McDonalds 2013 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2013 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

McDonald’s Corporation 2013 Annual Report | 11

enables McDonald's to consistently deliver locally-relevant

restaurant experiences to customers and be an integral part of the

communities we serve.

McDonald's customer-focused Plan to Win ("Plan") provides a

common framework that aligns our global business and allows for

local adaptation. We continue to focus on our three global growth

priorities of optimizing our menu, modernizing the customer

experience, and broadening accessibility to Brand McDonald's

within the framework of our Plan. Our initiatives support these

priorities, and are executed with a focus on the Plan's five pillars -

People, Products, Place, Price and Promotion - to enhance our

customers' experience and build shareholder value over the long

term. We believe these priorities align with our customers' evolving

needs, and - combined with our competitive advantages of

convenience, menu variety, geographic diversification and System

alignment - will drive long-term sustainable growth.

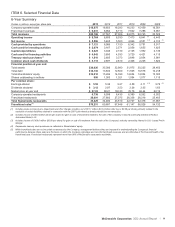

To measure our performance as we strive to build the

business, we have the following long-term, average annual

constant currency financial targets:

Systemwide sales growth of 3% to 5%;

Operating income growth of 6% to 7%;

ROIIC in the high teens.

In 2013, Systemwide sales growth was 1% (3% in constant

currencies), operating income growth was 2% (3% in constant

currencies), one-year ROIIC was 11.4% and three-year ROIIC was

20.2% (see reconciliation on page 23). Our operating income

growth and returns fell below our long-term financial targets,

reflecting the impact of soft comparable sales performance. In our

heavily franchised business model, growing comparable sales is

important to increasing operating income and returns.

In 2013, our comparable sales increased 0.2%, reflecting

higher average check and negative comparable guest counts of

1.9%. Challenging conditions, including a flat or contracting

informal eating out (“IEO”) segment in most major markets,

heightened competitive activity and consumer price sensitivity,

continued to pressure performance. Furthermore, McDonald’s

customer-facing initiatives did not generate the comparable sales

lift or customer visits necessary to overcome these headwinds.

In 2014, we do not expect significant changes in market

dynamics given modest growth projections for the IEO segment.

However, we continue to believe that our targets remain

achievable over the long term.

The following is a summary of our 2013 sales performance

and our initiatives within the three global growth priorities by major

segment.

U.S.

In the U.S., comparable sales declined 0.2% and comparable

guest counts declined 1.6%. Guest visits were down as initiatives

did not resonate as strongly as expected with customers amid a

sluggish IEO segment and heightened competitive activity.

The U.S. introduced a number of significant new products

(such as Premium McWraps, Egg White Delight McMuffins and an

extended line-up of Quarter Pounder Burgers) and featured new

limited-time food and beverage options to enhance the relevance

of its product offerings.

Modernizing the customer experience continued through our

reimaging program. During 2013, we completed about 700

restaurant reimages, of which the majority added drive-thru

capacity. Currently, 45% of our restaurant interiors and exteriors

reflect our contemporary restaurant design.

We broadened accessibility by opening 225 new restaurants,

extending hours in more restaurants, and improving the efficiency

of our drive-thru service with side-by-side or tandem ordering, and

hand-held order taking. More than half of our restaurants now use

one of these multiple order points to maximize drive-thru capacity.

In addition, the U.S. evolved its value proposition with the recent

introduction of Dollar Menu & More, which is intended to offer

value and variety to our customers at various price points.

Europe

In Europe, comparable sales were flat, while comparable guest

counts declined 1.5%, as persistently low consumer confidence

continued to negatively affect the IEO segment. Comparable sales

results reflected positive performance in the U.K. and Russia,

which were mostly offset by weak performance in Germany, where

we are working on rebuilding brand relevance to address the

current negative guest count trend.

In 2013, we remained focused on growing the business by

emphasizing value menu enhancements, premium menu

additions, limited-time offers and expansion of the breakfast

daypart. We also successfully launched blended ice beverages in

the U.K., which positively contributed to results.

In order to continue providing a relevant, contemporary

customer experience, Europe completed about 470 restaurant

reimages during the year. By the end of 2013, nearly 100% of

restaurant interiors and 80% of exteriors were modernized.

We increased our accessibility and convenience by opening

312 new restaurants, extending operating hours and optimizing

our drive-thrus. We enhanced our value offerings in certain

markets with multiple pricing tiers across our menu to appeal to a

broad range of customers. For example, in France we launched

the Casse-Croûte, a two-item meal for 4.50 Euro, which positively

contributed to recent results in that market.

APMEA

In APMEA, comparable sales declined 1.9% and comparable

guest counts declined 3.8%. Our three largest markets

experienced negative comparable sales, with Japan having the

most significant impact. Though the challenges differ across the

segment, overall performance was pressured amid slower

economic growth, a highly competitive environment focused

primarily on value, and issues such as Avian influenza in a few

markets. In addition, softer than expected performance of new

products and promotions did not overcome negative guest count

trends.

Throughout the segment, we focused on accelerating growth

across all dayparts, with particular emphasis on dinner and the

expansion of breakfast. APMEA held a National Breakfast Day,

during which five thousand restaurants gave away five million Egg

McMuffins to promote breakfast in the segment. We were also

committed to enhancing local relevance with consumers, by

balancing our global core menu with locally-relevant food and

beverage choices, which included new flavor profiles designed to

match local tastes.

We continued to make progress in our reimaging program,

completing about 240 restaurant reimages during the year. By the

end of 2013, over 65% of restaurant interiors and over 55% of

exteriors were modernized.

We opened 731 new restaurants, including 275 in China. We

deployed our convenience initiatives to more restaurants,

including dessert kiosks, delivery service, drive-thrus and

extended hours. In addition, we continued to evolve our everyday

value platform by including more affordable menu options and

promotional offers across dayparts and price points.