Lowe's 2006 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2006 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

18

Lowe’s 2006 Annual Report

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

is discussion and analysis summarizes the signicant factors aecting

our consolidated operating results, nancial condition, liquidity and

capital resources during the three-year period ended February 2, 2007

(our scal years 2006, 2005 and 2004). Fiscal years 2006 and 2004 con-

tain 52 weeks of operating results compared to scal year 2005 which

contains 53 weeks. Unless otherwise noted, all references herein for the

years 2006, 2005 and 2004 represent the scal years ended February 2,

2007, February 3, 2006, and January 28, 2005, respectively. is discus-

sion should be read in conjunction with the consolidated nancial state-

ments and notes to the consolidated nancial statements included in this

annual report.

EXECUTIVE OVERVIEW

External Factors Impacting Our Business

e home improvement market is large and fragmented. While we are

the world’s second-largest home improvement retailer, we have captured

a relatively small portion of the overall home improvement market. We

estimate the size of the U.S. home improvement market to be approxi-

mately $725 billion annually, comprised of $560 billion of product demand

and $165 billion of installed labor opportunity. is data captures a wide

range of categories relevant to our business, including major appliances

and garden supplies. We believe the current home improvement market

provides ample opportunity to support our growth plans.

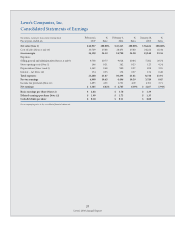

Net sales totaled $46.9 billion in 2006, an increase of 8.5% versus the

prior year. is increase was driven by our store expansion program. e

additional week in 2005 resulted in approximately $750 million in addi-

tional net sales in 2005. Excluding the additional week, net sales would

have increased approximately 10% in 2006. However, comparable store

sales were at in 2006. e eects of a slowing housing market, dicult

comparisons to 2005’s hurricane recovery and rebuilding eorts, and

signicant deation in lumber and plywood retail prices contributed to

lower than expected sales.

At the beginning of 2006, many markets including areas of the

Northeast, southern Florida and the west coast demonstrated signs of

slowing housing-related demand. at evidence led us to estimate housing

turnover would decline in 2006 as these once-hot markets cooled. What

was more dicult to anticipate was the decline in home improvement

demand that we experienced in many unaected markets where housing

dynamics remained solid, but consumers chose to delay home improve-

ment projects due to well-publicized reports of a slowing housing market

and declining home values. As the year progressed, housing turnover

slowed more quickly and deeply than we had originally anticipated. at

rapid decline also pressured home prices as speculative demand waned,

housing supply grew and home buyers, as well as home improvement

consumers, became cautious about spending. We continue to closely

monitor the drivers of demand and the mindset of the home improvement

consumer as we enter 2007.

Despite the housing-related pressures on the consumer, the job market

remains solid and personal disposable income continues to rise. In addi-

tion, the dicult sales comparisons due to 2005’s hurricanes and last year’s

commodity deflation are expected to ease in 2007. While we are not

expecting a rapid recovery, the most recent housing data shows encour-

aging signs of a stabilization of housing supply and a bottoming in total

housing turnover. Based on all these external factors, combined with our

internal initiatives to drive sales, we believe the quarterly trend of declining

comparable store sales performance has bottomed, and we expect to see

gradual improvement in comparable store sales throughout 2007.

Managing for the Long-Term

We continue to manage our business for the long-term. Our vision is to

provide customer-valued solutions with the best prices, products and

services to make Lowe’s the rst choice for home improvement. In today’s

environment, it is important that we remain focused on customers. is

focus on customers drives our operational, merchandising, marketing

and distribution initiatives to both capture market share and improve

operating eciency.

Capturing Market Share

Investing in existing stores

We continue to gain unit market share by improving the shopping experi-

ence in our stores, and by adding innovative products and services that

provide value to customers. In addition, we have opportunities to capture

additional unit market share in each of our 20 product categories by ensur-

ing that we meet the needs of home improvement customers better than

our competitors.

We have consistently invested in our business and we will continue to

do so, to ensure our stores remain clean, easy to shop and appropriately

staed in order to maintain our customer franchise and grow unit mar-

ket share. In 2006, we remerchandised 150 of our earlier-format stores to

make them more closely resemble our current store prototypes, with

minimal disruption to our customers. ese remerchandising eorts

focused on moving entire departments, improving adjacencies, and

enhancing the shopability within the appliances, cabinets & countertops,

ooring, fashion plumbing, paint, walls/windows, lighting, home orga-

nization, lumber and building materials departments. In addition, we

replaced or refurbished all of our selling centers, including the returns

and customer service areas of these stores. All new interior graphics, sig-

nage, and way-nding materials were also added to increase shopability

and brighten the atmosphere. Finally, we installed self-check-out in all

150 of our remerchandised stores. In 2007, we expect to complete the

remerchandising process in over 100 additional stores. We continuously

make these investments to maintain our best-in-class stores and oer cus-

tomers the shopping experience and environment they expect. As a result,

despite the external pressures we faced in 2006, we gained 110 basis points

of unit market share among all 20 of our product categories, according to

independent measures, a clear indication that more customers are choosing

Lowe’s for their home improvement needs.

Specialty Sales

We recognize the opportunity that our Specialty Sales initiatives represent

and the importance of these businesses to our long-term growth. Our

Specialty Sales initiatives include three major categories: Installed Sales,

Special Order Sales and Commercial Business Customer sales, internally

referred to as the “Big 3.” In addition, our eort to utilize e-Commerce to

drive sales and conveniently provide product information to customers

is managed by our Specialty Sales group. Our Big 3 Specialty Sales initia-

tives had mixed results in 2006. A hesitation to take on large projects by

some consumers had an impact on our Installed Sales and Special Order

Sales in the second half of 2006. Installed Sales increased by slightly more

than the Company average, while Special Order Sales increased less than

the Company average. However, sales growth for Commercial Business

Customers was nearly double the Company average.

We also continue to rene our oerings, including an ongoing test

of an in-home selling model for certain Installed Sales categories, new

Special Order electronic selling tools, and many enhancements to

Lowes.com, to continue growth in these areas for 2007.