Coca Cola 2005 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2005 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

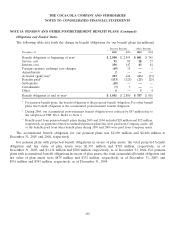

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 15: PENSION AND OTHER POSTRETIREMENT BENEFIT PLANS (Continued)

Asset allocation targets promote optimal expected return and volatility characteristics given the long-term

time horizon for fulfilling the obligations of the pension plans. Selection of the targeted asset allocation for U.S.

plan assets was based upon a review of the expected return and risk characteristics of each asset class, as well as

the correlation of returns among asset classes.

Investment guidelines are established with each investment manager. These guidelines provide the

parameters within which the investment managers agree to operate, including criteria that determine eligible

and ineligible securities, diversification requirements and credit quality standards, where applicable. Unless

exceptions have been approved, investment managers are prohibited from buying or selling commodities, futures

or option contracts, as well as from short selling of securities. Furthermore, investment managers agree to obtain

written approval for deviations from stated investment style or guidelines.

As of December 31, 2005, no investment manager was responsible for more than 10 percent of total U.S.

plan assets. In addition, diversification requirements for each investment manager prevent a single security or

other investment from exceeding 10 percent, at historical cost, of the total U.S. plan assets.

The expected long-term rate of return assumption for U.S. plan assets is based upon the target asset

allocation and is determined using forward-looking assumptions in the context of historical returns and

volatilities for each asset class, as well as correlations among asset classes. We evaluate the rate of return

assumption on an annual basis. The expected long-term rate of return assumption used in computing 2005 net

periodic pension cost for the U.S. plans was 8.5 percent. As of December 31, 2005, the 10-year annualized return

on U.S. plan assets was 9.6 percent, the 15-year annualized return was 11.6 percent, and the annualized return

since inception was 12.7 percent.

Plan assets for our pension plans outside the United States are insignificant on an individual plan basis.

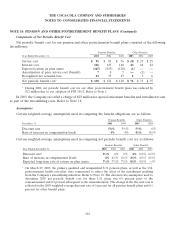

Cash Flows

Information about the expected cash flows for our pension and other postretirement benefit plans is as

follows (in millions):

Pension Other

Benefits Benefits

Expected employer contributions:

2006 $ 103 $ 9

Expected benefit payments1:

2006 $ 125 $ 30

2007 131 32

2008 134 34

2009 135 37

2010 140 39

2011-2015 782 233

1The expected benefit payments for our other postretirement benefit plans do not reflect any

estimated federal subsidies expected to be received under the Medicare Prescription Drug,

Improvement and Modernization Act of 2003. Federal subsidies are estimated to range from

$1.9 million in 2006 to $3.0 million in 2010 and are estimated to be $19.8 million for the period

2011-2015.

106