Coca Cola 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

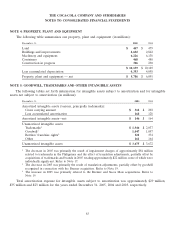

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1: BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Retirement-Related Benefits

Using appropriate actuarial methods and assumptions, our Company accounts for defined benefit pension

plans in accordance with SFAS No. 87, ‘‘Employers’ Accounting for Pensions.’’ We account for our nonpension

postretirement benefits in accordance with SFAS No. 106, ‘‘Employers’ Accounting for Postretirement Benefits

Other Than Pensions.’’ In 2003, we adopted SFAS No. 132 (revised 2003), ‘‘Employers’ Disclosures about

Pensions and Other Postretirement Benefits,’’ (‘‘SFAS No. 132(R)’’) for all U.S. plans. As permitted by this

standard, in 2004, we adopted the disclosure provisions for all foreign plans. SFAS No. 132(R) requires

additional disclosures about the assets, obligations, cash flows and net periodic benefit cost of defined benefit

pension plans and other defined benefit postretirement plans. This statement did not change the measurement

or recognition of those plans required by SFAS No. 87, SFAS No. 88, ‘‘Employers’ Accounting for Settlements

and Curtailments of Defined Benefit Pension Plans and for Termination Benefits,’’ or SFAS No. 106. Refer to

Note 15 for a description of how we determine our principal assumptions for pension and postretirement benefit

accounting.

Contingencies

Our Company is involved in various legal proceedings and tax matters. Due to their nature, such legal

proceedings and tax matters involve inherent uncertainties including, but not limited to, court rulings,

negotiations between affected parties and governmental actions. Management assesses the probability of loss for

such contingencies and accrues a liability and/or discloses the relevant circumstances, as appropriate. Refer to

Note 12.

Business Combinations

In accordance with SFAS No. 141, ‘‘Business Combinations,’’ we account for all business combinations by

the purchase method. Furthermore, we recognize intangible assets apart from goodwill if they arise from

contractual or legal rights or if they are separable from goodwill.

Recent Accounting Standards and Pronouncements

In May 2005, the FASB issued SFAS No. 154, ‘‘Accounting Changes and Error Corrections, a replacement

of Accounting Principles Board (‘‘APB’’) Opinion No. 20 and FASB Statement No. 3.’’ SFAS No. 154 requires

retrospective application to prior periods’ financial statements of a voluntary change in accounting principle

unless it is impracticable. APB Opinion No. 20, ‘‘Accounting Changes,’’ previously required that most voluntary

changes in accounting principle be recognized by including in net income of the period of the change the

cumulative effect of changing to the new accounting principle. SFAS No. 154 became effective for our Company

on January 1, 2006. We believe that the adoption of SFAS No. 154 will not have a material impact on our

consolidated financial statements.

In December 2004, the FASB issued SFAS No. 153, ‘‘Exchanges of Nonmonetary Assets, an amendment of

APB Opinion No. 29.’’ SFAS No. 153 is based on the principle that exchanges of nonmonetary assets should be

measured based on the fair value of the assets exchanged. APB Opinion No. 29, ‘‘Accounting for Nonmonetary

Transactions,’’ provided an exception to its basic measurement principle (fair value) for exchanges of similar

productive assets. Under APB Opinion No. 29, an exchange of a productive asset for a similar productive asset

was based on the recorded amount of the asset relinquished. SFAS No. 153 eliminates this exception and

replaces it with an exception for exchanges of nonmonetary assets that do not have commercial substance. SFAS

No. 153 became effective for our Company as of July 2, 2005, and did not have a material impact on our

74