LabCorp 2015 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2015 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

|

|

Index

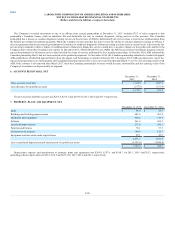

Also included in prepaid expenses and other current assets are assets held for sale. The Company records long-lived assets as held for sale when a plan to

sell the asset has been initiated and all other held for sale criteria have been satisfied. Assets classified as held for sale of $72.4 as of December 31, 2015 are

recorded in other current assets on the consolidated balance sheet at the lower of their carrying value or fair value less cost to sell. There were no assets held

for sale as of December 31, 2014.

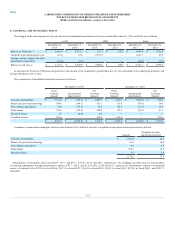

Property, plant and equipment are recorded at cost. The cost of properties held under capital leases is equal to the lower of the net present value of the

minimum lease payments or the fair value of the leased property at the inception of the lease. Depreciation and amortization expense is computed on all

classes of assets based on their estimated useful lives, as indicated below, using the straight-line method.

Years

Buildings and building improvements 10 - 40

Machinery and equipment 3 - 10

Furniture and fixtures 5 - 10

Software 3 - 10

Leasehold improvements and assets held under capital leases are amortized over the shorter of their estimated useful lives or the term of the related leases.

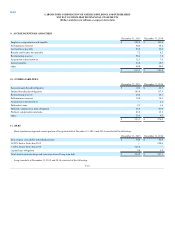

Expenditures for repairs and maintenance are charged to operations as incurred. Retirements, sales and other disposals of assets are recorded by removing the

cost and accumulated depreciation from the related accounts with any resulting gain or loss reflected in the consolidated statements of operations.

The Company capitalizes purchased software which is ready for service and capitalizes software development costs incurred on significant projects

starting from the time that the preliminary project stage is completed and the Company commits to funding a project until the project is substantially

complete and the software is ready for its intended use. Capitalized costs include direct material and service costs and payroll and payroll-related costs.

Research and development (R&D) costs and other computer software maintenance costs related to software development are expensed as incurred.

Capitalized software costs are amortized using the straight-line method over the estimated useful life of the underlying system, generally five years.

The Company assesses goodwill and indefinite-lived intangibles for impairment at least annually or whenever events or changes in circumstances

indicate that the carrying amount of such assets may not be recoverable. In 2015, the Company changed the timing of its annual impairment testing from the

end of the year to the beginning of the fourth quarter. In accordance with the FASB updates to their authoritative guidance regarding goodwill and

indefinite-lived intangible asset impairment testing, an entity is allowed to first assess qualitative factors as a basis for determining whether it is necessary to

perform quantitative impairment testing. If an entity determines that it is not more likely than not that the estimated fair value of an asset is less than its

carrying value, then no further testing is required. Otherwise, impairment testing must be performed in accordance with the original accounting standards.

The updated FASB guidance also allows an entity to bypass the qualitative assessment for any reporting unit in its goodwill assessment and proceed directly

to performing the first step of the two-step assessment. Similarly, a company can proceed directly to a quantitative assessment in the case of impairment

testing for indefinite-lived intangible assets as well.

Step One of the goodwill impairment test includes the estimation of the fair value of each reporting unit as compared to the carrying value of the

reporting unit. Reporting units are businesses with discrete financial information that is available and reviewed by management. The Company estimates the

fair value of a reporting unit using both income-based and market-based valuation methods. The income-based approach is based on the reporting unit's

forecasted future cash flows that are discounted to the present value using the reporting unit's weighted average cost of capital. For the market-based

approach, the Company utilizes a number of factors such as publicly available information regarding the market capitalization of the Company as well as

operating results, business plans, market multiples, and present value techniques. Based upon the range of estimated values developed from the income and

market-based methods, the Company determines the estimated fair value for the reporting unit. If the estimated fair value of the reporting unit exceeds the

carrying value, the goodwill is not impaired and no further review is required. However, if the estimated fair value is less than the carrying value, the

Company performs the second step of the goodwill impairment test is performed to measure the amount of the impairment, if any. The second step involves a

hypothetical allocation of the estimated fair value of the reporting unit to its tangible and intangible assets (excluding goodwill) and liabilities as if the

reporting unit were newly acquired, which results in an implied fair value of the goodwill. The amount of the impairment charge is the excess of the recorded

goodwill, if any, over the implied fair value of the goodwill.

F-12