LabCorp 2015 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2015 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

|

|

Index

In some cases, payments received are in excess of revenue recognized. For example, a contract invoicing schedule may provide for an upfront payment of

10% of the full contract value upon contract signing, but at the time of signing performance of services has not yet begun. Payments received in advance of

services being provided are deferred as unearned revenue on the balance sheet. As the contracted services are subsequently performed and the associated

revenue is recognized, the unearned revenue balance is reduced by the amount of revenue recognized during the period.

In other cases, services may be provided and revenue recognized before the client is invoiced. In these cases, revenue recognized will exceed amounts

billed, and the difference, representing an unbilled receivable, is recorded for the amount that is currently unbillable to the customer pursuant to contractual

terms. Once the client is invoiced, the unbilled services are reduced for the amount billed, and a corresponding account receivable is recorded. All unbilled

services are billable to customers within one year from the respective balance sheet date.

Most contracts are terminable with or without cause by the client, either immediately or upon notice. These contracts often require payment to CDD of

expenses to wind down the study or project, fees earned to date and, in some cases, a termination fee or a payment to CDD of some portion of the fees or

profits that could have been earned by CDD under the contract if it had not been terminated early. Termination fees are included in net revenues when

services are performed and realization is assured. In connection with the management of multi-site clinical trials, CDD pays on behalf of its customers fees to

investigators, volunteers and certain out-of-pocket costs, for which it is reimbursed at cost, without mark-up or profit. Investigator fees are not reflected in net

revenues or expenses where CDD acts in the capacity of an agent on behalf of the pharmaceutical company sponsor, passing through these costs without risk

or reward to CDD. All other out-of-pocket costs are included in total revenues and expenses.

LCD has a formal process to estimate and review the collectibility of its receivables based on the period of time they have been outstanding. Bad debt

expense is recorded within selling, general and administrative expenses as a percentage of sales considered necessary to maintain the allowance for doubtful

accounts at an appropriate level. LCD’s process for determining the appropriate level of the allowance for doubtful accounts involves judgment and

considers such factors as the age of the underlying receivables, historical and projected collection experience, and other external factors that could affect the

collectibility of its receivables. Accounts are written off against the allowance for doubtful accounts based on LCD’s write-off policy (e.g. , when they are

deemed to be uncollectible). In the determination of the appropriate level of the allowance, accounts are progressively reserved based on the historical

timing of cash collections relative to their respective aging categories within LCD’s receivables. These collection and reserve processes, along with the close

monitoring of the billing process, help reduce the risks of material revisions to reserve estimates resulting from adverse changes in collection or

reimbursement experience.

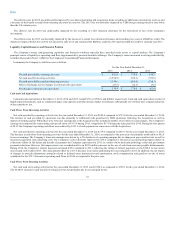

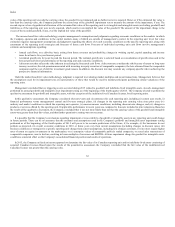

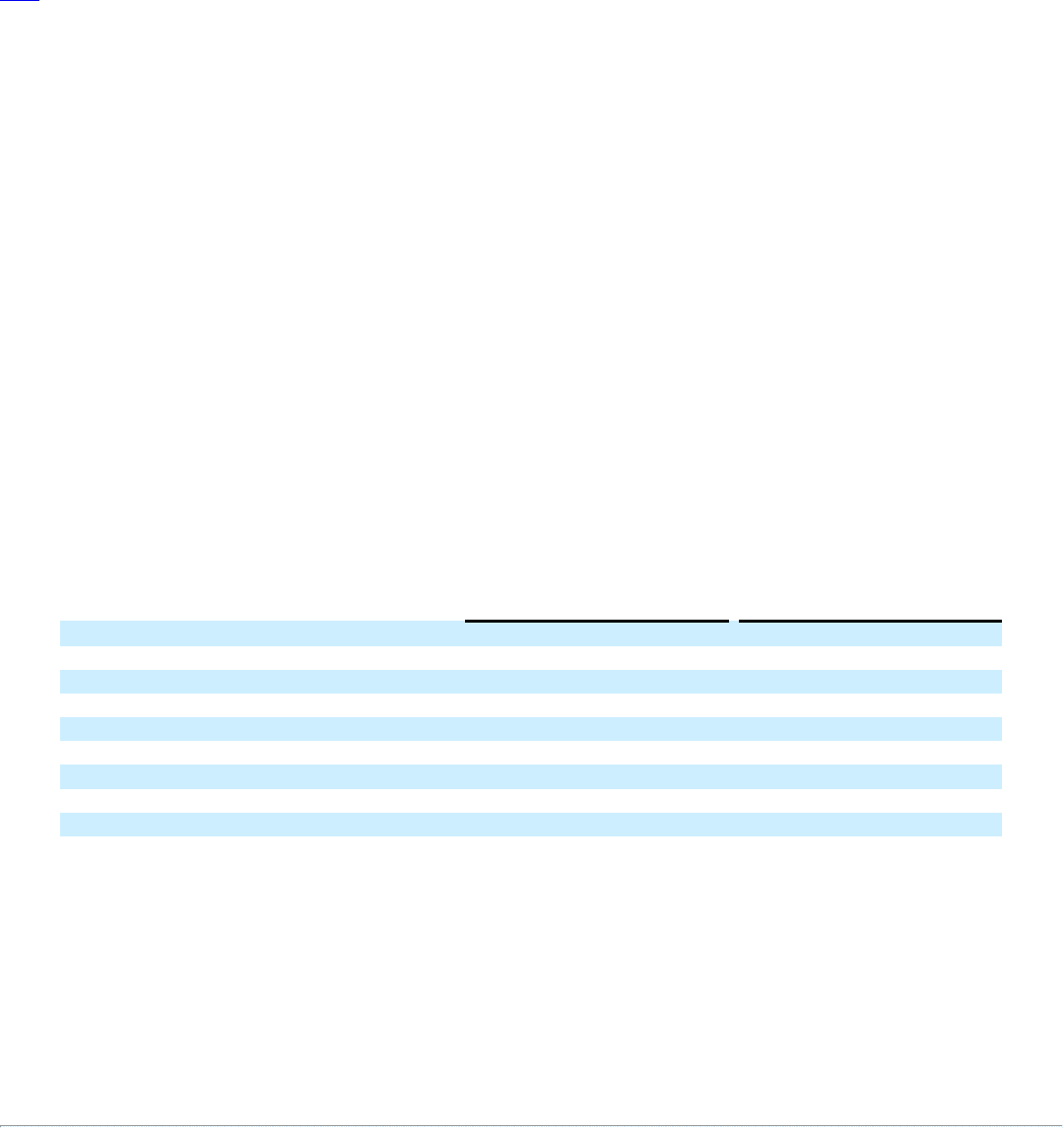

The following table presents the percentage of LCD’s net accounts receivable outstanding by aging category at December 31, 2015 and 2014:

0 – 30 46.8%

48.4%

31 – 60 16.9%

18.6%

61 – 90 12.1%

11.9%

91 – 120 7.4%

7.1%

121 – 150 4.4%

3.8%

151 – 180 4.1%

3.6%

181 – 270 7.1%

5.7%

271 – 360 1.1%

0.7%

Over 360 0.1%

0.1%

The above table excludes the percentage of net accounts receivable outstanding by aging category for certain foreign operations, BeaconLBS, and the

nutritional chemistry and food safety business. Combined these net accounts receivable balances comprise less than 6.7% of LCD's total net accounts

receivable balances. The Company believes that including the agings of the accounts receivables for these would not be representative of the majority of

accounts receivable by aging category for LCD. The majority of the accounts receivables for the foreign operations, BeaconLBS, and the nutritional

chemistry and food safety business are generally paid within 30 to 60 days of billing.

CDD endeavors to assess and monitor the creditworthiness of its customers to which it grants credit terms in the ordinary course of business. CDD

maintains a provision for doubtful accounts relating to amounts due that may not be collected. This bad debt provision is monitored on a monthly basis and

adjusted as circumstances warrant. Since the recorded bad debt provision is based upon management's judgment, actual bad debt write-offs may be greater or

less than the amount recorded. Historically, bad debt write-offs have not been material. The allowance for doubtful accounts amounted to $3.4 at

December 31, 2015.

59