LabCorp 2014 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2014 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

62

Critical Accounting Policies

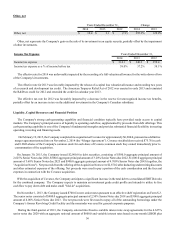

The preparation of financial statements in conformity with generally accepted accounting principles requires management to

make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and

liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported periods.

While the Company believes these estimates are reasonable and consistent, they are by their very nature, estimates of amounts

that will depend on future events. Accordingly, actual results could differ from these estimates. The Company’s Audit Committee

periodically reviews the Company’s significant accounting policies. The Company’s critical accounting policies arise in conjunction

with the following:

• Revenue recognition and allowance for doubtful accounts;

• Pension expense;

• Accruals for self insurance reserves;

• Income taxes; and

• Goodwill and indefinite-lived assets

Revenue recognition and allowance for doubtful accounts

Revenue is recognized for services rendered when the testing process is complete and test results are reported to the ordering

physician. The Company’s sales are generally billed to three types of payers – clients, patients and third parties such as managed

care companies, Medicare and Medicaid. For clients, sales are recorded on a fee-for-service basis at the Company’s client list

price, less any negotiated discount. Patient sales are recorded at the Company’s patient fee schedule, net of any discounts negotiated

with physicians on behalf of their patients, or fees made available through charity care or an uninsured patient program. The

Company bills third-party payers in two ways – fee-for-service and capitated agreements. Fee-for-service third-party payers are

billed at the Company's patient fee schedule amount, and third-party revenue is recorded net of contractual discounts. These

discounts are recorded at the transaction level at the time of sale based on a fee schedule that is maintained for each third-party

payer. The majority of the Company’s third-party sales are recorded using an actual or contracted fee schedule at the time of sale.

For the remaining third-party sales, estimated fee schedules are maintained for each payer. Adjustments to the estimated payment

amounts are recorded at the time of final collection and settlement of each transaction as an adjustment to revenue. These adjustments

are not material to the Company’s results of operations in any period presented. The Company periodically adjusts these estimated

fee schedules based upon historical payment trends. Under capitated agreements with managed care companies, the Company

recognizes revenue based on a negotiated monthly contractual rate for each member of the managed care plan regardless of the

number or cost of services performed.

The Company has a formal process to estimate and review the collectibility of its receivables based on the period of time they

have been outstanding. Bad debt expense is recorded within selling, general and administrative expenses as a percentage of sales

considered necessary to maintain the allowance for doubtful accounts at an appropriate level. The Company’s process for

determining the appropriate level of the allowance for doubtful accounts involves judgment, and considers such factors as the age

of the underlying receivables, historical and projected collection experience, and other external factors that could affect the

collectibility of its receivables. Accounts are written off against the allowance for doubtful accounts based on the Company’s

write-off policy (e.g., when they are deemed to be uncollectible). In the determination of the appropriate level of the allowance,

accounts are progressively reserved based on the historical timing of cash collections relative to their respective aging categories

within the Company’s receivables. These collection and reserve processes, along with the close monitoring of the billing process,

help reduce the risks of material revisions to reserve estimates resulting from adverse changes in collection or reimbursement

experience.