McDonalds 2013 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2013 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

22 | McDonald’s Corporation 2013 Annual Report

and will continue to make, substantial investments to support the

ongoing development and growth of our international operations.

Accordingly, no U.S. federal or state income taxes have been

provided on these undistributed foreign earnings. The Company's

cash and equivalents held by our foreign subsidiaries totaled

approximately $2.0 billion as of December 31, 2013. We do not

intend, nor do we foresee a need, to repatriate these funds.

Consistent with prior years, we expect existing domestic cash

and equivalents, domestic cash flows from operations, annual

repatriation of a portion of the current period's foreign earnings,

and the issuance of domestic debt to continue to be sufficient to

fund our domestic operating, investing, and financing activities.

We also continue to expect existing foreign cash and equivalents

and foreign cash flows from operations to be sufficient to fund our

foreign operating, investing, and financing activities.

In the future, should we require more capital to fund activities

in the U.S. than is generated by our domestic operations and is

available through the issuance of domestic debt, we could elect to

repatriate a greater portion of future periods' earnings from foreign

jurisdictions. This could also result in a higher effective tax rate in

the future.

While the likelihood is remote, to the extent foreign cash is

available, the Company could also elect to repatriate earnings

from foreign jurisdictions that have previously been considered to

be indefinitely reinvested. Upon distribution of those earnings in

the form of dividends or otherwise, the Company may be subject

to additional U.S. income taxes (net of an adjustment for foreign

tax credits), which could result in a use of cash. This could also

result in a higher effective tax rate in the period in which such a

determination is made to repatriate prior period foreign earnings.

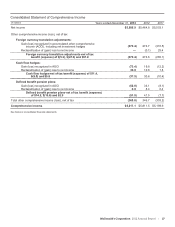

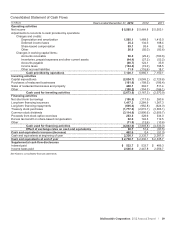

Refer to the Income Taxes note to the consolidated financial

statements for further information related to our income taxes and

the undistributed earnings of the Company's foreign subsidiaries.

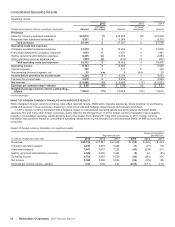

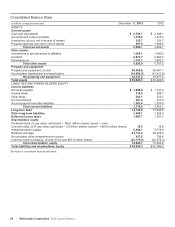

CONTRACTUAL OBLIGATIONS AND COMMITMENTS

The Company has long-term contractual obligations primarily in

the form of lease obligations (related to both Company-operated

and franchised restaurants) and debt obligations. In addition, the

Company has long-term revenue and cash flow streams that

relate to its franchise arrangements. Cash provided by operations

(including cash provided by these franchise arrangements) along

with the Company’s borrowing capacity and other sources of cash

will be used to satisfy the obligations. The following table

summarizes the Company’s contractual obligations and their

aggregate maturities as well as future minimum rent payments

due to the Company under existing franchise arrangements as of

December 31, 2013. See discussions of cash flows and financial

position and capital resources as well as the Notes to the

consolidated financial statements for further details.

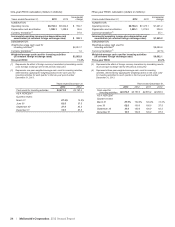

Contractual cash outflows Contractual cash inflows

In millions Operating

leases

Debt

obligations(1) Minimum rent under

franchise arrangements

2014 $ 1,440 $ 2,703

2015 1,334 $ 1,199 2,612

2016 1,218 2,095 2,507

2017 1,099 1,054 2,377

2018 990 1,004 2,260

Thereafter 7,632 8,765 18,042

Total $13,713 $14,117 $30,501

(1) The maturities reflect reclassifications of short-term obligations to long-

term obligations of $1.2 billion, as they are supported by a long-term line

of credit agreement expiring in November 2016. Debt obligations do not

include $13 million of noncash fair value hedging adjustments or $222

million of accrued interest.

In the U.S., the Company maintains certain supplemental

benefit plans that allow participants to (i) make tax-deferred

contributions and (ii) receive Company-provided allocations that

cannot be made under the qualified benefit plans because of

Internal Revenue Service ("IRS") limitations. At December 31,

2013, total liabilities for the supplemental plans were $531 million.

In addition, total liabilities for gross unrecognized tax benefits

were $513 million at December 31, 2013.

There are certain purchase commitments that are not

recognized in the consolidated financial statements and are

primarily related to construction, inventory, energy, marketing and

other service related arrangements that occur in the normal

course of business. The amounts related to these commitments

are not significant to the Company’s financial position. Such

commitments are generally shorter term in nature and will be

funded from operating cash flows.

Other Matters

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Management’s discussion and analysis of financial condition and

results of operations is based upon the Company’s consolidated

financial statements, which have been prepared in accordance

with accounting principles generally accepted in the U.S. The

preparation of these financial statements requires the Company to

make estimates and judgments that affect the reported amounts of

assets, liabilities, revenues and expenses as well as related

disclosures. On an ongoing basis, the Company evaluates its

estimates and judgments based on historical experience and

various other factors that are believed to be reasonable under the

circumstances. Actual results may differ from these estimates

under various assumptions or conditions.

The Company reviews its financial reporting and disclosure

practices and accounting policies quarterly to ensure that they

provide accurate and transparent information relative to the

current economic and business environment. The Company

believes that of its significant accounting policies, the following

involve a higher degree of judgment and/or complexity:

Property and equipment

Property and equipment are depreciated or amortized on a

straight-line basis over their useful lives based on management’s

estimates of the period over which the assets will generate

revenue (not to exceed lease term plus options for leased

property). The useful lives are estimated based on historical

experience with similar assets, taking into account anticipated

technological or other changes. The Company periodically reviews

these lives relative to physical factors, economic factors and

industry trends. If there are changes in the planned use of

property and equipment, or if technological changes occur more

rapidly than anticipated, the useful lives assigned to these assets

may need to be shortened, resulting in the accelerated recognition

of depreciation and amortization expense or write-offs in future

periods.

Share-based compensation

The Company has a share-based compensation plan which

authorizes the granting of various equity-based incentives

including stock options and restricted stock units ("RSUs") to

employees and nonemployee directors. The expense for these

equity-based incentives is based on their fair value at date of grant

and generally amortized over their vesting period.

The fair value of each stock option granted is estimated on

the date of grant using a closed-form pricing model. The pricing

model requires assumptions, which impact the assumed fair value,

including the expected life of the stock option, the risk-free interest

rate, expected volatility of the Company’s stock over the expected