LabCorp 2014 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2014 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

F-22

funds rate plus a margin ranging from 0.125% to 1.00%. Advances under the new revolving credit facility will accrue interest at

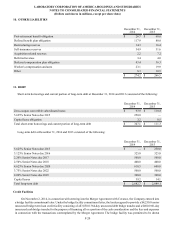

a per annum rate equal to, at the Company’s election, either a LIBOR rate plus a margin ranging from 1.00% to 1.60%, or a base

rate determined according to a prime rate or federal funds rate plus a margin ranging from 0.00% to 0.60%. Fees are payable on

outstanding letters of credit under the new revolving credit facility at a per annum rate equal to the applicable margin for LIBOR

loans, and the Company is required to pay a facility fee on the aggregate commitments under the new revolving credit facility, at

a per annum rate ranging from 0.125% to 0.40%. The 60-day cash bridge term loan credit facility will accrue interest at a per

annum rate equal to, at the Company’s election, either a LIBOR rate plus a margin ranging from 1.25% to 2.00%, or a base rate

determined according to a prime rate or federal funds rate plus a margin ranging from 0.25% to 1.00%. In each case, the interest

margin applicable to the credit facilities, and the facility fee and letter of credit fees payable under the new revolving credit facility,

are based on the Company’s senior credit ratings as determined by Standard & Poor’s and Moody’s, which are currently BBB and

Baa2, respectively.

There were no balances outstanding on the Company's new Revolving Credit Facility at December 31, 2014 or on its former

revolving credit facility at December 31, 2013.

As of December 31, 2014, the effective interest rate on the new Revolving Credit Facility was 1.1%.

Zero-Coupon Convertible Subordinated Notes

The Company had $106.9 and $128.8 aggregate principal amount at maturity of zero-coupon convertible subordinated notes

(the “notes”) due 2021 outstanding at December 31, 2014 and 2013, respectively. The notes, which are subordinate to the Company’s

bank debt, were sold at an issue price of $671.65 per $1,000.0 principal amount at maturity (representing a yield to maturity of

2.0% per year). Each one thousand dollar principal amount at maturity of the notes is convertible into 13.4108 shares of the

Company’s common stock, subject to adjustment in certain circumstances, if one of the following conditions occurs:

1) If the sales price of the Company’s common stock for at least 20 trading days in a period of 30 consecutive trading days

ending on the last trading day of the preceding quarter reaches specified thresholds (beginning at 120% and declining

0.1282% per quarter until it reaches approximately 110% for the quarter beginning July 1, 2021 of the accreted conversion

price per share of common stock on the last day of the preceding quarter). The accreted conversion price per share will

equal the issue price of a note plus the accrued original issue discount and any accrued contingent additional principal,

divided by the number of shares of common stock issuable upon conversion of a note on that day. The conversion trigger

price for the fourth quarter of 2014 was $73.97.

2) If the credit rating assigned to the notes by Standard & Poor’s Ratings Services is at or below BB-.

3) If the notes are called for redemption.

4) If specified corporate transactions have occurred (such as if the Company is party to a consolidation, merger or

binding share exchange or a transfer of all or substantially all of its assets).

The Company may redeem for cash all or a portion of the notes at any time at specified redemption prices per one thousand

dollar principal amount at maturity of the notes.

The Company has registered the notes and the shares of common stock issuable upon conversion of the notes with the Securities

and Exchange Commission.

During 2014 and 2013, the Company settled notices to convert $21.9 and $25.5 aggregate principal amount at maturity of its

zero-coupon subordinated notes with a conversion value of $28.7 and $31.8, respectively. The total cash used for these settlements

was $18.9 and $21.5 and the Company also issued 0.1 and 0.1 additional shares of common stock, respectively. As a result of

these conversions, in 2014 and 2013 the Company also reversed approximately $3.8 and $3.4, respectively, of deferred tax liability

to reflect the tax benefit realized upon issuance of the shares.

On September 12, 2014, the Company announced that for the period of September 12, 2014 to March 11, 2015, the zero-coupon

subordinated notes will accrue contingent cash interest at a rate of no less than 0.125% of the average market price of a zero-

coupon subordinated note for the five trading days ended September 9, 2014, in addition to the continued accrual of the original

issue discount.

LABORATORY CORPORATION OF AMERICA HOLDINGS AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars and shares in millions, except per share data)