McDonalds 2011 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2011 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

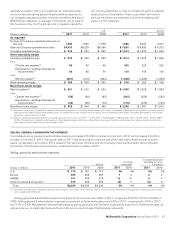

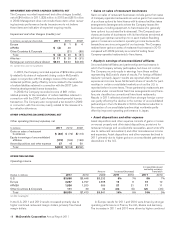

higher occupancy costs. Europe’s franchised margin percent

decreased in 2010 as positive comparable sales were more than

offset by higher occupancy expenses, the cost of strategic brand

and sales building initiatives and the refranchising strategy.

In APMEA, the franchised margin percent increase in 2011

was primarily due to a contractual escalation in the royalty rate

for Japan in addition to positive comparable sales in most mar-

kets, partly offset by a negative impact from the strengthening of

the Australian dollar. The 2010 decrease was primarily driven by

a negative impact from the strengthening of the Australian dollar.

The franchised margin percent in APMEA and Other Coun-

tries & Corporate is higher relative to the U.S. and Europe due to

a larger proportion of developmental licensed and/or affiliated

restaurants where the Company receives royalty income with no

corresponding occupancy costs.

• Company-operated margins

Company-operated margin dollars represent sales by Company-

operated restaurants less the operating costs of these

restaurants. Company-operated margin dollars increased $282

million or 9% (5% in constant currencies) in 2011 and increased

$366 million or 13% (12% in constant currencies) in 2010. The

constant currency growth in Company-operated margin dollars in

2011 was driven by positive comparable sales partially offset by

higher costs, primarily commodity costs, in all segments. Positive

comparable sales and lower commodity costs were the primary

drivers of the constant currency growth in Company-operated

margin dollars in 2010.

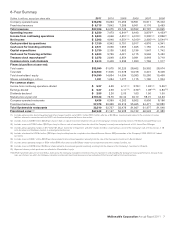

Company-operated margins

In millions 2011 2010 2009

U.S. $ 914 $ 902 $ 832

Europe 1,514 1,373 1,240

APMEA 876 764 624

Other Countries & Corporate 151 134 111

Total $3,455 $3,173 $2,807

Percent of sales

U.S. 20.6% 21.3% 19.4%

Europe 19.3 19.8 18.4

APMEA 17.3 17.8 16.8

Other Countries & Corporate 16.0 17.2 15.2

Total 18.9% 19.6% 18.2%

In the U.S., the Company-operated margin percent decreased

in 2011 due to higher commodity and occupancy costs, partially

offset by positive comparable sales. The margin percent

increased in 2010 due to lower commodity costs and positive

comparable sales, partly offset by higher labor costs. Refranchis-

ing also had a positive impact on the margin percent in 2010.

Europe’s Company-operated margin percent decreased in

2011 primarily due to higher commodity, labor, and occupancy

costs, partially offset by positive comparable sales. The margin

percent increased in 2010 primarily due to positive comparable

sales and lower commodity costs, partly offset by higher labor costs.

In APMEA, the Company-operated margin percent in 2011

reflected positive comparable sales, offset by higher commodity,

labor and occupancy costs. Acceleration of new restaurant open-

ings in China negatively impacted the margin percent. Similar to

other markets, new restaurants in China initially open with lower

margins that grow significantly over time. The APMEA margin

percent increased in 2010 due to positive comparable sales and

lower commodity costs, partly offset by higher occupancy & other

costs and increased labor costs.

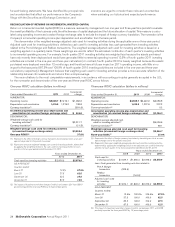

Supplemental information regarding Company-

operated restaurants

We continually review our restaurant ownership mix with a goal of

improving local relevance, profits and returns. In most cases,

franchising is the best way to achieve these goals, but as pre-

viously stated, Company-operated restaurants are also important

to our success.

We report results for Company-operated restaurants based

on their sales, less costs directly incurred by that business includ-

ing occupancy costs. We report the results for franchised

restaurants based on franchised revenues, less associated occu-

pancy costs. For this reason and because we manage our

business based on geographic segments and not on the basis of

our ownership structure, we do not specifically allocate selling,

general & administrative expenses and other operating (income)

expenses to Company-operated or franchised restaurants. Other

operating items that relate to the Company-operated restaurants

generally include gains/losses on sales of restaurant businesses

and write-offs of equipment and leasehold improvements.

We believe the following information about Company-

operated restaurants in our most significant segments provides

an additional perspective on this business. Management respon-

sible for our Company-operated restaurants in these markets

analyzes the Company-operated business on this basis to assess

its performance. Management of the Company also considers

this information when evaluating restaurant ownership mix, sub-

ject to other relevant considerations.

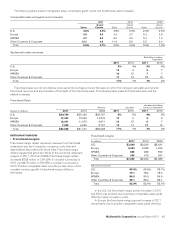

The following table seeks to illustrate the two components of

our Company-operated margins. The first of these relates

exclusively to restaurant operations, which we refer to as “Store

operating margin.” The second relates to the value of our brand

and the real estate interest we retain for which we charge rent

and royalties. We refer to this component as “Brand/real estate

margin.” Both Company-operated and conventional franchised

restaurants are charged rent and royalties, although rent and

royalties for Company-operated restaurants are eliminated in

consolidation. Rent and royalties for both restaurant ownership

types are based on a percentage of sales, and the actual rent

percentage varies depending on the level of McDonald’s invest-

ment in the restaurant. Royalty rates may also vary by market.

As shown in the following table, in disaggregating the compo-

nents of our Company-operated margins, certain costs

with respect to Company-operated restaurants are reflected in

Brand/real estate margin. Those costs consist of rent payable by

McDonald’s to third parties on leased sites and depreciation for

buildings and leasehold improvements and constitute a portion of

occupancy & other operating expenses recorded in the Con-

solidated statement of income. Store operating margins reflect

rent and royalty expenses, and those amounts are accounted for

as income in calculating Brand/real estate margin.

While we believe that the following information provides a

perspective in evaluating our Company-operated business, it is

not intended as a measure of our operating performance or as an

alternative to operating income or restaurant margins as reported

by the Company in accordance with accounting principles

16 McDonald’s Corporation Annual Report 2011