Lowe's 2010 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2010 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

|

|

42 LOWE’S 2010 ANNUAL REPORT

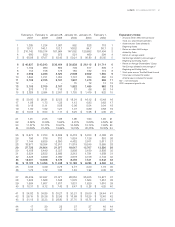

The fair value of each option grant is estimated on the date of

grant using the Black-Scholes option-pricing model. When determining

expectedvolatility,theCompanyconsidersthehistoricalperformance

of the Company’s stock, as well as implied volatility. The risk-free interest

rate is based on the U.S. Treasury yield curve in effect at the time of

grant,basedontheoptions’expectedterm.Theexpectedtermof

the options is based on the Company’s evaluation of option holders’

exercisepatternsandrepresentstheperiodoftimethatoptionsare

expectedtoremainunexercised.TheCompanyuseshistoricaldatato

estimate the timing and amount of forfeitures. The assumptions used in

the Black-Scholes option-pricing model for options granted in 2010, 2009

and 2008 are as follows:

2010 2009 2008

Assumptions used:

Expectedvolatility 37.7%-41.4% 36.4%-38.6% 25.0%-32.2%

Weighted-average

expectedvolatility 39.4% 36.4% 25.1%

Expecteddividend

yield 0.96%-1.30% 0.82%-0.97% 0.56%-0.74%

Weighted-average

dividend yield 1.07% 0.82% 0.56%

Risk-free interest rate 1.22%-2.30% 1.70%-2.08% 2.19%-3.09%

Weighted-average

risk-free interest rate 2.02% 1.71% 2.19%

Expectedterm,inyears 4-5 4 4

Weighted-average

expectedterm,inyears 4.42 4 4

The weighted-average grant-date fair value per share of options

grantedwas$7.68,$4.58and$5.25in2010,2009and2008,respectively.

Thetotalintrinsicvalueofoptionsexercised,representingthedifference

betweentheexercisepriceandthemarketpriceonthedateofexercise,

wasapproximately$6million,$8millionand$17millionin2010,2009

and 2008, respectively.

Transactions related to stock options issued for the year ended

January 28, 2011 are summarized as follows:

Weighted-

Weighted- Average Aggregate

Average Remaining Intrinsic

Shares ExercisePrice Term Value

(In thousands) Per Share (In years) (In thousands)

1

Outstanding at

January29,2010 23,170 $26.42

Granted 3,208 23.96

Canceled, forfeited

orexpired (883) 26.74

Exercised (1,386) 19.31

Outstanding at

January28,2011 24,109 $26.48 3.06 $49,035

Vested and

expectedtovestat

January 28, 20112 23,473 $26.56 2.98 $48,083

Exercisableat

January28,2011 16,750 $29.13 2.04 $13,851

1 Options for which the exercise price exceeded the closing market price of a share of the Company’s common stock

at January 28, 2011 are excluded from the calculation of aggregate intrinsic value.

2 Includes outstanding vested options as well as outstanding, nonvested options after a forfeiture rate is applied.

Performance Accelerated Restricted Stock Awards (PARS)

PARS are valued at the market price of a share of the Company’s

common stock on the date of grant. In general, these awards vest

at the end of a five-year service period from the date of grant, unless

performance acceleration goals are achieved, in which case, awards

vest 50% at the end of three years or 100% at the end of four years.

The performance acceleration goals are based on targeted Company

average return on beginning non-cash assets, as defined in the PARS

agreement.PARSareexpensedonastraight-linebasisovertheshorter

oftheexplicitserviceperiodrelatedtotheserviceconditionorthe

implicit service period related to the performance conditions, based on

the probability of meeting the conditions. The Company uses historical

data to estimate the timing and amount of forfeitures. No PARS were

granted in 2010, 2009 or 2008. The total fair value of PARS vested

wasapproximately$7millionin2010and$6millionin2008.NoPARS

vested in 2009.

Transactions related to PARS issued for the year ended January 28,

2011 are summarized as follows:

Weighted-Average

Shares Grant-Date Fair

(In thousands) Value Per Share

NonvestedatJanuary29,2010 1,073 $32.91

Vested (311) 30.00

Canceled or forfeited (29) 33.59

NonvestedatJanuary28,2011 733 $34.11

Performance-Based Restricted Stock Awards

Performance-based restricted stock awards are valued at the market

price of a share of the Company’s common stock on the date of grant.

In general, 25% to 100% of the awards vest at the end of a three-year

service period from the date of grant based upon the achievement of

a threshold and target performance goal specified in the performance-

based restricted stock agreement. The performance goal is based on

targeted Company average return on non-cash assets, as defined in

the performance-based restricted stock agreement. These awards

areexpensedonastraight-linebasisovertherequisiteserviceperiod,

based on the probability of achieving the performance goal. If the

performance goal is not met, no compensation cost is recognized

and any previously recognized compensation cost is reversed. The

Company uses historical data to estimate the timing and amount of

forfeitures. The weighted-average grant-date fair value per share of

performance-basedrestrictedstockawardsgrantedwas$23.97in

2008. No performance-based restricted stock awards were granted

in 2010 or 2009. The total fair value of performance-based restricted

stockawardsvestedwasapproximately$4millionin2010.No

performance-based restricted stock awards vested in 2009 or 2008.

During 2008, the Company amended all 2007 performance-based

restricted stock agreements, modifying the performance goal to a

prorated scale, which caused the probability of vesting to go from

improbable to probable.