LabCorp 2014 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2014 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

64

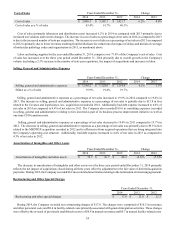

Return on Plan Assets

In establishing its expected return on plan assets assumption, the Company reviews its asset allocation and develops return

assumptions based on different asset classes adjusting for plan operating expenses. Actual asset over/under performance compared

to expected returns will respectively decrease/increase unrecognized loss. The change in the unrecognized loss will change

amortization cost in upcoming periods. A one percentage point increase or decrease in the expected return on plan assets would

have resulted in a corresponding change in 2014 pension expense of $2.6.

Net pension cost for 2014 was $8.1 as compared with $11.0 in 2013 and $12.1 in 2012. The decrease in pension expense was

due to decreases in the amount of net amortization and deferral. The decrease in pension expense in 2013 was due decrease in

pension expense was due to decreases in the amount of net amortization and deferral as a result of higher discount rates. Projected

pension expense for the Company Plan and the PEP is expected to increase to $11.6 in 2015 as a result of a lower assumed discount

rate and changes in participant mortality tables.

Further information on the Company’s defined benefit retirement plan is provided in Note 16 to the consolidated financial

statements.

Accruals for Self-insurance Reserves

Accruals for self-insurance reserves (including workers’ compensation, auto and employee medical) are determined based on

a number of assumptions and factors, including historical payment trends and claims history, actuarial assumptions and current

and estimated future economic conditions. These estimated liabilities are not discounted.

The Company is self-insured (up to certain limits) for professional liability claims arising in the normal course of business,

generally related to the testing and reporting of laboratory test results. The Company maintains excess insurance which limits the

Company’s maximum exposure on individual claims. The Company estimates a liability that represents the ultimate exposure for

aggregate losses below those limits. The liability is discounted and is based on actuarial assumptions and factors for known and

incurred but not reported claims, including the frequency and payment trends of historical claims.

If actual trends differ from these estimates, the financial results could be impacted. Historical trends have not differed materially

from these estimates.

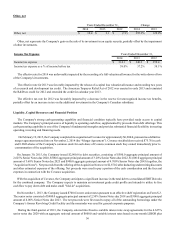

Income Taxes

The Company accounts for income taxes utilizing the asset and liability method. Under this method deferred tax assets and

liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying

amounts of existing assets and liabilities and their respective tax bases and for tax loss carryforwards. Deferred tax assets and

liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences

are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in

income in the period that includes the enactment date. The Company does not recognize a tax benefit, unless the Company concludes

that it is more likely than not that the benefit will be sustained on audit by the taxing authority based solely on the technical merits

of the associated tax position. If the recognition threshold is met, the Company recognizes a tax benefit measured at the largest

amount of the tax benefit that the Company believes is greater than 50% likely to be realized. The Company records interest and

penalties in income tax expense.

Goodwill and Indefinite-Lived Assets

The Company assesses goodwill and indefinite-lived intangibles for impairment at least annually and more frequently if

triggering events occur. The timing of the Company's annual impairment testing is the end of the fiscal year. In accordance with

the Financial Accounting Standards Board (“FASB”) updates to their authoritative guidance regarding goodwill and indefinite-

lived intangible asset impairment testing, an entity is allowed to first assess qualitative factors as a basis for determining whether

it is necessary to perform quantitative impairment testing. If an entity determines that it is not more likely than not that the estimated

fair value of an asset is less than its carrying value, then no further testing is required. Otherwise, impairment testing must be

performed in accordance with the original accounting standards. The updated FASB guidance also allows an entity to bypass the

qualitative assessment for any reporting unit in its goodwill assessment and proceed directly to performing the first step of the

two-step assessment. Similarly, a Company can proceed directly to a quantitative assessment in the case of impairment testing

for indefinite-lived intangible assets as well. In 2014 and 2013, the Company elected to bypass the purely qualitative assessments

for its goodwill and indefinite-lived intangible assets and proceed to quantitative assessments utilizing methodologies as described

in the following paragraphs.