McDonalds 2011 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2011 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

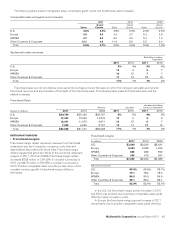

(denominator), primarily capital expenditures. The calculation

uses a constant average foreign exchange rate over the peri-

ods included in the calculation.

STRATEGIC DIRECTION AND FINANCIAL PERFORMANCE

The strength of the alignment between the Company, its franchi-

sees and suppliers (collectively referred to as the System) has

been key to McDonald’s success. This business model enables

McDonald’s to consistently deliver locally-relevant restaurant

experiences to customers and be an integral part of the commun-

ities we serve. In addition, it facilitates our ability to identify,

implement and scale innovative ideas that meet customers’

changing needs and preferences.

McDonald’s customer-focused Plan to Win—which concen-

trates on being better, not just bigger—provides a common

framework for our global business while allowing for local

adaptation. Through the execution of multiple initiatives surround-

ing the five elements of our Plan to Win—People, Products,

Place, Price and Promotion—we have enhanced the restaurant

experience for customers worldwide and grown comparable

sales and customer visits in each of the last eight years. This

Plan, combined with financial discipline, has delivered strong

results for our shareholders.

We have exceeded our long-term, constant currency financial

targets of average annual Systemwide sales growth of 3% to

5%; average annual operating income growth of 6% to 7%; and

annual returns on incremental invested capital in the high teens

every year since the Plan’s implementation in 2003, after adjust-

ing for the loss in 2007 from the Latin America developmental

license transaction. Given the size and scope of our global busi-

ness, we believe these financial targets are realistic and

sustainable over time, keeping us focused on making the best

decisions for the long-term benefit of our System.

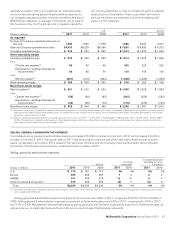

In 2011, we remained focused on customers’ needs and

accelerated efforts within the Plan to Win where the greatest

opportunity exists. The Company’s key global priorities of optimiz-

ing our menu, modernizing the customer experience, and

broadening accessibility to our Brand represent areas where we

are intensifying our efforts to drive the business further. Initiatives

supporting these priorities resonated with consumers, driving

increases in sales and customer visits despite challenging

economies and a contracting Informal Eating Out (IEO) segment

in many markets. As a result, every area of the world contributed

to 2011 global comparable sales and guest counts increasing

5.6% and 3.7%, respectively.

Specific menu pricing actions across our system reflect local

market conditions as well as other factors, notably the food away

from home and food at home inflation indices. In our Company-

operated restaurants, we manage menu board prices to ensure

value at all price points, increase profitability and mitigate

inflation, all while trying to maintain guest count momentum. In

order to accomplish these objectives, we utilize a strategic pricing

tool that balances price, product mix and promotion. Franchisees

also have access to, and many utilize, this strategic pricing tool. In

general, we believe franchisees employ a similar pricing strategy.

In 2011, we increased average price at Company-operated res-

taurants in each area of the world, although increases varied by

market and region. We look to optimize product mix by utilizing a

menu with entry-point value, core, premium and fourth-tier offer-

ings. We also introduce new products that meet customer needs,

which can expand average check and increase guest counts.

In the U.S., we grew sales, guest counts and market share

with comparable sales up for the ninth consecutive year, rising

4.8% in 2011, while comparable guest counts rose 3.3%. These

results were achieved despite a slight decline in the IEO seg-

ment. We remained focused on maximizing our core business

while providing customers with affordable products and value

throughout our menu including options available on the Dollar

Menu at breakfast and the rest of the day. We highlighted core

menu items like Chicken McNuggets that featured new sauces,

breakfast products including our new Fruit & Maple Oatmeal,

additions to the McCafé beverage line and limited-time offerings

such as the McRib sandwich. The national launch of the McCafé

Frozen Strawberry Lemonade and Mango Pineapple real-fruit

smoothie provided meaningful extensions to the McCafé bever-

age line. Convenient locations also continued to provide a

competitive advantage with extended hours and efficient drive-

thru service. Modernizing the customer experience remained a

focus with the expansion of our major remodeling program to

enhance the appearance and functionality of our restaurants and

make our restaurants more relevant to our customers’ daily lives.

Over 900 existing restaurants were remodeled during 2011 with

the majority adding drive-thru capacity to capture additional guest

counts. We also completed our two-year, Systemwide roll-out of a

new point-of-sale system. This allows us to continue expanding

our menu offerings while making it easier for our crew to fulfill

every order accurately.

In Europe, comparable sales rose 5.9%, marking the eighth

consecutive year of comparable sales increases, and comparable

guest counts rose 3.4%. Major contributors were the U.K., France,

Russia and Germany. Initiatives that helped drive our business

included leveraging our tiered menu featuring everyday affordable

prices, menu variety including new and limited-time offerings, and

reimaging over 900 restaurants. We continue to expand our cof-

fee business and have over 1,500 McCafé locations, which in

Europe are generally separate areas inside the restaurants that

serve specialty coffees, indulgent desserts and snacks. We com-

pleted the rollout of the new drive-thru customer order display

system in over 4,500 restaurants. In addition, we increased our

accessibility and convenience with extended operating hours. We

offered new premium menu items such as the 1955 burger and

expanded McWraps across several European markets. In many

markets, we have continued to offer a fourth-tier platform—such

as Little Tasters in the U.K.—a range of tasty and appealing items

in smaller portion sizes. Finally, we continued building customer

trust in our brand through communications that emphasized the

quality and origin of McDonald’s food and our commitment to

sustainable business practices.

In APMEA, our momentum continued with nearly every coun-

try delivering positive comparable sales, led by China and

Australia. Comparable sales rose 4.7% and comparable guest

counts rose 4.3% with performance driven by strategies empha-

sizing value, breakfast, convenience, core menu extensions,

desserts and promotional food events. Australia launched a Value

Lunch program that features meals at discounted price points for

certain hours while China and Japan concentrated on afford-

ability by continuing their Value Lunch platforms. New menu

items such as real-fruit smoothies and frappés in Australia and

the extension of the Value Breakfast program in China were

popular with customers. Japan executed another successful U.S.

themed burger promotion and celebrated its 40th anniversary by

offering popular core menu items at reduced prices. Desserts

10 McDonald’s Corporation Annual Report 2011