McDonalds 2010 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2010 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

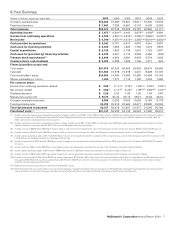

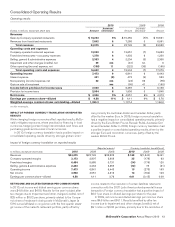

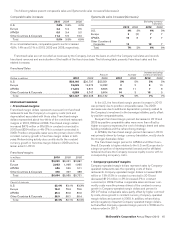

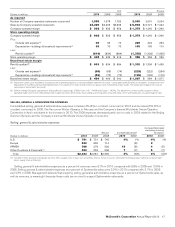

items, food events and limited-time offerings to present a bal-

anced mix of products to our customers. Value will continue to be

a key growth driver as we reinforce the affordability of our menu

to consumers and build on our successful Value Lunch platforms.

We will invest in our business primarily by opening over 600 new

restaurants and reimaging over 500 existing restaurants while

elevating our focus on service and operations to drive efficien-

cies. In China, we will continue to build a foundation for long-term

growth by increasing our base of restaurants by approximately

15% in 2011 toward our goal of nearly 2,000 restaurants by the

end of 2013. Convenience initiatives include expanding delivery

service across the region and building on the success of our

extended operating hours.

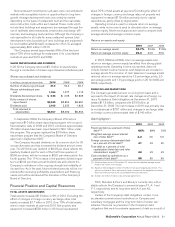

McDonald’s has an ongoing commitment to optimize our res-

taurant ownership structure. A heavily franchised, less capital-

intensive business model has favorable implications for the

strength and stability of our cash flow, the amount of capital we

invest and long-term returns.

We continue to maintain a strong culture of financial dis-

cipline by effectively managing all spending in order to maximize

business performance. In making capital allocation decisions, our

goal is to elevate the McDonald’s experience by driving sustain-

able growth in sales and market share while earning strong

returns. We remain committed to returning all of our free cash

flow (cash from operations less capital expenditures) to share-

holders over the long term via dividends and share repurchases.

McDonald’s does not provide specific guidance on diluted

earnings per share. The following information is provided to assist

in analyzing the Company’s results:

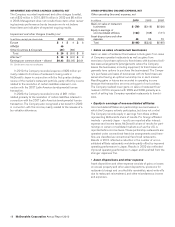

• Changes in Systemwide sales are driven by comparable sales

and net restaurant unit expansion. The Company expects net

restaurant additions to add approximately 1.5 percentage

points to 2011 Systemwide sales growth (in constant

currencies), most of which will be due to the 541 net traditional

restaurants added in 2010.

• The Company does not generally provide specific guidance on

changes in comparable sales. However, as a perspective,

assuming no change in cost structure, a 1 percentage point

increase in comparable sales for either the U.S. or Europe

would increase annual diluted earnings per share by about

3 cents.

• With about 75% of McDonald’s grocery bill comprised of 10

different commodities, a basket of goods approach is the most

comprehensive way to look at the Company’s commodity costs.

For the full year 2011, the total basket of goods cost is

expected to increase 2-2.5% in the U.S. and to increase

3.5-4.5% in Europe as compared to 2010. Some volatility may

be experienced between quarters in the normal course of

business.

• The Company expects full-year 2011 selling, general & admin-

istrative expenses to decrease 2-3%, in constant currencies,

partly due to higher incentive compensation in 2010 based on

performance. In addition, fluctuations will be experienced

between quarters due to certain items in 2010, such as the

Vancouver Winter Olympics in February and the biennial

Worldwide Owner/Operator Convention in April.

• Based on current interest and foreign currency exchange rates,

the Company expects interest expense for the full year 2011

to increase approximately 7% compared with 2010.

• A significant part of the Company’s operating income is gen-

erated outside the U.S., and about 40% of its total debt is

denominated in foreign currencies. Accordingly, earnings are

affected by changes in foreign currency exchange rates,

particularly the Euro, Australian Dollar, British Pound and

Canadian Dollar. Collectively, these currencies represent

approximately 65% of the Company’s operating income out-

side the U.S. If all four of these currencies moved by 10% in

the same direction, the Company’s annual diluted earnings per

share would change by about 20 cents.

• The Company expects the effective income tax rate for the full

year 2011 to be approximately 30% to 32%. Some volatility

may be experienced between the quarters resulting in a quar-

terly tax rate that is outside the annual range.

• The Company expects capital expenditures for 2011 to be

approximately $2.5 billion. About half of this amount will be

used to open new restaurants. The Company expects to open

about 1,100 restaurants including about 400 restaurants in

affiliated and developmental licensee markets, such as Japan

and Latin America, where the Company does not fund any

capital expenditures. The Company expects net additions of

about 750 traditional restaurants. The remaining capital will be

used for reinvestment in existing restaurants. Over half of this

reinvestment will be used to reimage approximately 2,200

locations worldwide, some of which will require no capital

investment from the Company.

12 McDonald’s Corporation Annual Report 2010