Verizon Wireless 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

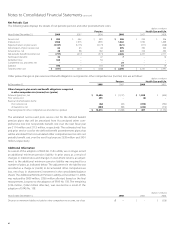

Notes to Consolidated Financial Statements continued

57

Guarantees

We guarantee the debt obligations of GTE Corporation (but not the

debt of its subsidiary or affiliate companies) that were issued and out-

standing prior to July 1, 2003. As of December 31, 2008, $2,200 million

principal amount of these obligations remained outstanding. Verizon

Communications Inc. and NYNEX Corporation are the joint and several

co-obligors of the 20-Year 9.55% Debentures due 2010 previously issued

by NYNEX on March 26, 1990. As of December 31, 2008, $47 million prin-

cipal amount of this obligation remained outstanding. NYNEX and GTE

no longer issue public debt or file SEC reports.

Debt Covenants

We and our consolidated subsidiaries are in compliance with all of our

debt covenants.

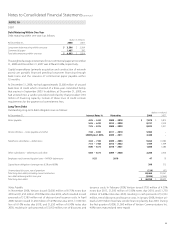

Maturities of Long-Term Debt

Maturities of long-term debt outstanding at December 31, 2008 are as

follows:

Years (dollars in million)

2009 $ 3,506

2010 5,018

2011 5,647

2012 4,306

2013 5,638

Thereafter 26,350

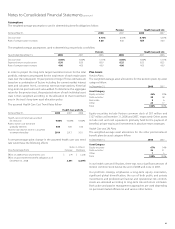

NOTE 11

FINANCIAL INSTRUMENTS

Derivatives

The ongoing effect of SFAS No. 133 and related amendments and inter-

pretations on our consolidated financial statements will be determined

each period by several factors, including the specific hedging instru-

ments in place and their relationships to hedged items, as well as market

conditions at the end of each period.

Interest Rate Risk Management

We have entered into domestic interest rate swaps to achieve a targeted

mix of fixed and variable rate debt, where we principally receive fixed

rates and pay variable rates based on LIBOR. These swaps are designated

as fair value hedges and hedge against changes in the fair value of our

debt portfolio. We record the interest rate swaps at fair value in our bal-

ance sheet as assets and liabilities and adjust debt for the change in

its fair value due to changes in interest rates. During 2008, we entered

into domestic interest rate swaps, designated as fair value hedges, with a

notional principal value of approximately $2 billion. The fair value of our

entire portfolio of interest rate swaps at December 31, 2008 included in

Other assets and Long-term debt was $415 million.

Foreign Exchange Risk Management

During 2008, we entered into cross currency swaps designated as cash

flow hedges to exchange the net proceeds from the December 18, 2008

Verizon Wireless and Verizon Wireless Capital LLC offering (see Note 10)

from British Pound Sterling and Euros into U.S. dollars, to fix our future

interest and principal payments in U.S. dollars as well as mitigate the

impact of foreign currency transaction gains or losses. We record these

contracts at fair value and any gains or losses on the contract will, over

time, offset the gains or losses on the underlying debt obligations.

Net Investment Hedges

During 2007, we entered into foreign currency forward contracts to

hedge a portion of our net investment in Vodafone Omnitel. Changes

in fair value of these contracts due to Euro exchange rate fluctuations

are recognized in Accumulated other comprehensive loss and partially

offset the impact of foreign currency changes on the value of our net

investment. During 2008, our positions in these foreign currency forward

contracts were settled. As of December 31, 2008, Accumulated other

comprehensive loss includes unrecognized losses of approximately

$166 million ($108 million after-tax) related to these hedge contracts,

which along with the unrealized foreign currency translation balance on

the investment hedged, remain in Accumulated other comprehensive

loss until the investment is sold.

Concentrations of Credit Risk

Financial instruments that subject us to concentrations of credit risk con-

sist primarily of temporary cash investments, short-term and long-term

investments, trade receivables, certain notes receivable, including lease

receivables, and derivative contracts. Our policy is to deposit our tem-

porary cash investments with major financial institutions. Counterparties

to our derivative contracts are also major financial institutions. The finan-

cial institutions have all been accorded high ratings by primary rating

agencies. We limit the dollar amount of contracts entered into with any

one financial institution and monitor our counterparties’ credit ratings.

We generally do not give or receive collateral on swap agreements due

to our credit rating and those of our counterparties. While we may be

exposed to credit losses due to the nonperformance of our counterpar-