Lowe's 2006 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2006 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

21

Lowe’s 2006 Annual Report

Although we believe we have sucient current and historical knowl-

edge to record reasonable estimates of sales returns, it is possible that actual

returns could dier from recorded amounts. A 1% change in actual returns

would have aected net earnings for 2006 by approximately $3 million. A

1% change in the average return period would not have had a signicant

impact on net earnings for 2006.

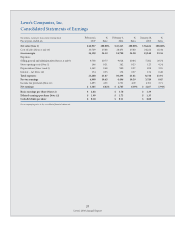

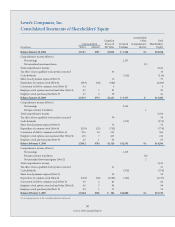

OPERATIONS

e following table sets forth the percentage relationship to net sales of

each line item of the consolidated statements of earnings, as well as the

percentage change in dollar amounts from the prior year. is table should

be read in conjunction with the following discussion and analysis and

the consolidated nancial statements, including the related notes to the

consolidated nancial statements.

Basis Point Percentage

Increase/ Increase/

(Decrease) (Decrease)

in Percentage in Dollar

of Net Sales Amounts

from from

Prior Year

1

Prior Year

1

2006 vs. 2006 vs.

2006 2005 2005 2005

Net sales 100.00% 100.00% N/A 9%

Gross margin 34.52 34.20 32 10

Expenses:

Selling, general

and administrative 20.75 20.84 (9) 8

Store opening costs 0.31 0.33 (2) 3

Depreciation 2.48 2.27 21 19

Interest – net 0.33 0.37 (4) (3)

Total expenses 23.87 23.81 6 9

Pre-tax earnings 10.65 10.39 26 11

Income tax provision 4.03 4.00 3 9

Net earnings 6.62% 6.39% 23 12%

Basis Point Percentage

Increase/ Increase/

(Decrease) (Decrease)

in Percentage in Dollar

of Net Sales Amounts

from from

Prior Year

1

Prior Year

1

2005 vs. 2005 vs.

2005 2004 2004 2004

Net sales 100.00% 100.00% N/A 19%

Gross margin 34.20 33.56 64 21

Expenses:

Selling, general

and administrative 20.84 20.74 10 19

Store opening costs 0.33 0.34 (1) 15

Depreciation 2.27 2.35 (8) 14

Interest – net 0.37 0.48 (11) (10)

Total expenses 23.81 23.91 (10) 18

Pre-tax earnings 10.39 9.65 74 28

Income tax provision 4.00 3.71 29 28

Net earnings 6.39% 5.94% 45 28%

Other Metrics 2006 2005 2004

Comparable store

sales increases2 0.0% 6.1% 6.6%

Customer transactions (in millions)

1

680 639 575

Average ticket1,3 $ 68.98 $ 67.67 $ 63.43

At end of year:

Number of stores 1,385 1,234 1,087

Sales oor square feet (in millions) 157 140 124

Average store size selling

square feet (in thousands) 113 113 114

Return on beginning assets1,4 12.6% 13.1% 11.6%

Return on beginning

shareholders’ equity

1,5

21.7% 24.0% 21.3%

1 e scal years ended February 2, 2007 and January 28, 2005 had 52 weeks. e scal year

ended February 3, 2006 had 53 weeks.

2 We dene a comparable store as a store that has been open longer than 13 months. A store that

is identied for relocation is no longer considered comparable one month prior to its relocation.

e relocated store must then remain open longer than 13 months to be considered comparable.

e comparable store sales increase for 2006 included in the preceding table was calculated using

sales for a comparable 52-week period, while the comparable store sales increase for 2005 was

calculated using sales for a comparable 53-week period.

3 We dene average ticket as net sales divided by number of customer transactions.

4 Return on beginning assets is dened as net earnings divided by beginning total assets.

5 Return on beginning shareholders’ equity is dened as net earnings divided by beginning

shareholders’ equity.

Fiscal 2006 Compared to Fiscal 2005

For the purpose of the following discussion, comparable store sales,

comparable store average ticket and comparable store customer transac-

tions are based on comparable 52-week periods.

Net sales

Our continued focus on executing the fundamentals and providing cus-

tomer-valued solutions together with our store expansion program

drove sales of $46.9 billion in 2006. We opened 155 stores in 2006,

including four relocations, and ended the year with 1,385 stores in 49 states.

e additional week in 2005 resulted in approximately $750 million in

additional net sales in 2005. Excluding the additional week, net sales

would have increased approximately 10% in 2006.

Comparable store sales were at in 2006 versus a comparable store

sales increase of 6.1% in 2005. Average ticket for comparable stores

increased slightly versus the prior year, but comparable store customer

transactions declined slightly.

Although nine of our 21 regions had comparable store sales increases

for 2006, sales in many areas of the country were pressured by the slowdown

in the housing market. Markets in the Northeast, Florida and California

were most exposed to the slowdown in housing in 2006. Sales trends in

those areas clearly indicated a cautious home improvement consumer.

Also, areas of the Gulf Coast and Florida, which experienced increased

demand in 2005 related to rebuilding from the hurricanes, experienced

comparable store sales declines in the second half of 2006. We expect the

dicult sales comparisons to ease in the second half of 2007 as we pass

the second anniversary of Hurricanes Katrina, Rita and Wilma.

Reective of the dicult sales environment, only 11 of our 20 product

categories experienced comparable store sales increases in 2006. e

categories that performed above our average comparable store sales change

included rough plumbing, building materials, rough electrical, home

environment, paint, fashion plumbing, ooring, nursery, seasonal living,

and lawn & landscape products. In addition, hardware performed at

approximately our average comparable store sales change in 2006. Despite

the dicult sales environment, we were able to gain unit market share in

all of our 20 product categories versus the prior calendar year, according

to third-party estimates.