McDonalds 2013 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2013 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

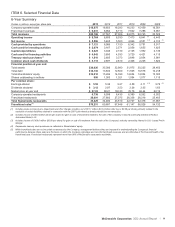

McDonald’s Corporation 2013 Annual Report | 13

APMEA

In 2014, APMEA’s growth opportunities include menu variety,

convenience, value evolution and restaurant expansion. We will

balance core and limited-time offers and execute a series of

exciting food events. APMEA will shift existing value platforms

toward more compelling offers that resonate with customers and

generate incremental visits, including “mid-tier” options to fill the

gap between entry-level options and Extra Value Meals. Our

efforts around reimaging will continue as we expect to modernize

approximately 400 existing restaurants. Our plan is to open

around 800 new restaurants, with about 300 expected in China. In

addition, we will evolve our franchising strategy to include more

conventional franchisees and developmental licensees, enabling

an increased pace of development and enhanced profitability.

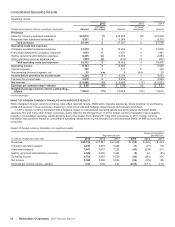

Consolidated

In making capital allocation decisions, our goal is to make

investments that elevate the McDonald's experience and drive

sustainable long-term growth in sales and market share. We focus

on markets that generate strong returns or have opportunities for

long-term growth. We remain committed to returning all of our free

cash flow (cash from operations less capital expenditures) to

shareholders over the long-term via dividends and share

repurchases.

McDonald's does not provide specific guidance on diluted

earnings per share. The following information is provided to assist

in forecasting the Company's future results:

Changes in Systemwide sales are driven by comparable

sales and net restaurant unit expansion. The Company

expects net restaurant additions to add approximately 2.5

percentage points to 2014 Systemwide sales growth (in

constant currencies), most of which will be due to the 949 net

restaurants (1,098 net traditional openings less 149 net

satellite closings) added in 2013.

The Company does not generally provide specific guidance

on changes in comparable sales. However, as a perspective,

assuming no change in cost structure, a 1 percentage point

change in comparable sales for either the U.S. or Europe

would change annual diluted earnings per share by about 4

cents.

With about 75% of McDonald's grocery bill comprised of 10

different commodities, a basket of goods approach is the

most comprehensive way to look at the Company's

commodity costs. For the full year 2014, the total basket of

goods cost is expected to increase 1.0-2.0% in the U.S. and

Europe.

The Company expects full-year 2014 selling, general and

administrative expenses to increase approximately 8% in

constant currencies, with fluctuations expected between the

quarters. The increase is primarily due to the impact of

below target 2013 incentive-based compensation, expenses

associated with our Worldwide Owner/Operator Convention

and sponsorship of the Winter Olympic games, and costs

related to other initiatives.

Based on current interest and foreign currency exchange

rates, the Company expects interest expense for the full year

2014 to increase approximately 5-7% compared with 2013.

A significant part of the Company's operating income is

generated outside the U.S., and about 40% of its total debt is

denominated in foreign currencies. Accordingly, earnings are

affected by changes in foreign currency exchange rates,

particularly the Euro, British Pound, Australian Dollar and

Canadian Dollar. Collectively, these currencies represent

approximately 65% of the Company's operating income

outside the U.S. If all four of these currencies moved by 10%

in the same direction, the Company's annual diluted earnings

per share would change by about 25 cents.

The Company expects the effective income tax rate for the

full-year 2014 to be 31% to 33%. Some volatility may be

experienced between the quarters resulting in a quarterly tax

rate that is outside the annual range.

The Company expects capital expenditures for 2014 to be

between $2.9 - $3.0 billion. Over half of this amount will be

used to open new restaurants. The Company expects to

open about 1,500 - 1,600 restaurants including about 500

restaurants in affiliated and developmental licensee markets,

such as Japan and Latin America, where the Company does

not fund any capital expenditures. The Company expects net

additions of between 1,000 - 1,100 restaurants. The

remaining capital will be used to reinvest in existing

locations, in part through reimaging. Over 1,000 restaurants

worldwide are expected to be reimaged, including locations

in affiliated and developmental licensee markets that require

no capital investment from the Company.

The Company expects to return approximately $5 billion to

shareholders through dividends and share repurchases in

2014.