of the members’ aggregate tion Provisions described above could result in Charter paying

capital account balances are allocated under the rules governing taxes in an amount that is more or less than if Charter Holdco

Regulatory Allocations, as described below. Subject to the had allocated net tax profits and net tax losses among its

Curative Allocation Provisions described below, the LLC Agree- members based generally on the number of common member-

ment further provides that, beginning at the time Charter ship units owned by such members. This could occur due to

Holdco generates net tax profits, the net tax profits that would differences in (i) the character of the allocated income (e.g.,

otherwise have been allocated to Charter based generally on its ordinary versus capital), (ii) the allocated amount and timing of

percentage ownership of outstanding common membership tax depreciation and tax amortization expense due to the

units, will instead generally be allocated to Vulcan Cable and CII application of section 704(c) under the Internal Revenue Code,

(the ‘‘Special Profit Allocations’’). The Special Profit Allocations (iii) the potential interaction between the Special Profit Alloca-

to Vulcan Cable and CII will generally continue until the tions and the Curative Allocation Provisions, (iv) the amount

cumulative amount of the Special Profit Allocations offsets the and timing of alternative minimum taxes paid by Charter, if any,

cumulative amount of the Special Loss Allocations. The amount (v) the apportionment of the allocated income or loss among

and timing of the Special Profit Allocations are subject to the the states in which Charter Holdco does business, and

potential application of, and interaction with, the Curative (vi) future federal and state tax laws. Further, in the event of

Allocation Provisions described in the following paragraph. The new capital contributions to Charter Holdco, it is possible that

LLC Agreement generally provides that any additional net tax the tax effects of the Special Profit Allocations, Special Loss

profits are to be allocated among the members of Charter Allocations, Regulatory Allocations and Curative Allocation

Holdco based generally on their respective percentage owner- Provisions will change significantly pursuant to the provisions of

ship of Charter Holdco common membership units. the income tax regulations or the terms of a contribution

35