LabCorp 2015 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2015 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

|

|

Index

from 0.125% to 0.40%. The interest margin applicable to the credit facilities, and the facility fee and letter of credit fees payable under the new revolving

credit facility, are based on the Company’s senior credit ratings as determined by Standard & Poor’s and Moody’s, which are currently BBB and Baa2,

respectively.

As of December 31, 2015, the effective interest rate on the revolving credit facility was 1.5% and the effective interest rate on the term loan was 1.7%.

Net cash used for financing activities for the year ended December 31, 2014 was $200.6 compared to $518.3 for the year ended December 31, 2013. The

$317.7 decrease in the cash used for financing activities for the year ended December 31, 2014, as compared to the prior year, was primarily a result of a

$746.6 decrease in repurchases of common stock partially offset by a net increase of $328.5 in debt financing in 2013.

As of December 31, 2015, the Company provided letters of credit aggregating $45.4, primarily in connection with certain insurance programs. Letters of

credit provided by the Company are issued under the Company's revolving credit facility and are renewed annually, around mid-year.

As of December 31, 2015, the Company had outstanding authorization from the Board of Directors to purchase up to $789.5 of Company common stock

based on settled trades as of that date. Following the announcement of the Acquisition in the fourth quarter of 2014, the Company suspended its share

repurchases. The Company does not anticipate resuming its share repurchase activity until it approaches its targeted leverage ratio of total debt to

consolidated EBITDA of 2.5 to 1.0. However, the Company will continue to evaluate all opportunities for strategic deployment of capital in light of market

conditions.

The Company had a $36.9 and $24.9 reserve for unrecognized income tax benefits, including interest and penalties as of December 31, 2015 and

December 31, 2014, respectively. The Acquisition accounted for substantially all of the increase. Substantially all of these tax reserves are classified in other

long-term liabilities in the Company's Consolidated Balance Sheets at December 31, 2015 and December 31, 2014.

On September 11, 2015, the Company announced that for the period of September 12, 2015 to March 11, 2016, the zero-coupon subordinated notes will

accrue contingent cash interest at a rate of no less than 0.125% of the average market price of a zero-coupon subordinated note for the five trading days ended

September 9, 2015, in addition to the continued accrual of the original issue discount.

On January 4, 2016, the Company announced that its zero-coupon subordinated notes may be converted into cash and common stock at the conversion

rate of 13.4108 per $1,000 principal amount at maturity of the notes, subject to the terms of the zero-coupon subordinated notes and the Indenture, dated as

of October 24, 2006 between the Company and The Bank of New York Mellon, as trustee and conversion agent. In order to exercise the option to convert all

or a portion of the zero-coupon subordinated notes, holders are required to validly surrender their zero-coupon subordinated notes at any time during the

calendar quarter beginning January 1, 2016, through the close of business on the last business day of the calendar quarter, which is 5:00 p.m., New York City

time, on Thursday, March 31, 2016. If notices of conversion are received, the Company plans to settle the cash portion of the conversion obligation with cash

on hand and/or borrowings under the new revolving credit facility.

The Company’s debt ratings of Baa2 from Moody’s and BBB from S&P’s contribute to its ability to access capital markets.

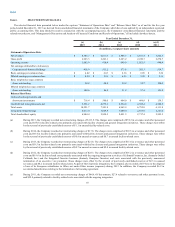

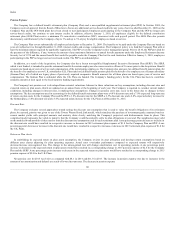

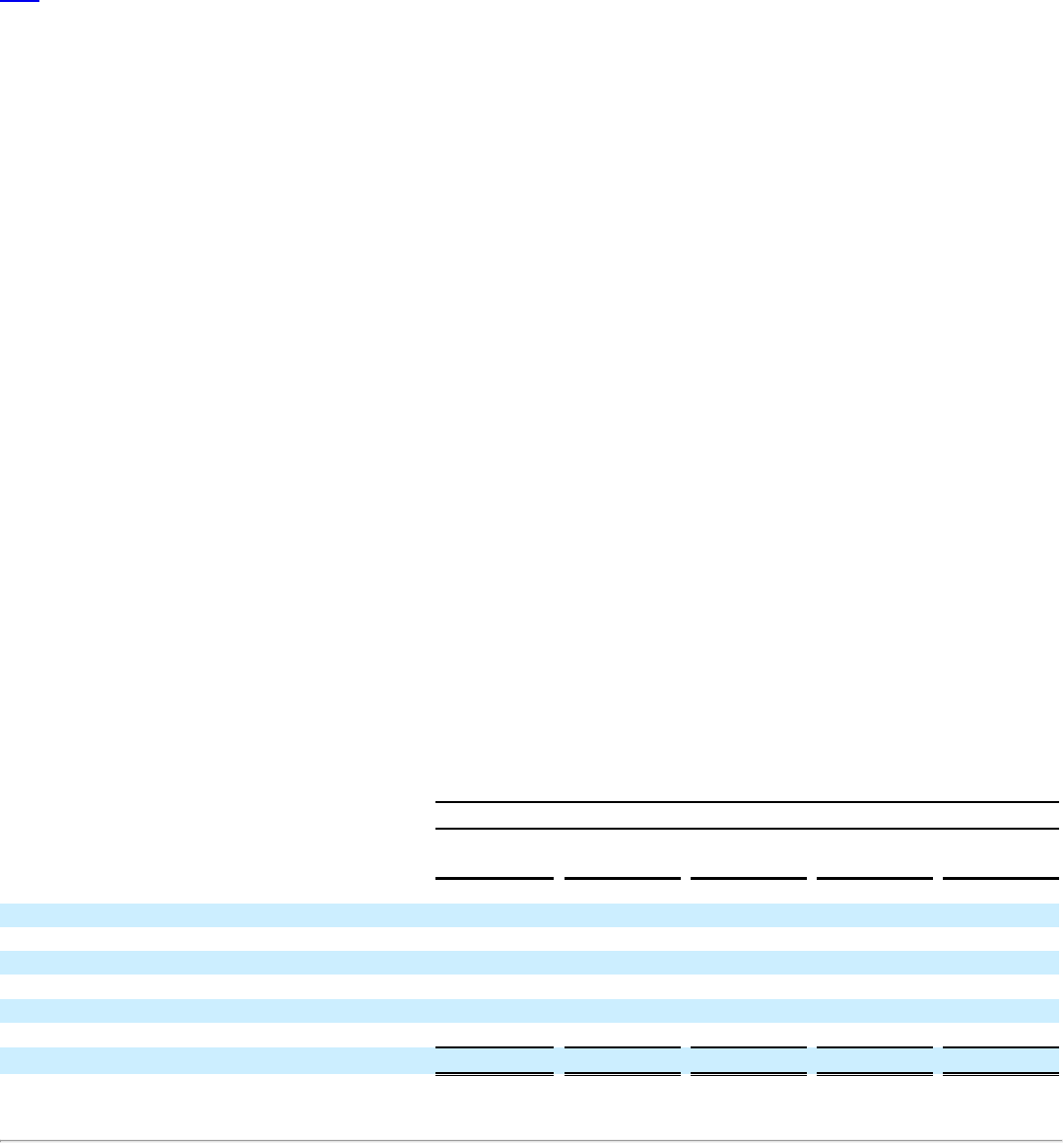

Payments Due by Period

2017-

2019-

2021 and

Total

2016

2018

2020

thereafter

Operating lease obligations $ 346.0

$ 73.4

$ 108.0

$ 59.6

$ 105.0

Contingent future licensing payments (a) 18.2

3.4

7.2

4.4

3.2

Minimum royalty payments 5.9

1.0

1.9

2.0

1.0

Purchase obligations 60.0

29.5

28.4

2.1

—

Scheduled interest payments on Senior Notes 2,148.2

197.7

364.0

326.4

1,260.1

Scheduled interest payments on Term Loan 62.0

14.5

31.6

15.9

—

Long-term debt, other than revolving credit facility 5,525.0

325.0

900.0

1,100.0

3,200.0

Total contractual cash obligations (b) and (c) $ 8,165.3

$ 644.5

$ 1,441.1

$ 1,510.4

$ 4,569.3

55