LabCorp 2014 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2014 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

F-13

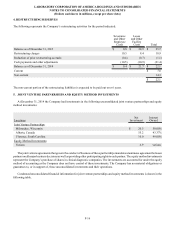

Fair Value of Financial Instruments

Fair value measurements for financial assets and liabilities are determined based on the assumptions that a market participant

would use in pricing an asset or liability. A three-tiered fair value hierarchy draws distinctions between market participant

assumptions based on (i) observable inputs such as quoted prices in active markets (Level 1), (ii) inputs other than quoted prices

in active markets that are observable either directly or indirectly (Level 2) and (iii) unobservable inputs that require the Company

to use present value and other valuation techniques in the determination of fair value (Level 3).

Research and Development

The Company expenses research and development costs as incurred.

New Accounting Pronouncements

In February 2013, the FASB issued a new accounting standard on joint and several liability arrangements for which the total

amount of the obligation is fixed at the reporting date. Under this new standard, obligations resulting from joint and several

liability arrangements are to be measured as the sum of: (a) the amount the reporting entity agreed with its co-obligors that it will

pay and (b) any additional amount the reporting entity expects to pay on behalf of its co-obligors. This standard, which applies

prospectively, became effective for the Company beginning January 1, 2014. The adoption of this standard did not have a material

effect on the consolidated financial statements.

In March 2013, the FASB issued a new accounting standard on foreign currency matters that clarifies the guidance of a parent

company's accounting for the cumulative translation adjustment upon derecognition of certain subsidiaries or groups of assets

within a foreign entity or of an investment in a foreign entity. Under this new standard, a parent company that ceases to have a

controlling financial interest in a foreign subsidiary or group of assets within a foreign entity shall release any related cumulative

translation adjustment into net income only if a sale or transfer results in complete or substantially complete liquidation of the

foreign entity. This standard, which applies prospectively, became effective for the Company beginning January 1, 2014. The

adoption of this standard did not have a material effect on the consolidated financial statements.

In April 2014, the FASB issued a new accounting standard on discontinued operations that significantly changes criteria for

discontinued operations and disclosures for disposals. Under this new standard, to be a discontinued operation, a component or

group of components must represent a strategic shift that has (or will have) a major effect on an entity's operations and financial

results. Expanded disclosures for discontinued operations include more details about earnings and balance sheet accounts, total

operating and investing cash flows, and cash flows resulting from continuing involvement. The guidance is to be applied

prospectively to all new disposals of components and new classifications as held for sale beginning in 2015, with early adoption

allowed in 2014. The adoption of this standard is not expected to have a material impact on the consolidated financial statements.

In May 2014, the FASB issued the converged standard on revenue recognition with the objective of providing a single,

comprehensive model for all contracts with customers to improve comparability in the financial statements of companies reporting

using International Financial Reporting Standards and U.S. Generally Accepted Accounting Principles. The standard contains

principles that an entity must apply to determine the measurement of revenue and timing of when it is recognized. The underlying

principle is that an entity must recognize revenue to depict the transfer of goods or services to customers at an amount that the

entity expects to be entitled to in exchange for those goods or services. An entity can apply the revenue standard retrospectively

to each prior reporting period presented (full retrospective method) or retrospectively with the cumulative effect of initially applying

the standard recognized at the date of initial application in retained earnings. The revenue standard is effective for the Company

beginning January 1, 2017. The Company is currently evaluating the expected impact of the standard.

In August 2014, the FASB issued a new accounting standard that explicitly requires management to assess an entity's ability

to continue as a going concern, and to provide related financial statement footnote disclosures in certain circumstances. Under

this standard, in connection with each annual and interim period, management must assess whether there is substantial doubt about

an entity's ability to continue as a going concern within one year after the financial statements are issued (or available to be issued

when applicable). Management shall consider relevant conditions and events that are known and reasonably knowable at such

issuance date. Substantial doubt about an entity's ability to continue as a going concern exists if it is probable that the entity will

be unable to meet its obligations as they become due within one year after issuance date. Disclosures will be required if conditions

or events give rise to substantial doubt. This standard is effective for the Company for the annual period after December 15, 2016,

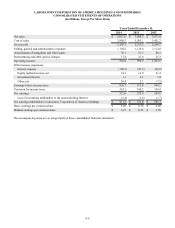

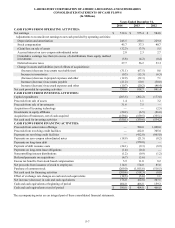

LABORATORY CORPORATION OF AMERICA HOLDINGS AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars and shares in millions, except per share data)