LabCorp 2014 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2014 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

60

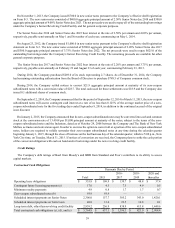

(a) Contingent future licensing payments will be made if certain events take place, such as the launch of a specific test, the transfer

of certain technology, and when specified revenue milestones are met.

(b) As announced by the Company on January 2, 2015, holders of the zero-coupon subordinated notes may choose to convert

their notes during the first quarter of 2015 subject to terms as defined in the note agreement. See “Note 11 to Consolidated

Financial Statements” and "Credit Ratings" above for further information regarding the Company’s zero-coupon subordinated

notes.

(c) The table does not include obligations under the Company’s pension and postretirement benefit plans, which are included in

"Note 16 to Consolidated Financial Statements." Benefits under the Company's postretirement medical plan are made when

claims are submitted for payment, the timing of which is not practicable to estimate.

(d) The table does not include the Company’s reserves for unrecognized tax benefits. The Company had a $24.9 and $34.9 reserve

for unrecognized tax benefits, including interest and penalties, at December 31, 2014 and 2013, respectively, which is included

in “Note 13 to Consolidated Financial Statements.” Substantially all of these tax reserves are classified in other long-term

liabilities in the Company’s Consolidated Balance Sheets at December 31, 2014 and 2013.

(e) This table does not include the $2,900.0 senior notes issued January 30, 2015.

Off-Balance Sheet Arrangements

The Company does not have transactions or relationships with “special purpose” entities, and the Company does not have any

off balance sheet financing other than normal operating leases and letters of credits.

Other Commercial Commitments

As of December 31, 2014, the Company provided letters of credit aggregating approximately $42.5, primarily in connection

with certain insurance programs. Letters of credit provided by the Company are secured by the new Company’s Revolving Credit

Facility and are renewed annually, around mid-year.

On October 14, 2011, the Company issued notice to a noncontrolling interest holder in its Other segment of its intent to purchase

the holder's partnership units in accordance with the terms of the joint venture's partnership agreement. On November 28, 2011,

this purchase was completed for a total purchase price of CN$151.7 as outlined in the partnership agreement (CN$147.8 plus

certain adjustments relating to cash distribution hold backs made to finance recent business acquisitions and capital expenditures).

The purchase of these additional partnership units brings the Company's percentage interest owned to 98.2%.

The contractual value of the remaining noncontrolling interest put totals $17.7 at December 31, 2014. At December 31, 2014

and 2013, $17.7 and $19.4, respectively, have been classified as mezzanine equity in the Company's consolidated balance sheet.

Based on current and projected levels of operations, coupled with availability under its Revolving Credit Facility, the Company

believes it has sufficient liquidity to meet both its anticipated short-term and long-term cash needs; however, the Company

continually reassesses its liquidity position in light of market conditions and other relevant factors.

Covance Drug Development Revenue-Generating Arrangements

The Company expects that Covance Drug Development's revenues will be generated from contractual arrangements that are

similar in structure to Covance’s historical experience. Historically, a majority of revenues have been earned under contracts

that range in duration from a few months to two years, but can extend in duration up to five years or longer. Covance Drug

Development also has committed minimum volume arrangements with certain clients with initial terms that generally range in

duration from three to ten years. Underlying these arrangements are individual project contracts for the specific services to be

provided. These arrangements enable Covance Drug Development's clients to secure its services in exchange for which they

commit to purchase an annual minimum dollar value, or volume, of services. Under these types of arrangements, if the annual

minimum volume commitment is not reached, the client is required to pay Covance Drug Development for the shortfall.

Many of Covance Drug Development's client contracts are either fixed price or with a cap. To a lesser extent,

some of its contracts are without a cap. In cases where the contracts are fixed price, Covance Drug Development

may bear the cost of overruns, or Covance Drug Development may benefit if the costs are lower than anticipated. In cases where

contracts are with a cap, the contracts contain an overall budget for the trial based on time and cost estimates. If

costs are lower than anticipated, the client generally keeps the savings, but if costs are higher than estimated, Covance Drug

Development may be responsible for the overrun unless the increased cost is a result of a scope change or other factors outside