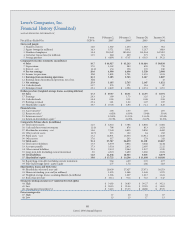

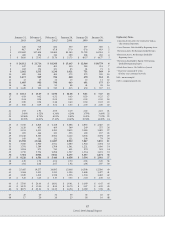

Lowe's 2006 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2006 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

|

|

38

Lowe’s 2006 Annual Report

for homogeneous employee groups. Prior to the adoption of the fair

value recognition provisions of SFAS No. 123(R), share-based payment

expense was adjusted for actual forfeitures as they occurred. is transition

resulted in a pre-tax cumulative eect adjustment of $10 million as of

February 4, 2006. e cumulative eect adjustment was presented as a

reduction of share-based payment expense in the rst quarter of 2006.

e Company recognized share-based payment expense in SG&A

expense on the consolidated statements of earnings totaling $62 million,

$76 million and $70 million in 2006, 2005 and 2004, respectively. e

total income tax benet recognized was $18 million, $19 million and

$16 million in 2006, 2005 and 2004, respectively.

Total unrecognized share-based payment expense for all share-based

payment plans was $103 million at February 2, 2007, of which $51 million

will be recognized in 2007, $34 million in 2008 and $18 million thereaer.

is results in these amounts being recognized over a weighted-average

period of 1.2 years.

Prior to the adoption of SFAS No. 123(R), the Company presented all

tax benets of deductions resulting from the exercise of stock options as

operating cash ows in the consolidated statements of cash ows. SFAS

No. 123(R) requires the cash ows resulting from the tax benets of

deductions in excess of the compensation cost recognized for those options

(excess tax benets) to be classied as nancing cash ows. In accordance

with the modied-prospective-transition method of SFAS No. 123(R),

the prior period consolidated statements of cash ows have not been

restated to reect this change.

As the Company adopted the fair-value recognition provisions of

SFAS No. 123 prospectively for all employee awards granted or modied

aer January 31, 2003, share-based payment expense included in the

determination of net earnings for years ended February 3, 2006 and

January 28, 2005 is less than that which would have been recognized if

the fair-value-based method had been applied to all awards since the

original eective date of SFAS No. 123. e following table illustrates

the eect on net earnings and earnings per share in the period if the

fair-value-based method had been applied to all outstanding and

unvested awards.

(In millions, except per share data) 2005 2004

Net earnings as reported $2,765 $2,167

Add: Stock-based compensation expense included

in net earnings, net of related tax eects 57 53

Deduct: Total stock-based compensation expense

determined under the fair-value-based method

for all awards, net of related tax eects (59) (95)

Pro forma net earnings $2,763 $2,125

Earnings per share:

Basic – as reported $ 1.78 $ 1.39

Basic – pro forma $ 1.78 $ 1.37

Diluted – as reported $ 1.73 $ 1.35

Diluted – pro forma $ 1.73 $ 1.32

Overview of Share-Based Payment Plans

e Company has (a) four equity incentive plans, referred to as the “2006,”

“2001,” “1997,” and “1994” Incentive Plans, (b) one share-based plan for

awards to non-employee directors and (c) an employee stock purchase

plan (ESPP) that allows employees to purchase Company shares through

payroll deductions. ese plans contain a nondiscretionary antidilution

provision that is designed to equalize the value of an award as a result of an

equity restructuring. Share-based awards in the form of incentive and

non-qualied stock options, performance accelerated restricted stock

(PARS), restricted stock and deferred stock units may be granted to key

employees from the 2006 plan. No new awards may be granted from the

2001, 1997 and 1994 plans.

e share-based plan for non-employee directors is referred to as the

Amended and Restated Directors’ Stock Option and Deferred Stock Unit

Plan (Directors’ Plan). Prior to the amendment to the Directors’ Plan in

2005, each non-employee Director was awarded 8,000 options on the date

of the rst Board meeting aer each annual meeting of the Company’s

shareholders, which occurs in the second quarter of each scal year.

Since the amendment to the Directors’ Plan in 2005, each non-employee

Director is awarded a number of deferred stock units determined by

dividing the annual award amount by the fair market value of a share of

the Company’s common stock on the award date and rounding up to the

next 100 units. e annual award amount used to determine the number

of deferred stock units granted to each director was $115,000 and $85,000

in 2006 and 2005, respectively.

Share-based awards were authorized for grant to key employees and

non-employee directors for up to 169.0 million shares of common stock.

Stock options were authorized for up to 129.2 million shares, while PARS,

restricted stock and deferred stock units, which represent nonvested

stock, were authorized for up to 39.8 million shares of common stock.

At February 2, 2007, there were 49.8 million shares available for grant

under the 2006 and Directors’ Plans, and 1.3 million shares available

under the ESPP.

General terms and methods of valuation for the Company’s share-based

awards are as follows:

Stock Options

Stock options generally have terms of seven years, with normally one-

third of each grant vesting each year for three years, and are assigned

an exercise price of not less than the fair market value of a share of the

Company’s common stock on the date of grant.

e fair value of each option grant is estimated on the date of grant

using the Black-Scholes option-pricing model. When determining

expected volatility, the Company considers the historical performance

of the Company’s stock, as well as implied volatility. e risk-free interest

rate is based on the U.S. Treasury yield curve in eect at the time of grant,

based on the options’ expected term. e expected term of the options is

based on the Company’s evaluation of option holders’ exercise patterns

and represents the period of time that options are expected to remain

unexercised. e Company uses historical data to estimate the timing

and amount of forfeitures. ese options are expensed on a straight-line

basis over the vesting period, which is considered to be the requisite

service period. e assumptions used in the Black-Scholes option-

pricing model for options granted in the three years ended February 2,

2007, February 3, 2006 and January 28, 2005 were as follows:

2006 2005 2004

Assumptions used:

Expected volatility 22.3%–29.4% 25.8%–34.1% 31.6%–41.4%

Weighted-average

expected volatility 26.8% 31.4% 38.3%

Expected dividend yield 0.27%–0.31% 0.23%–0.28% 0.21%–0.23%

Weighted-average

dividend yield 0.28% 0.24% 0.22%

Risk-free interest rate 4.54%–4.97% 3.76%–4.44% 2.18%–3.46%

Weighted-average risk-free

interest rate 4.69% 3.81% 2.39%

Expected term, in years 3–4 3–4 3–4

Weighted-average expected

term, in years 3.57 3.22 3.27

e weighted-average grant-date fair value per share of options granted

was $8.86, $7.81 and $8.28 in 2006, 2005 and 2004, respectively. e total

intrinsic value of options exercised, representing the dierence between

the exercise price and the market price on the date of exercise, was approxi-

mately $80 million, $175 million and $76 million in 2006, 2005 and

2004, respectively.