Verizon Wireless 2008 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2008 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Alltel Interest Rate Swaps

InconnectionwiththeAlltelacquisition(see“RecentDevelopments”),

Verizon Wireless acquired seven interest rate swap agreements with a

notional value of $9.5 billion that pay fixed and receive variable rates

basedonthree-monthandone-monthLIBORwithmaturitiesranging

from 2009 to 2013. Until they are terminated, the swap agreements are

guaranteed by Verizon Wireless. Upon closing of the acquisition, these

swap agreements will be recorded at fair value as of the closing date as

part of the purchase price allocation and subsequent changes in the fair

value will be recorded in earnings. Based on recent trends in the credit

markets, changes in interest rates may have a significant impact on our

earnings as long as the contracts are outstanding. We estimate that a

10-basis point change in rates can result in an approximately $30 mil-

lion impact on pretax earnings. We anticipate that these contracts will be

settled during the first half of 2009.

Foreign Currency Translation

The functional currency of our foreign operations is generally the local cur-

rency. For these foreign entities, we translate income statement amounts

at average exchange rates for the period, and we translate assets and

liabilities at end-of-period exchange rates. We record these translation

adjustments in Accumulated other comprehensive loss, a separate com-

ponent of Shareowners’ Investment, in our consolidated balance sheets.

We report exchange gains and losses on intercompany foreign currency

transactions of a long-term nature in Accumulated other comprehen-

sive loss. Other exchange gains and losses are reported in income. At

December 31, 2008, our primary translation exposure was to the British

Pound Sterling, the Euro and the Australian Dollar.

During 2008, we entered into cross currency swaps designated as cash

flow hedges to exchange the net proceeds from the December 18, 2008

Verizon Wireless and Verizon Wireless Capital LLC offering from British

Pound Sterling and Euros into U.S. dollars, to fix our future interest and

principal payments in U.S. dollars as well as mitigate the impact of for-

eign currency transaction gains or losses. We record these contracts at

fair value and any gains or losses on these contracts will, over time, offset

the gains or losses on the underlying debt obligations.

During 2007, we entered into foreign currency forward contracts to

hedge a portion of our net investment in Vodafone Omnitel. Changes

in fair value of these contracts due to Euro exchange rate fluctuations

are recognized in Accumulated other comprehensive loss and partially

offset the impact of foreign currency changes on the value of our net

investment. During 2008, our positions in these foreign currency forward

contracts were settled. As of December 31, 2008, Accumulated other

comprehensive loss includes unrecognized losses of approximately $166

million ($108 million after-tax) related to these hedge contracts, which

along with the unrealized foreign currency translation balance on the

investment hedged, remain in Accumulated other comprehensive loss

until the investment is sold.

Guarantees

In connection with the execution of agreements for the sale of businesses

and investments, Verizon ordinarily provides representations and warran-

ties to the purchasers pertaining to a variety of nonfinancial matters, such

as ownership of the securities being sold, as well as financial losses.

As of December 31, 2008, letters of credit totaling approximately $200

million were executed in the normal course of business, which support

several financing arrangements and payment obligations to third parties.

MARKET RISK

We are exposed to various types of market risk in the normal course of

business, including the impact of interest rate changes, foreign currency

exchange rate fluctuations, changes in equity investment and commodity

prices and changes in corporate tax rates. We employ risk management

strategies which may include the use of a variety of derivatives, including

cross currency swaps, foreign currency forwards and collars, equity

options, interest rate and commodity swap agreements and interest rate

locks. We do not hold derivatives for trading purposes.

It is our general policy to enter into interest rate, foreign currency and

other derivative transactions only to the extent necessary to achieve our

desired objectives in limiting our exposure to the various market risks. Our

objectives include maintaining a mix of fixed and variable rate debt to

lower borrowing costs within reasonable risk parameters and to protect

against earnings and cash flow volatility resulting from changes in market

conditions. We do not hedge our market risk exposure in a manner that

would completely eliminate the effect of changes in interest rates and

foreign exchange rates on our earnings. We do not expect that our net

income, liquidity and cash flows will be materially affected by these risk

management strategies.

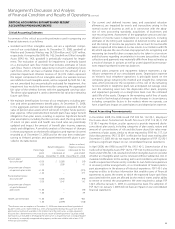

Interest Rate Risk

The table that follows summarizes the fair values of our long-term debt

and interest rate and cross currency swap derivatives as of December 31,

2008 and 2007. The table also provides a sensitivity analysis of the esti-

mated fair values of these financial instruments assuming 100-basis-point

upward and downward shifts in the yield curve. Our sensitivity analysis

does not include the fair values of our commercial paper and bank loans,

if any, because they are not significantly affected by changes in market

interest rates.

(dollars in millions)

At December 31, 2008 Fair Value

Fair Value

assuming

+100 basis

point shift

Fair Value

assuming

–100 basis

point shift

Long-term debt and related

derivatives $ 51,258 $ 48,465 $ 54,444

At December 31, 2007

Long-term debt and related

derivatives $ 31,930 $ 30,154 $ 33,957

28

Management’s Discussion and Analysis

ofFinancialConditionandResultsofOperations continued