Verizon Wireless 2008 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2008 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

• Our current and deferred income taxes, and associated valuation

allowances, are impacted by events and transactions arising in the

normal course of business as well as in connection with the adop-

tion of new accounting standards, acquisitions of businesses and

non-recurring items. Assessment of the appropriate amount and clas-

sification of income taxes is dependent on several factors, including

estimates of the timing and realization of deferred income tax assets

and the timing of income tax payments. We account for tax benefits

taken or expected to be taken in our tax returns in accordance with FIN

48, which requires the use of a two-step approach for recognizing and

measuring tax benefits taken or expected to be taken in a tax return

and disclosures regarding uncertainties in income tax positions. Actual

collections and payments may materially differ from these estimates as

a result of changes in tax laws as well as unanticipated future transac-

tions impacting related income tax balances.

• Verizon’s plant, property and equipment balance represents a sig-

nificant component of our consolidated assets. Depreciation expense

on Verizon’s local telephone operations is principally based on the

composite group remaining life method and straight-line composite

rates, which provides for the recognition of the cost of the remaining

net investment in telephone plant, less anticipated net salvage value,

over the remaining asset lives. We depreciate other plant, property

and equipment generally on a straight-line basis over the estimated

useful life of the assets. Changes in the remaining useful lives of assets

as a result of technological change or other changes in circumstances,

including competitive factors in the markets where we operate, can

have a significant impact on asset balances and depreciation expense.

Recent Accounting Pronouncements

InDecember2008,theFASBissued FSP FASNo.132(R)-1,Employers’

Disclosures about Postretirement Benefit Plan Assets(FSP132(R)-1).FSP

132(R)-1requiresVerizon,asplansponsor,toprovideimproveddisclo-

sures about plan assets, including categories of plan assets, nature and

amount of concentrations of risk and disclosure about fair value mea-

surements of plan assets, similar to those required by SFAS No. 157, Fair

Value Measurements.FAS132(R)-1iseffectiveforfiscalyearsendingafter

December15,2009.WedonotexpectthattheadoptionofFSP132(R)-1

will have a significant impact on our consolidated financial statements.

In April 2008, the FASB issued FSP No. FAS 142-3, Determination of the

Useful Life of Intangible Assets (FSP 142-3). FSP 142-3 removes the require-

ment under SFAS No. 142, Goodwill and Other Intangible Assets to consider

whether an intangible asset can be renewed without substantial cost or

material modifications to the existing terms and conditions, and replaces

it with a requirement that an entity consider its own historical experience

in renewing similar arrangements, or a consideration of market partici-

pant assumptions in the absence of historical experience. FSP 142-3 also

requires entities to disclose information that enables users of financial

statements to assess the extent to which the expected future cash flows

associated with the asset are affected by the entity’s intent and/or ability

to renew or extend the arrangement. We were required to adopt FSP

142-3 effective January 1, 2009 on a prospective basis. The adoption of

FSP 142-3 on January 1, 2009 did not have an impact on our consolidated

financial statements.

CRITICAL ACCOUNTING ESTIMATES AND RECENT

ACCOUNTING PRONOUNCEMENTS

Critical Accounting Estimates

A summary of the critical accounting estimates used in preparing our

financial statements is as follows:

• Goodwill and Other intangible assets, net are a significant compo-

nent of our consolidated assets. At December 31, 2008, goodwill at

Wireline and Domestic Wireless was $4,738 million and $1,297 million,

respectively. As required by SFAS No. 142, Goodwill and Other Intangible

Assets (SFAS No. 142), goodwill is periodically evaluated for impair-

ment. The evaluation of goodwill for impairment is primarily based

on a discounted cash flow model that includes estimates of future

cash flows. There is inherent subjectivity involved in estimating future

cash flows, which can have a material impact on the amount of any

potential impairment. Wireless licenses of $61,974 million represent

the largest component of our intangible assets. Our wireless licenses

are indefinite-lived intangible assets, and as required by SFAS No. 142,

are not amortized but are periodically evaluated for impairment. Any

impairment loss would be determined by comparing the aggregated

fair value of the wireless licenses with the aggregated carrying value.

The direct value approach is used to determine fair value by estimating

future cash flows.

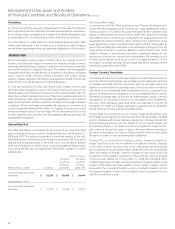

• We maintain benefit plans for most of our employees, including pen-

sion and other postretirement benefit plans. At December 31, 2008,

in the aggregate, pension plan benefit obligations exceeded the fair

value of pension plan assets which will result in higher future pension

plan expense. Other postretirement benefit plans have larger benefit

obligations than plan assets, resulting in expense. Significant benefit

plan assumptions, including the discount rate used, the long-term rate

of return on plan assets and health care trend rates are periodically

updated and impact the amount of benefit plan income, expense,

assets and obligations. A sensitivity analysis of the impact of changes

in these assumptions on the benefit obligations and expense (income)

recorded as of December 31, 2008 and for the year then ended per-

taining to Verizon’s pension and postretirement benefit plans is pro-

vided in the table below.

(dollars in millions)

Percentage

point

change

Benet obligation

increase

(decrease) at

December 31, 2008

Expense increase

(decrease) for the

year ended

December 31, 2008

Pension plans

discount rate* + 0.50 $ (1,281) $ (29)

- 0.50 1,399 41

Long-term rate of return

on pension plan assets + 1.00 – (375)

- 1.00 – 375

Postretirement plans

discount rate* + 0.50 (1,401) (99)

- 0.50 1,547 110

Long-term rate of return

on postretirement

plan assets + 1.00 – (39)

- 1.00 – 39

Health care trend rates + 1.00 2,891 460

- 1.00 (2,399) (318)

*The discount rate assumptions at December 31, 2008 were determined from hypothetical

double A yield curves represented by a series of annualized individual discount rates devel-

oped using actual bonds available in the market. From the yield curves a single equivalent

discount rate is determined at which the future stream of benefit payments could be settled.

Each bond issue included in developing the yield curves is required to have a rating of double

A or better by a nationally recognized rating agency and be non-callable with at least $150

million par outstanding.

29

Management’s Discussion and Analysis

ofFinancialConditionandResultsofOperations continued