McDonalds 2013 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2013 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

32 | McDonald’s Corporation 2013 Annual Report

GOODWILL

Goodwill represents the excess of cost over the net tangible

assets and identifiable intangible assets of acquired restaurant

businesses. The Company's goodwill primarily results from

purchases of McDonald's restaurants from franchisees and

ownership increases in subsidiaries or affiliates, and it is generally

assigned to the reporting unit expected to benefit from the

synergies of the combination. If a Company-operated restaurant is

sold within 24 months of acquisition, the goodwill associated with

the acquisition is written off in its entirety. If a restaurant is sold

beyond 24 months from the acquisition, the amount of goodwill

written off is based on the relative fair value of the business sold

compared to the reporting unit (defined as each individual

country).

The Company conducts goodwill impairment testing in the

fourth quarter of each year or whenever an indicator of impairment

exists. If an indicator of impairment exists (e.g., estimated

earnings multiple value of a reporting unit is less than its carrying

value), the goodwill impairment test compares the fair value of a

reporting unit, generally based on discounted future cash flows,

with its carrying amount including goodwill. If the carrying amount

of a reporting unit exceeds its fair value, an impairment loss is

measured as the difference between the implied fair value of the

reporting unit's goodwill and the carrying amount of goodwill.

Historically, goodwill impairment has not significantly impacted the

consolidated financial statements.

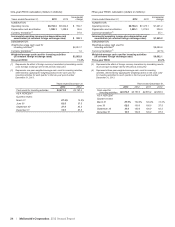

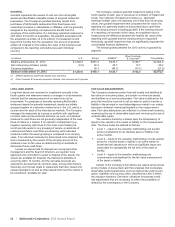

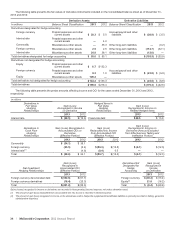

The following table presents the 2013 activity in goodwill by

segment:

In millions U.S. Europe APMEA(1) Other Countries

& Corporate(2) Consolidated

Balance at December 31, 2012 $1,294.2 $ 881.4 $ 438.7 $ 189.7 $2,804.0

Net restaurant purchases (sales) (0.6) 50.4 30.7 15.7 96.2

Currency translation 26.3 (40.7) (13.1) (27.5)

Balance at December 31, 2013 $1,293.6 $ 958.1 $ 428.7 $ 192.3 $2,872.7

(1) APMEA represents Asia/Pacific, Middle East and Africa.

(2) Other Countries & Corporate represents Canada, Latin America and Corporate.

LONG-LIVED ASSETS

Long-lived assets are reviewed for impairment annually in the

fourth quarter and whenever events or changes in circumstances

indicate that the carrying amount of an asset may not be

recoverable. For purposes of annually reviewing McDonald’s

restaurant assets for potential impairment, assets are initially

grouped together at a television market level in the U.S. and at a

country level for each of the international markets. The Company

manages its restaurants as a group or portfolio with significant

common costs and promotional activities; as such, an individual

restaurant’s cash flows are not generally independent of the cash

flows of others in a market. If an indicator of impairment (e.g.,

negative operating cash flows for the most recent trailing 24-

month period) exists for any grouping of assets, an estimate of

undiscounted future cash flows produced by each individual

restaurant within the asset grouping is compared to its carrying

value. If an individual restaurant is determined to be impaired, the

loss is measured by the excess of the carrying amount of the

restaurant over its fair value as determined by an estimate of

discounted future cash flows.

Losses on assets held for disposal are recognized when

management and the Board of Directors, as required, have

approved and committed to a plan to dispose of the assets, the

assets are available for disposal, the disposal is probable of

occurring within 12 months, and the net sales proceeds are

expected to be less than its net book value, among other factors.

Generally, such losses relate to restaurants that have closed and

ceased operations as well as other assets that meet the criteria to

be considered “available for sale”.

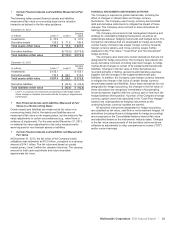

FAIR VALUE MEASUREMENTS

The Company measures certain financial assets and liabilities at

fair value on a recurring basis, and certain non-financial assets

and liabilities on a nonrecurring basis. Fair value is defined as the

price that would be received to sell an asset or paid to transfer a

liability in the principal or most advantageous market in an orderly

transaction between market participants on the measurement

date. Fair value disclosures are reflected in a three-level hierarchy,

maximizing the use of observable inputs and minimizing the use of

unobservable inputs.

The valuation hierarchy is based upon the transparency of

inputs to the valuation of an asset or liability on the measurement

date. The three levels are defined as follows:

Level 1 – inputs to the valuation methodology are quoted

prices (unadjusted) for an identical asset or liability in an

active market.

Level 2 – inputs to the valuation methodology include quoted

prices for a similar asset or liability in an active market or

model-derived valuations in which all significant inputs are

observable for substantially the full term of the asset or

liability.

Level 3 – inputs to the valuation methodology are

unobservable and significant to the fair value measurement

of the asset or liability.

Certain of the Company’s derivatives are valued using various

pricing models or discounted cash flow analyses that incorporate

observable market parameters, such as interest rate yield curves,

option volatilities and currency rates, classified as Level 2 within

the valuation hierarchy. Derivative valuations incorporate credit

risk adjustments that are necessary to reflect the probability of

default by the counterparty or the Company.